We are living through strange times. Many lifetimes ago, the world seemed to be heading in a very different direction. Students were on the streets across Europe and America, protesting wars and trying to dismantle the political structure and the ones who it served. Decolonisation was still fresh, and most importantly, there appeared to be genuine optimism.

Sixty years later, the mood could not be more different. Borders are hardening, tariffs are back in fashion, and the open-order gospel that era produced has few serious defenders left. Even something as horrendous as almost the entire global elite being in the Epstein files has done little to shake the status quo.

Pakistan’s own arc mirrors that reversal in a rather hilarious manner. During that era, development economists, instead of national security scholars, paid attention to the country. It was the same intellectual climate, filled with postcolonial optimism, that produced convergence theory.

As an academic field, development economics drew serious intellectual firepower from this region, with major contributions from Sen, Haq, and Sobhan, among others. Central to it was the so-called advantage of backwardness, the idea that poorer countries could grow faster precisely because they were starting from a lower base, and would, over time, close the gap with richer ones.

The relative safety of emerging market workers stems largely from their concentration in primary industries, which already generate lower per-capita output than the export-oriented services sectors AI is now disrupting

The numbers, however, tell a more complicated story. The US accounted for 40 per cent of global GDP in 1960, a share that has since declined to 26pc. On the surface, that looks like progress. But almost the entire share ceded by Washington was captured by Beijing. The unipolar economic order simply gave way to a bipolar one, rather than the egalitarian spread that globalists like to point to. At the frontier of innovation and value creation, concentration has been accelerating, not diffusing. AI is not arriving into a world on the path to convergence. It is arriving into one that was already diverging.

For emerging markets, the traditional development playbook suggested two main pathways; build a low-cost manufacturing base and export those goods to richer markets; and/or become an offshore tradeable services hub. Other than mineral-rich economies, almost every success story of the past 50 years essentially followed one of these two pathways. Southeast Asia, including South Korea and China, took the former route while India’s rise was rooted, in part, in the services offshoring boom.

Both of these options are at risk today because of AI.

To be fair, there were some question marks even before. According to the World Bank, 108 countries remain stuck in the middle-income trap — including economies that industrialised successfully, as their cost advantage eroded faster than their productivity advanced. Only 34 have crossed that threshold to reach “high-income” status since 1990, with a combined population equal to Pakistan’s, of which a third either joined the EU or struck oil.

In manufacturing, the post-Covid supply chain scare made the risks of offshoring glaringly obvious, which, coupled with anti-trade sentiment, brought reshoring back into the national agenda for many developed markets. But beyond protectionist hyperbole, realising those promises has proved difficult so far because it’s still much cheaper to produce goods in the developing countries.

However, that labour arbitrage is not forever going to hold, and as advancements in robotics materialise, the economics of reshoring will become a lot more appealing. Meanwhile, high-value manufacturing — batteries, electric vehicles, clean energy hardware, among others — is heavily dominated by China, so replicating it elsewhere would be quite an endeavour, to put it mildly.

The services story is more immediate and more disruptive. Generative AI has fundamentally altered the economics of knowledge work, which is precisely what the offshoring model was selling. It may sound like a doomsday warning, but there’s no doubt that all state-of-the-art models now comfortably surpass what an average worker produces, when adjusted for price and delivery timelines.

Early evidence doesn’t paint a particularly rosy picture. Since early 2024, ie when Opus 3.5 was released, the five largest Indian IT firms have seen a median stock decline of roughly 19pc. More noticeably, revenue and profit growth rates have both slowed. Of course, the post-pandemic spending correction definitely would have played a role there, but dismissing the signal entirely would also be a mistake.

And these are not low-end operators. The firms in question sit at the premium end of the offshoring market, handling enterprise software, consulting, and complex IT delivery. If AI is moving the needle there, the implications for the rest of the pyramid are far worse.

Usually, the boilerplate response to such warning signs is that workers need to upskill themselves with AI. But it still ignores the fundamental question of whether genAI will augment or substitute the labour force.

