KARACHI, Oct 24: Stocks on Monday recovered from the last weekend lows as dividend-aided covering purchases put the market back on the rails, although underlying sentiment was still a bit shaky.

KARACHI, Oct 24: Stocks on Monday recovered from the last weekend lows as dividend-aided covering purchases put the market back on the rails, although underlying sentiment was still a bit shaky.

Selective support, however, emerged strong on a number of counters, which allowed the market to maintain a steady posture despite several negative counter-pulls and the weakness of the some leading base shares including OGDC ahead of its board meeting. Technically, stocks resumed trading on a promising note as leading bulls were back in the market and made extensive covering purchases in most of the pivotals at the lower levels, trend-setters being bank and oil shares.

But the chief motivating factors behind the recovery appears to be reports of higher corporate earnings and talk of interim dividend by some of the leading companies whose quarterly board meetings are due during the current and next week.

Boards of Pakistan Petroleum, Askari Bank, Packages, Bank Alfalah, OGDC, Unilever Pakistan, Saudi Pak Commercial Bank and Nestle Pakistan are scheduled for the current week and there is market talk of higher interims.

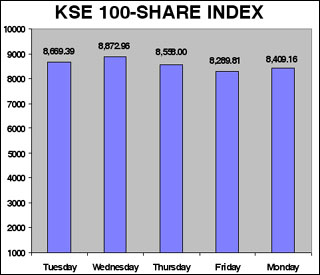

The market’s recovery momentum was also evident by a smart recovery of 119.35 in the KSE 100-share index at 8,409.16 and managed to recover in part some of the losses it suffered during the last two sessions of the previous week.

Bank, oil and cement shares led the market recovery followed by leading shares on the other counters but buying was not that aggressive as it should have been in a massively battered market, which shed 575 points or about seven per cent last week.

The selling in October contract on the forward market, which caused major dents in the firm price structure last week, may not be yet over but bulk of it has already been absorbed and may not be a future threat to the market set price pattern. “But the situation on the PTCL deal is still not clear”, analysts said, adding “as the deadline of Oct 28 set to sort out pending issues between the seller and the buyer is approaching investors are worried over the final outcome”.

Already it had shed about Rs6 from Rs68 to Rs62 during the last week and further weakness in its share value could jolt the entire market again, they said.

“I fear the deal may not go through as the Pakistan government has already rejected the two major demands of Etisalat”, fear a leading broker “some of us are already preparing to hear that bad news.” But Monday’s modest recovery signals some positive developments on the deal.

Etisalat has reportedly sought to raise credits from the Pakistani banks after having pledged their shareholding and to increase their stake in the deal after purchasing PTCL’s B class shares.

Etisalat has reportedly sought to raise credits from the Pakistani banks after having pledged their shareholding and to increase their stake in the deal after purchasing PTCL’s B class shares.

Last week’s seven per cent drop in the index was attributed partly to selling in October futures, which will be rung off the board during the next couple of sessions, and partly to conflicting reports about the PTCL deal, brokers said.

Plus signs were strewn all over the list, leading gainers being Siemens Pakistan, Shell Pakistan, Attock Petroleum, Pakistan Oilfields and PSO, which posted gains ranging from Rs9.35 to Rs19.15.

They were followed by National Bank, MCB, Thal, National Refinery, Packages, Engro Chemicals and Millat Tractors, up by Rs6 to Rs8.

Losers were led by Fazal Textiles, Arif Habib Securities, National Foods, Pakistan Cables, Bestway Cement, Wyeth Pakistan, Bank of Punjab, EFU Life and Atlas Honda, off Rs3 to Rs8.

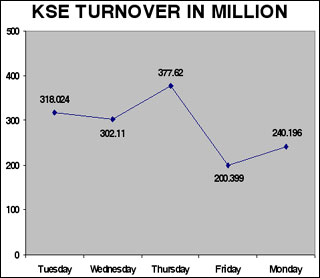

Trading volume showed a modest rise at 240m shares from the previous 200m shares as gainers held a comfortable lead over the losers at 183 to 97, with 23 shares holding on to the last levels.

Bank of Punjab came in for fresh unloading and was marked down by Rs5.25 at Rs100 on 41m shares followed by National Bank, up by Rs7.30 at Rs153.40 on 29m shares, OGDC, lower Rs1.55 at Rs107.40 on 27m shares, PTCL, up by 95 paisa at Rs63.35 on 22m shares, Pakistan Petroleum, higher by Rs9.35 at Rs119.15 on 14m shares, Pakistan Oilfields, up by Rs15.75 on 13m shares and MCB, higher by Rs6.80 at Rs142.80 on 7m shares.

Other actives included PSO, higher by Rs19.15 at Rs402.20 also on 7m shares, Fauji Cement, up by Re1 at Rs18.60 on 12m shares and Fauji Fertiliser Bin Qasim, higher by Rs1.25 on 11m shares.

FORWARD COUNTER: OGDC led the list of losers on this counter, off Rs1.75 at Rs107.95 on 13m shares followed by National Bank, up by Rs7.36 at Rs154.61 on 12m shares and Pakistan Petroleum, higher by Rs8.59 on 11m shares.

Bank of Punjab on the other hand received fresh battering, off Rs5.35 at Rs101.80 on 10m shares, Pakistan Oilfields, sharply higher by Rs14.90 at Rs412.90 on 8m shares and some others rose modestly higher but on light turnover.

The notable feature was that trading also resumed in the November settlements side by the maturing October contracts, which will be rung off the board on Oct 28.

DEFAULTER COS: There was no larger turnover in any of the share but some of the leading among them showed erratic price movements. While Glamour Textiles, Ghandhara Industries and Morafco Industries posted gains ranging from Re1 to Rs2.15, Mehr Dastgir Textiles and Saleem Denim fell by Re1 each on light turnover. Others showed fractional changes.

DIVIDEND: Dawood Hercules, cash interim at the rate of 20 per cent, Callmate Telips, bonus shares of 7.5 per cent and Prudential Discount House, interim 2.5 per cent.