THE crucial importance of saving and investment for sustainable economic growth is universally recognized. A developing country in its very early stage has low income and domestic saving constraint. This can be eased by external resources supplementing domestic resources.

As the economy takes off, increased incomes enhance the capacity to save and if used for actual saving, this sets in motion a virtuous circle of increased income resulting in increased saving and investment, leading to further increase in income.

After some time, this enables the economy to become self-reliant, not needing the crutches of external resources.

Pakistan is perhaps unique not to conform to this normal economic phenomenon with the least hope of becoming self-reliant in foreseeable future. In recent years, the process seems to have been reversed, as higher growth rate, instead of resulting in increased domestic saving, has been accompanied by a declining rate of domestic saving and greater dependence on external resources which are now more in the nature of external debt liability.

Tall claims of authorities of having broken the begging bowl apart, external debt, in spite of large write off in the wake of 9\11, had gone up from $32.14 billion in 2000 to $34.04 billion in 2005, as of end-June. During this period, public and public guaranteed debt increased from $28.80 billion to $31.08 billion.

According to the annual report of the State Bank of Pakistan, FY 05, Vol. I, Review of the Economy, (SBPRE):

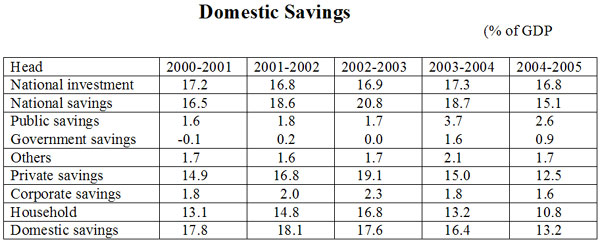

“In contrast to the preceding year, the FY 05 growth is derived substantially from a sharp rise in real private consumption as much as continued robust growth in investment. It is important to note here that the rise in real private consumption is not necessarily a negative indicator for the economy-consumer led demand has proven to be potent engine of growth in many countries and, more importantly, investment growth also remained strong in FY 05. However, the fact that a sharp drop in savings parallels the rise in consumption raises a note of disquiet in FY 05; national savings have been on a decline, in nominal prices, for the first time in six years.”

“It may be noted that despite the rise in nominal investment during the preceding three years, the investment to GDP ratio has remained stagnant in recent years, continuing to hover around 15.5 percent in the last three years. While the decline in public investment as a percentage of GDP is consistent with the increasing importance to the private sector, the absence of a corresponding acceleration in private investment is disappointing. The growth in private gross fixed investment this year was much lower than expectations and does not conform to the behaviour of other components that form the investment goods basket.”

In contrast to household savings, corporate savings witnessed a positive growth of 8.7 percent during FY 05 on the back of improved profitability amidst domestic demand. However, the small positive contribution was unable to offset the aggregate negative impact of other components of national savings.”

“On the demand side, the economy experienced a sharp climb as a result of soaring private consumption expenditure in FY 05 for the second year in a row.”

Consumer credit has certainly contributed to increased private consumption. The major focus which induced the State Bank to encourage consumer financing was (1) to give the economy a demand-pull boost given that it had been in the clutches of a decade=long recession, (2) to enable banks to diversify their loan portfolios in a low interest rate environment; and (3) to provide the middle class, the backbone of the economy, an easy access to bank credit.

During FY 05, consumer credit registered an expansion of Rs84.7 billion as compared with an increase of Rs45.9 billion in FY 04. Unlike FY04, when the growth in consumer finance was led by personal loans, during FY 05 auto loans and housing finance have also contributed significantly in the growth of consumer finance.

At the end of FY05, outstanding bank advances by way of consumer finance was of the order of Rs213.8 billion, of which Personal Loans accounted for Rs.91.9 billion; Transport, Rs66.1 billion; house building, Rs29.0 billion; credit cards Rs19.5 billion; consumer durables, Rs2.4 billion and Others Rs4.9 billion. During FY 06 till November, consumer lending expanded by Rs38.7 billion. During FY 05, increase in consumer credit accounted for only 16 per cent of the increase in and 2.3 per cent of the absolute amount of private consumption expenditure.

