A GENERAL consensus exits among economists that the moderate inflation helps in promoting economic growth, unlike high inflation that creates uncertainty and hampers economic performance. This consensus raises an interesting policy issue of how much of inflation is too much; that is, how much inflation impedes economic growth?

A GENERAL consensus exits among economists that the moderate inflation helps in promoting economic growth, unlike high inflation that creates uncertainty and hampers economic performance. This consensus raises an interesting policy issue of how much of inflation is too much; that is, how much inflation impedes economic growth?

This study follows Khan and Senhadji (2001) methodology and exclusively focuses on Pakistan and suggests a point estimate of threshold level as opposed to a range. Several studies have estimated a negative relationship between inflation and economic growth. Nevertheless, some studies have accounted for the opposite.

Thirlwall and Barton (1971), in one of the earlier cross-country studies, report a positive relationship between inflation and growth in a cross section of industrial countries and a negative relationship in a cross section of seven developing countries.

Gillman et al. (2002), based on a panel data of Organization for Economic Cooperation and Development (OECD) and Asia-Pacific Economic Cooperation (APEC) countries, indicate that the reduction of high and medium inflation (double digits) to moderate single digit figures has a significant positive effect on growth for the OECD countries, and to a lesser extent for the APEC countries.

They further add that the effect of an expected deceleration of inflation might only be observed when the world economy is not facing a sudden growth rate deceleration due to shocks. If there are no such shocks, a reduction in inflation rate can produce considerably higher growth rate. Similarly, Alexander (1997) finds a strong negative influence of inflation on growth rate of per capita GDP using a panel of OECD countries.

Fischer (1993) reports that inflation reduces growth by reducing investment and productivity growth. He further notes that large budget surpluses are also strongly associated with more rapid growth, through greater capital accumulation and productivity growth.

Ghosh and Phillip (1998) by covering IMF member countries over 1960 to 1996, found that at very low inflation rates (less than 2-3 per cent) inflation and growth are positively correlated. However, they are negatively correlated at high level of inflation.

Similarly, the empirical results of Nell (2000) suggest that inflation within the single-digit zone may be beneficial, while inflation in the double-digit zone appears to impose costs in terms of slower growth.

Bruno and Easterly (1996) find no evidence of any relationship between inflation and growth at annual inflation rates of less than 40 percent. They find a negative, shorter to medium term relationship between high inflation (more than 40 percent) and growth. Furthermore, they report that there was no lasting damage to growth from discrete high inflation crises, as countries tend to recover back toward their pre-crisis growth rates.

Mallik and Chowdhury (2001) conducted cointegration analysis of inflation on economic growth for four South Asian countries (Bangladesh, India, Pakistan and Sri Lanka) and report two interesting points. First, inflation and economic growth are positively related. Second, the sensitivity of inflation to changes in growth rates is larger than that of growth to changes in inflation rates.

Mallik and Chowdhury (2001) conducted cointegration analysis of inflation on economic growth for four South Asian countries (Bangladesh, India, Pakistan and Sri Lanka) and report two interesting points. First, inflation and economic growth are positively related. Second, the sensitivity of inflation to changes in growth rates is larger than that of growth to changes in inflation rates.

The seminal work of Khan and Senhadji (2001) suggests that there is a threshold level of inflation in the relationship between output growth and inflation. They not only examine the relationship of high and low inflation with economic growth but also suggest the threshold inflation level for both industrialized and developing countries. They conduct a study using panel data for 140 developing and industrialized countries for the period of 1960-98.

Their results strongly suggest the existence of a threshold beyond which the inflation exerts a negative effect on economic growth. In particular, the threshold estimates are 1-3 per cent and 7-11 per cent for industrial and developing countries, respectively.

The literature review does suggest a negative relationship between inflation and economic growth. However, as a motivation, it is imperative to observe the relationship through visual examination.

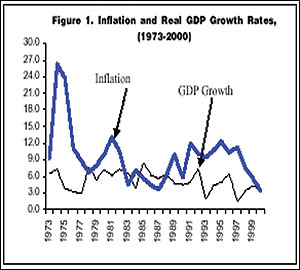

Figure 1 illustrates the trend in inflation and GDP growth rates of Pakistan. The figure somehow indicates an inverse relationship between both these variables. As illustrated in the figure, growth rates remained below five per cent until late 1970s during which inflation remained mostly double digit. Another double-digit episode of inflation was in the 1990s during which the growth performance remained dismal.

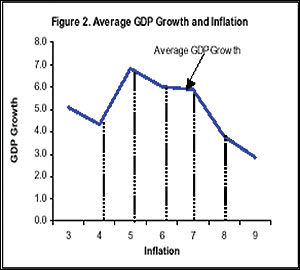

However, for a more precise picture, it is worthy to understand the historical nature of relationship between the two variables. For this purpose, whole sample (1973-2000) was reduced into few observations (in Figure 2). How did I arrive on these observations?

First of all the range of inflation was chosen from the sample (minimum and maximum levels of inflation in the given sample). Within this band of inflation, the average GDP growth rates were calculated against each linear level of inflation; for example, what was the average value of GDP when inflation rates were 3 percent during the period (1973-2000) and so on.

Figure 2 shows that the positive relationship between GDP growth and inflation remains dominant up to seven per cent inflation; and beyond that level there is a negative relationship. This suggests that the threshold level is roughly around seven per cent that may affect economic growth.

This simple analysis suggests that inflation has a negative effect on economic growth. Here, policymakers would be interested in a threshold level of inflation above which inflation adversely affects economic growth while below that level inflation is favourable for economic growth.

The estimates of causality test, an application of threshold model and finally its sensitivity analysis using country data of inflation and output growth suggest the following finds:

The Granger Causality test defines causality direction from inflation to economic growth and not vice versa (uni-directed). The threshold model estimation recommends nine per cent threshold inflation level for economic growth in which Inflation is inimical for economic growth.

The sensitivity analysis, conducted for the robustness of the model, also suggests the same level of threshold inflation. The empirical analysis suggests that the inflation below the estimated level of nine per cent is conducive for economic growth.

The result might be useful for policy makers in providing some clue in setting an optimal inflation target. However, this study does not estimate that level of inflation that is too low for economic growth; indeed this calls for further research on the topic.

( Extracts from a State Bank working paper on “Inflation and growth”)