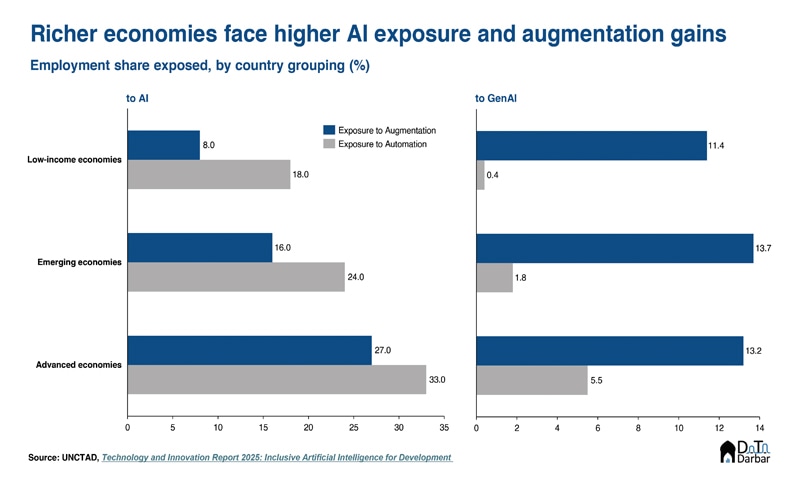

The International Monetary Fund’s 2024 paper on AI and the future of work attempts to answer this by assessing countries and occupations through two lenses: exposure to AI and complementarity with it. It finds advanced economies more at risk, while emerging markets appear less vulnerable. But that conclusion is less reassuring than it sounds. The relative safety of emerging market workers stems largely from their concentration in primary industries, which already generate lower per-capita output than the export-oriented services sectors AI is now disrupting.

A recent Moody’s report adds some texture to this. It estimates annual productivity gains of 1.2pc-2.9pc for advanced economies, against just 0.4pc-1.4pc for emerging markets. The divergence stems from occupational structure — advanced economies simply have a greater share of workers in roles that AI can augment. The gap, in other words, is baked in.

Ironically, if AI is closing down both traditional pathways to convergence — manufacturing and services — the only remaining escape route is to build frontier technology. But that requires access to capital and computing at a scale that is itself increasingly concentrated in a handful of geographies, with emerging markets having little stake. Nothing illustrates better than the state of venture funding in 2025 which saw AI companies raise roughly 52pc of the aggregate, with almost 80pc of it going towards North America, as per Pitchbook.

This will have compounding effects as the financial returns from these investments would inevitably flow to advanced economies through the investment returns channel, only further widening the gap with other countries. Emerging markets, in other words, are being asked to absorb the disruption without any meaningful stake in the upside.

There is, of course, the possibility that this is all noise. Perhaps another tech cycle is running ahead of its fundamentals, one that will correct course. And for all the capabilities on show, the hard impact of AI on global output is yet to be seen, something Microsoft CEO Satya Nadella himself alluded to recently. But that is somewhat beside the point.

In some ways, the current moment is not too unlike the 1960s — each convinced it was standing at the edge of a fundamental shift. But at least back then, for all the naivety, there was a seat at the table for workers and developing nations. That assumption is conspicuously absent this time.

As far as Pakistan is concerned, things were never comforting in the first place, as the process of deindustrialisation started a little too early. In fact, the country’s value-added manufacturing as a share of GDP has only trended down, sliding to 13pc by 2024, albeit from still a fairly low peak of 16pc back in 1994. Contrast this with Bangladesh, which sits at 22pc or Indonesia, 19pc.

Unsurprisingly, the performance is worse when it comes to exports, whose share in the GDP has slipped to just 10.4pc as of 2024, a far cry not only from our own peak of 17.3pc more than three decades ago (1992) but also a fraction of where low & middle income group countries currently stand (24.5pc).

To make matters worse, the key driver — textile — has consistently punched below its weight and is among the least productive industries, as revealed in the Planning Commission’s own research.

It’s no wonder then that Pakistan’s ranking on the Economic Complexity Index, a measure of the diversity and sophistication of a country’s export basket, places it near the bottom of the global distribution, reflecting a structural inability to move up the value chain that long predates AI.

The services side presents a different kind of vulnerability, precipitated by AI. For the last decade, Pakistan’s information and communication technology exports have ballooned to $4.2 billion, increasing at an impressive compound annual growth rate of 18.2pc. More importantly, its share in the broader services inflows now stands at 46pc. Unfortunately, this is the first in the ranks to be hit by genAI.

Almost funnily, IT services were supposed to be the way out of Pakistan’s balance of payment troubles, and for a while, things seemed to be doing well. But it appears that our moment has already passed, even before it arrived. I guess Muneer Niazi was referring to our economic plight when he wrote “hamesha dair kardeta hun”.

Mutaher Khan is co-founder of Data Darbar and works for the Karachi School of Business and Leadership

Published in Dawn, The Business and Finance Weekly, March 2nd, 2026