What matters more is the anti-saving stance of economic policies pursued in recent years and this has impacted household saving more. One of the basic objectives of monetary policy has been to help keep the cost of servicing of domestic public debt low and this has been to the great disadvantage of the saver. This has particularly adversely affected the return to the saver, which has been negative in real terms in a big way.

This resulted, among other things, in net outflow from small saving schemes to the tune of Rs44.9 billion during FY 05 as against an inflow of Rs1.6 billion in FY 04, Rs126.2 billion in FY03 and Rs84.9 billion in FY 02. Bank deposit holders have been hit really hard.

During FY 05 as against the inflation rate of 9.3 per cent, the average return on bank deposits was no more than 1.8 per cent meaning a negative real rate of return of as much as 7.5 per cent.

According to the State Bank Monetary Policy Statement for January-June 06, interest rates have become positive as the average lending rate during July-November 05 rose by 1.56 per cent to 9.77 per cent. At the same time the average return to depositors rose by only 0.52 to 2.4 percent. Adjusted for the withholding tax of 10 percent, this actually comes to 2.13 per cent.

The banking spread between the two rates increased by 1.04 percent to 7.4 percent. The annualized consumer price inflation was 8.4 per cent during July-December 05, somewhat down from 8.8 per cent in the corresponding period last year.

The rate of return to depositors thus continues to be negative in real terms and was so at 6.7 percent in the current year. The overall rate of return does not indicate the position of small deposit holders, who get nothing even in nominal terms and lose the value of their capital to the full extent of inflation when they maintain the minimum balance required by banks. If not, they are subjected to a hefty service charge on a monthly basis, which can wipe out their meagre balance in no time.

The small depositors are moving out of the banking system. The total number of personal deposits of less than Rs50 thousand, the current nominal per capita income (MP) being Rs43 thousand, declined from 12.8 million accounts with Rs212.5 billion in June 02 to 11.4 million accounts with Rs208.9 billion in 05. They represented 7.5 percent of the population in 05 as compared with 8.9 per cent in 02.

The need for stepping up saving in all sectors of the economy cannot be over emphasized. Corporate savings can be increased, apart from enhancing retained earnings by the existing corporate units, by increasing the size of the sector by incorporating new units. The establishment of broad based corporate business units is a very sad story. The recent boom conditions in the stock market should have encouraged listing of new companies, but this normal phenomenon is conspicuously absent.

Interestingly enough, instead of increase, the number of listed companies this has declined. In 1998, there were 547 private non-financial companies listed at the Karachi Stock Exchange and by 02 this was down to 481. A major factor inimical to the growth of broad-based corporate bodies is the cheap and easy availability of bank credit. Hence, the mostly closely held family controlled business units.

It is time there was an objective appraisal of credit policy from the point of its impact on the structure of financial institutions, particularly the capital market. Policies, if at all, appropriate to the conditions in the middle of the last century when private capital was almost non-existent are no loner valid when, now, there is plenty of private capital around.

The first obvious step should be to gradually revert to the old debt equity ratio of 60:40, if not the ideal 50:50, from the current general ratio of 70:30.(For housing finance this is 85:15) In bank credit, as a matter of policy, preference should be given to those borrowers who maintain a higher proportion of equity. In any case, household saving has to provide the bulk of domestic saving. The trend in household saving has been reversed. The decline has been both in quantum of saving from Rs812 billion in FY03 to Rs710 billion in FY 05 and its ratio to GDP from 16.8 per cent to 10.8 percent over this period. This should have rung alarm bells for the authorities, but no such concern is visible and it is “All is well,” so long as external resources are available to meet the current national needs. This is a myopic view.

First, there should be an in-depth objective analysis of the basic causes of the declining household saving at a time when the economy has a robust growth rate. This suggests that there has been something fundamentally wrong. The fact is the actual ground realities are not reflected in official statistics.

For the first time, the SBP report has touched on this vital subject in a Box, entitled, “gaps, weaknesses, infrequencies and lags in the Statistical System.” It is hoped that this official recognition of the problem would lead to some improvement allowing realistic assessment of the economic problems.

The basic reason for the low and declining household savings is the mal-distribution of income and wealth and its concentration in a few hands. As a result, in Pakistan the middle class, which is the backbone of society and an important source of stability, is being eliminated and pushed down below the poverty line.