KARACHI: Mounting escalation in the Middle East and subsequent supply disruption due to closure of Strait of Hormuz continued dampening equity investors sentiments as surging oil prices hit global economies with no exception to Pakistan, which meets its 85 per cent energy needs through imports, the Pakistan Stock Exchange (PSX) closed in the red for the second straight session on Thursday.

A delay in reaching a Staff-Level Agreement (SLA) with the International Monetary Fund on the third review of the country’s $7 billion Extended Fund Facility (EFF) and the second review of the Resilience and Sustainability Facility (RSF) within the scheduled time-frame also contributed to market volatility.

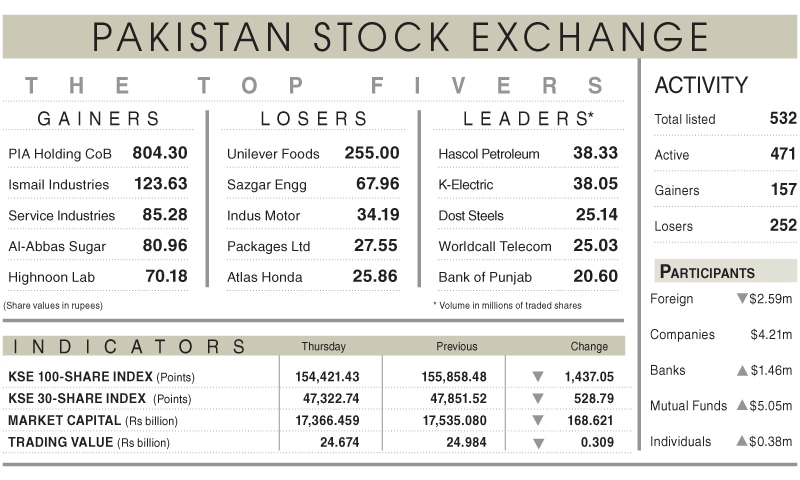

Ali Najib, Deputy Head of Trading at Arif Habib Ltd (AHL), said the PSX witnessed another directionless and volatile session, with the benchmark KSE-100 index settling at 154,421, down 1,437 points or 0.92pc from the previous close.

During the session, the market experienced notable fluctuations, with the index moving within a 3,577-point range. It recorded an intraday high of 157,080 and an low of 153,504, reflecting cautious investor sentiment and intermittent profit-taking amid lingering uncertainty.

On the sectoral front, energy production showed encouraging momentum. Gas output increased by 11.8pc week-on-week to 3,005 mmcfd in the first week of March, while oil production rose 6.1pc to 62,714 bopd. The improvement was primarily driven by reduced curtailment in northern fields alongside stronger demand from the power sector.

Topline Securities Ltd noted that the mid-session optimism sparked a rebound, briefly lifting the market into positive territory. However, the recovery proved

short-lived as profit-taking and cautious sentiment amid the ongoing Middle East conflict dragged the index back into the red.

Among index-heavy stocks, Engro Holdings, Systems Ltd, Service Industries, Engro Fertiliser, and Highnoon Laboratories emerged as key gainers, collectively adding 745 points to the index. Conversely, United Bank, Lucky Cement, Oil and Gas Development Company, Hub Power, and MCB Bank weighed heavily on the market, cumulatively dragging 972 points from the benchmark.

Market participation remained low as the trading volume dipped 8.51pc to 404 million shares and the traded value eased to Rs24.67b from the previous session.

As the market heads into the final trading session of the week, momentum will largely depend on the stability of geopolitical developments.

Published in Dawn, March 13th, 2026