DESPITE a weak performance tuned in by blue chip counters, the stocks maintained an uppish leaning last week on active short-covering at the dips. The KSE 100-share index briefly touched the 8,000-point level.

DESPITE a weak performance tuned in by blue chip counters, the stocks maintained an uppish leaning last week on active short-covering at the dips. The KSE 100-share index briefly touched the 8,000-point level.

Though, the week’s best level could not be sustained owing to late selling but the on-balance trend remained high as the dividend-driven rally manifested itself on selective counters.

The bulk of buying remained confined to cement on the expectations of higher payouts in the backdrop of a steep rise in sales and some bank shares, notably the National Bank, the MCB and the Bank of Punjab.

The stocks, therefore, explored new highs as investors failed to take a technical breather in an effort not to miss the rising market. Both, the KSE index and the market capital added significantly to the total amid brisk activity and large volumes.

The price flare-up was attributed to an increase in the existing fund under the Continuous Funding System.

Despite the mid-week sluggishness, the KSE index briefly touched 8,000 points on rumours of an increase in the CFS amount. The CFS was available for 14 active and most liquid scrips on forward counter.

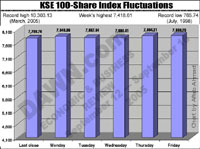

It finished the week with an extended gain of 45.31 points at 7,934.54 as compared to 7,889.25 a week earlier despite weakness of leading base shares, notably the PTCL, the OGDC and some others. The market capital also rose by Rs30 billion at Rs2,285 billion. The market capital rose by Rs24 billion at Rs2,272.973 billion.

It may not be galloping to hit the previous all-time peak level of 10,303 points and a market capital of $45 billion as it has, since March, declined by about 23 per cent. However, the index was maintaining its upward drive on the strength of higher dividend and an attractive bait of capital gains, said a leading broker.

Click to view the larger image

Much of the activity remained confined to bank and cement shares, notably the National Bank, the MCB, the Bank of Punjab, the D.G. Khan Cement, the Fauji Cement and some others followed by auto shares on the reports of higher dividend for the year ended June 30, 2005.

Trading on September 12, resumed on a steady note but the investors played on both sides of the fence amid alternate bouts of buying and selling ahead of the board meetings of some leading companies, including the Pakistan Oilfields and the Attock Petroleum.

As a result brokers kept rolling their positions from high-profile counters to where the potentials of quick gains were sure after or prior to the dividend announcements.

Reports that the Pakistan Oilfields had announced a higher cash dividend but skipped the widely rumoured bonus shares briefly affected the broader market as was reflected by a modest decline in its share value on post-dividend selling.

A final cash dividend of 50 per cent by the Attock Petroleum and a final cash of 125 per cent sans widely expected bonus shares seemed below the market expectations as its share value suffered a decline of Rs6.65 on hasty selling. It already, had paid interim bonus shares at the rate of 33.33 per cent. The cash dividend of 20 per cent plus the bonus shares of 10 per cent by the PNSC, 30 per cent cash and 25 per cent bonus by the Cherat Cement were also well-received.

But after the mid-week, leading shares came in for active support and finished with good gains and so did some others including, the Cherat Papersack, Dawood Lawrence, Shabbir Tiles, Jahangir Siddiqui Capital Market Fund, Thal, Attock Cement and the Ghandhara Nissan in post-dividend trading.

The market appeared to be in a consolidation phase, although some analysts claimed that it was still in an overbought position.

Some best dividend news, notably from the Pakistan Petroleum, and the OGDC were yet to be announced possibly during the current week and as the market talk goes their payouts could well be beyond expectations.

But some others said that the heating up of the political scenario after the Opposition’s general strike last Friday and a loud whispering about possible changes in the ruling elite though denied by some top leaders could take its toll in the form of pruning.

The next few weeks may not be crucial for future market direction but certainly warns of some negative fallout of the current manoeuvring, analysts said adding the dividend-linked rally may not last long in the developing scenario.

The cement scrips, notably the low-priced among them came in for active support partly on reports of higher exports and partly on expectations of enhanced dividend for the year ended June 30,2005. The D.G. Khan Cement, the Fauji Cement and some others were leading among them.

The current favourites in banking turned in a mixed performance as some of them attracted profit-selling at higher levels under the lead of National Bank. But the Bank of Punjab and the MCB finished with extended gains on renewed short-covering.

Plus signs again dominated under the lead of Shell Pakistan and Unilever Pakistan, Adamjee Insurance, Artistic Denim, Lakson Tobacco, Millat Tractors, Aventis, Dawood Hercules, Shezan International, Wyeth Pakistan, Artistic Denim, and Pakistan Refinery.

Prominent losers were led by the Treet Corporation, respectively. Others to fall sharply were the PSO, the National Refinery, the Pakistan Cables, the National Foods, and the Attock Petroleum.

FORWARD COUNTER: Trading on this counter remained mixed amid alternate bouts of buying and selling. While the National Bank, the D.G. Khan Cement, the Nishat Mills, the Pakistan Petroleum, and some others rose, the PTCL and the OGDC among the leading fell on late selling.

—Muhammad Aslam