Pakistan, at this critical time in its economic and political history, faces not one but three energy crises. Two of these are of its own making; the third is the consequence of the developments over which its policy makers have neither influence nor control. The two that are the product of public policy failure concern the short supply of two important components of energy – electricity and natural gas.

Pakistan, at this critical time in its economic and political history, faces not one but three energy crises. Two of these are of its own making; the third is the consequence of the developments over which its policy makers have neither influence nor control. The two that are the product of public policy failure concern the short supply of two important components of energy – electricity and natural gas.

The third, of course, is the way the global oil market is evolving which has taken the price of crude oil to around $140 a barrel. The price rise has been sharp; in the first six months of 2008, it increased by 40 per cent. The way the oil market is working has puzzled both producers and large consumers. A special meeting convened by King Abdullah of Saudi Arabia on June 21 failed to identify the reasons for the continuous and unrelenting increase in the price of oil.

The purpose here is not to discuss the recent working of the international oil market and how it is impacting and will impact a country such as Pakistan that relies heavily on imported oil. That is an extremely important subject but I will save its discussion for a later date. Today the focus will be on one aspect of the energy crisis Pakistan faces: to explore why the policy makers have failed so often to plan for the steady supply of energy to the consumers.

There are basically two ways of developing the energy sector. The first is to estimate the increase in GDP and to determine the contribution each of the important sectors of the economy would make to anticipated growth. It is important to have a good appreciation of the sectoral determinants of economic growth. If growth is led by industry or the IT sector, there will be higher demand for energy than would be the case if agriculture or traditional services led the way.

That said, a rough estimate for the anticipated increase in energy demand can be made by applying to a situation what we know through empirical analysis. It is generally recognised that the demand elasticity for energy – the ratio of increase in the need for energy to the rate of growth in national output – is more than one. Sometimes it may be much higher than one. This means that if GDP grows by one per cent a year, the need for energy will increase by more than one percent per annum.

The demand elasticity for Pakistan, given the structure of consumption, is possibly in the range of 1.2 to 1.4. This means that if the GDP is growing at seven per cent a year – the rate achieved by the country in the five year period between 2002 and 2007 – the demand for energy will increase at the rate of 8-10 per cent a year. Having determined some indication of the growth in demand, the government must develop a programme to satisfy it.

For a country where the production of various forms of energy is the responsibility of the public sector, adequate provision needs to be made in the government’s programme for increasing supply by appropriate amounts. Until the early 1990s, the Pakistani state had a virtual monopoly over the production, transmission and distribution of various forms of energy.

The second way is to leave the estimation of energy requirement and satisfaction of demand to the market place. This approach works in the countries where the state has only a regulatory role to perform; the private sector is entirely responsible for providing energy supply. In such systems, demand analysis and provision of supply is done locally; there is little, if any, state planning and guidance.

Since in many situations, monopolies tend to constrain supply to push up prices and hence profits, such behavior is controlled by regulatory action. Regulatory Commissions usually have good representation of consumers who watch over the working of the companies that operates in the energy sector. One important exception to this rule is the oil and petroleum sector where there is brisk competition among many suppliers and prices are determined by market considerations.

Some of the public policy shortfalls that have produced such a serious energy situation can be attributed to the structural changes in governance that began to be introduced in the mid-1990s. That was another period during which there had to be a resort to load-shedding of electricity to balance supply and demand. The state, constrained by the shortage of finance, was persuaded to turn to the private sector to meet the growing demand for power.

The persuasion was done by the international financial institutions, in particular the World Bank, to induct independent power producers (IPPs), into the power sector. The government led by Prime Minister Benazir Bhutto accepted the advice and opened up one part – the sector of generation – to the private sector. Reorganisation of the Water and Power Development Authority, the Wapda, which had the monopoly not only to generate electricity but also to transmit and distribute it in all parts of Pakistan other than Karachi, was aimed an opening up other parts of the power supply system to private participation. This reorganisation was still going when there was a regime change in Pakistan.

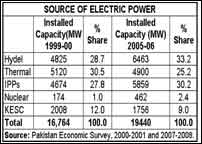

As shown in the accompanying table, the IPPs made a remarkable difference in short time to the energy situation in the country. By 1999-2000, they were contributing 27.8 per cent to installed generation capacity, almost equal to the share of hydro power. Thanks to the IPPs, within three years, the country went from severe shortages to a reasonable surplus of power. In the late 1990s, when relations between India and Pakistan began to thaw, Islamabad seriously contemplated sale of power to its neighbour which had also developed serious electricity shortages. Such a sale would have been possible; all that was required was to link the transmission systems of the two countries. Connecting the grids was not only feasible; it would also have been relatively inexpensive. The distance between the two systems was small and could be easily bridged.

Two developments took place to disturb this happy situation. In November 1996, the Bhutto government was dismissed to be replaced, after a short interregnum, by an administration led by Prime Minister Nawaz Sharif. Corruption was one of the many charges leveled by President Farooq Leghari against his prime minister. The power sector was singled out especially as an area of government activity in which large favours were granted in return for hefty bribes allegedly paid to senior officials. The Sharif government, using the charge sheet issued by President Leghari, against his predecessor reversed the position her administration had taken in the power sector. Pakistan has a long and troubling history of lack of continuity in public policy. Major policy initiatives taken by one regime were discontinued when it was replaced by another. The change from Bhutto to Sharif resulted in the same kind of interruption. The power sector was particularly affected. The new administration not only abandoned support to the IPPs in the energy sector, it also instituted the policy to renegotiate the deals that were struck between the power generating enterprises and Wapda.

The Authority gave the guarantee of procuring all that was produced by the IPPs but at a pre-determined price. These steps were not appreciated by the IPP owners. The private sector does not act favourably to two things: lack of continuity in public policy and breach of contracts by the government. Both happened and the flow of private capital into electric power generation came to a complete halt.

The other development that adversely affected the power sector happened during the period of President Pervez Musharraf. During this time, the state pulled back some distance from economic management, allowing a great deal of space to the private sector. This was a positive development but in a hybrid system of economic management, the state must not give up some of the functions it must perform. In the power sector, in spite of the share that had been allowed to the IPPs, two-thirds of the power was still being generated by the state entities. (See the table.) The state should have planned for the future increasing its own investments while rewriting the conditions for getting the IPPs back into the sector. The fact that neither got done constituted a major failure of public policy leading to the crisis the country currently faces. To deal with it, policy makers must start by clearly defining the role of the state, the amount of space allowed to the private sector and the conditions under which private operators can work in the system, and give the assurance that once contracts are awarded, they will not be tempered with.