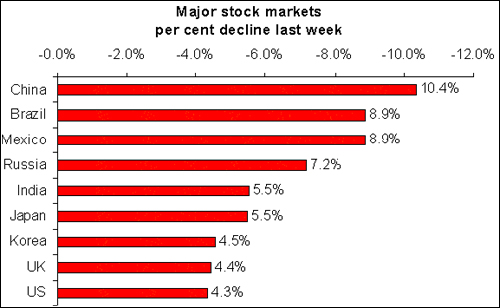

LAST week’s sell-off in global stock markets wiped off nearly $1.2 trillion of investors’ wealth worldwide. It started with nearly a nine per cent plunge February 27 — worst in a decade — in China’s main stock market, which had hit a new high only a day earlier.

LAST week’s sell-off in global stock markets wiped off nearly $1.2 trillion of investors’ wealth worldwide. It started with nearly a nine per cent plunge February 27 — worst in a decade — in China’s main stock market, which had hit a new high only a day earlier.

The US market followed the plunge the same evening and fell by 3.5 per cent — a daily record decline in more than three years. Asian markets, which had all shrugged off Tuesday’s decline in Shanghai, dropped sharply on Wednesday morning in response to the heavy selling in Europe and New York. Most stock markets finished the week down five to nine per cent.

The markets had started the New Year on a generally positive note but last week’s fall erased gains of the major equity indexes and sparked fears of a general flight from risky assets, such as equities and emerging markets, to cash and bonds. The VIX index, a measure of volatility (or risk) in global financial markets, shot up by 75 per cent to its highest level since July 2006 as the markets swung wildly during the week.

Was this a healthy correction or the beginning of a bigger tumble in weeks or months to come? In 2006, US stock markets dropped by about eight per cent during May-June and Emerging Markets by about 20-25 per cent but recovered four/five months later to climb to even higher levels.

Shanghai’s index — dominated by state-owned banks and property companies- is hardly a barometer of the Chinese economy and accounts for less than one per cent of the world’s market capitalisation. Domestic retail investors drive the market as China restricts the foreign investors to a quota. The market has more than doubled in one year and almost tripled since June 2005 and currently trades at a price to earnings (P/E) multiple of 31 compared to 15 in the United States.

Stock trading has spread like a mania in China’s big cities with taxi drivers, office workers and sundry taking punts on their favourite stocks. Earlier, the Chinese government had warned banks about improper loans to finance stock speculation. Hence, the plunge, though large, was not without precedent when such feverish conditions exist. What was surprising that its tremors were felt globally.

The timing of the comments of former Federal Reserve chairman Alan Greenspan did not help the US markets. On Monday, he said that a US recession is possible (but not probable) by the end of this year. “Profit margins suggest the economy is in the later stages of a cycle”, he added. The following day, the data for the orders placed with US factories for capital goods reported the biggest drop in four months indicating slowdown in investment spending. More negative economic data came on Friday. The US consumer confidence for February fell to 91.3 from 96.9 at the end of January, reaching a five-month low as concerns over incomes and jobs in a slowing economy weighed in. The US stocks finished the week with their biggest weekly decline in almost four years.

Nevertheless, it is difficult to attribute last week’s record drop to just economic causes or fears of a slowdown in the US or China. These concerns have been frequently voiced in the recent past but the markets continued their rise. While it is always easy to have the benefit of hindsight, it appears that investors were simply looking for excuses to take profits. A decline looked overdue. Wall Street had enjoyed its longest period without a two per cent daily fall for more than five decades. Margin debt — the money investors borrow from brokers — had just passed its previous peak in March 2000, recorded during the dotcom bubble.

Last Tuesday, it was not just the stock markets that dropped. dollar lost 2.25 per cent against Japanese Yen while it gained against most emerging market currencies. The yen's recent strength has been a concern to stock-market investors, as many hedge funds borrow in yen to fund trades made elsewhere in the world. Should the yen appreciate too rapidly, the "carry trade," a popular strategy in which investors borrow in low-yielding yen to invest in higher-yielding assets, could unwind further and exacerbate market declines and volatility.

Many analysts believe that the fall in the Chinese market may simply have been the wake-up call the bulls needed to take a closer look at the risks they have been taking and at the stock valuations. While this may be true from a short-term view, the fundamental reasons for longer-term bullish behaviour go beyond the US economy or complacency of the investors.

The overarching reason is actually quite simple. Since 2000, world GDP per head has grown by an average of 3.2 per cent a year, beating the previous record of 2.9 per cent annual growth during 1950-73, when Europe and Japan were rebuilding their economies after the war. This means that the first decade of the 21st century could see the fastest growth in average world income in the whole of history.

Emerging economies are now a key driver of global growth and have a far greater influence on the performance of the rich economies than is generally realised. The rich countries no longer dominate the global economy. In 2005, the combined output of emerging economies reached an important milestone: it accounted for more than half of total world GDP (measured at purchasing power parity). They no longer are net borrowers as they were in the 1980s and 1990s and are running record current account surpluses. Their combined foreign exchange reserves now represent nearly 60 per cent of the world’s total and are a major source of financing the US current account deficit and of liquidity to the global financial markets.

This emerging economies’ growth has coincided with a tripling of the oil price since 2001. The oil producing countries in the Middle East have generated excess liquidity of around $400 billion in the last five years and their estimated investment portfolios (since they do not disclose their foreign exchange reserves) are believed to have crossed $3 trillion. A lot of this money has been recycled by professional investment managers into global financial markets through different instruments like treasury bonds, debt products, hedge funds, private equity and stocks, etc.

If bulk of this money was invested in real assets globally, the financial markets will not be so flushed with liquidity. An abundance of liquidity has increased risk-taking appetite — particularly for higher yielding assets — as volatility has declined to historic lows, except for periodic surges, compared to its long-term averages. Hence, investors have been willing to make bigger and often more leveraged bets on risky assets than they were in the past.

Any surge in volatility drives the investors to sell investments perceived to have higher risk or those that involve the use of debt such as the “carry trades”. Emerging Markets stocks are one example of assets perceived to have higher risk.

It is clear that the emerging markets were hit harder last week, compared to the developed markets despite their relatively higher growth potential and lower valuations. This appears to have been anticipated by some investors who withdrew money from emerging markets funds. Emerging markets equity funds had net outflows of $600 million in the week ended Feb 28, 2007 after 19 weeks of inflows out of 20.

Since October 4, 2006, when flows turned positive after $18 billion of outflows that started with the May 2006 sell-off in emerging markets, cumulative aggregate inflows stand at $19.2 billion, with Asia accounting for 72 per cent of the total. During 2007, aggregate flows of $6.1 billion compare to $14.5 billion during the same period in 2006 and $2.4 billion in 2005.

Pakistan received about $275 million in foreign investors’ flows in 2007 and this together with strong support from local investors enabled its market to post good gains in January. It lost about four per cent last week. With the reversal of global equity flows, local investors will be watching the foreign funds’ managers to see if they will trim their bets on Pakistan’s market. If they do, Pakistan’s market may have more downside in the coming weeks and months. But is there a bubble in the global stock markets that is about to burst? If valuations are any indication, the answer is a NO.