QUITE a number of low income developing countries have reaped the benefits of external debt booked by them at the initial stage of their borrowings which eased up their position on huge trade and fiscal deficits, thus fostering higher economic growth rate.

QUITE a number of low income developing countries have reaped the benefits of external debt booked by them at the initial stage of their borrowings which eased up their position on huge trade and fiscal deficits, thus fostering higher economic growth rate.

However, after sometime, these countries started experiencing diminishing returns on investments with the increasing inflow of foreign loans. Consequently, economic growth rate also started receding due to an overhang of external debt. The debt burden of these countries could no longer match their repaying capacity.

A major share of the benefit accruing from investment projects started drifting to foreign creditors / funding agencies in the form of debt servicing. This in turn impacted adversely both domestic and foreign investments. It has now become difficult for a majority of low-income economies with excessive debt burden to achieve Millennium Development Goals within the stipulated time.

Increased resources deployed through external borrowings ensure sustainable economic growth rate only up to a certain level and thereafter additional injection of resources in the economy fail to boost growth rate unless a balance is maintained between quantum of debt servicing and investment on development of infrastructure and human capital.

Here the question arises as to how to measure this marginal level or threshold of external debt up to which speeded growth of economies is ensured? This can be done by applying internationally established parameters viz. size of external debt not to increase 50 per cent of GDP and its ratio to exports to remain within the range of 100-105 per cent.

However, these equations hold good only if external debt foster growth via its effect on how efficiently overall resources of a country are used and private investment is not discouraged at any point of time. It generally happened in case of heavily debt burdened low-income developing countries that, due to absence of fiscal incentives, investment by both domestic and foreign investments started receding. The momentum of economic growth rate slowed down in view of government’s inability to carry out important structural and fiscal reforms needed for growth environment.

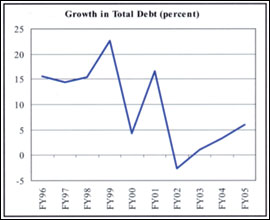

In case of Pakistan, external borrowings stimulated the economy during the period from mid-seventies to late eighties. The trade and fiscal deficit was contained at lower level to some extent and at the close of eighties external debt along with foreign exchange liabilities had stood at $22 billion. The abrupt increase in fiscal and trade deficit which persisted until late nineties, the total external liabilities had exceeded US$ 42 billion. It impacted adversely not only budgetary position but also made average growth rate hover around three per cent during the second half of nineties.

Debt servicing had a share of 11.6 per cent in total revenues until early eighties, but at the close of nineties it reached the level of 64 per cent. Of the total revenues, only one-third was available for defence, social sector and civil administration.

During this period, export earnings remained within the range of $9-10 billion. These were too little to meet cost of import bills having liability range of $10-12 billion plus debt servicing, which remained around $5-6 billion per year. Hence external borrowings continued to grow and by end of 90’s it was around 92 per cent of GDP. The quantum leap in debt servicing caused a large fiscal deficit, which by 1998-99 was seven per cent of GDP. This, in turn, had adverse repercussions on social and physical infrastructure development.

The per capita income also remained stagnant at $450. The overall saving and investment ratio to GDP at 19-20 per cent in early nineties, came down to 15 per cent and still hovers around this ratio. The country experienced worst foreign exchange reserves position until 2001.

However 9/11 proved a blessing in disguise. An abrupt rise in inflow of workers’ remittances and rescheduling of debts and relief by donors resulted in manifold increase in country’s foreign exchange reserves.

Robust foreign exchange reserves position reduced vulnerability of the exchange rate and provided some stability to country’s currency value. However on domestic front, despite structural adjustments, economic growth rate remained stagnant until 2003 mainly due to neglect of investments on social sector, infrastructure and human capital development.

Immediately thereafter, the improved law and order situation and the incentives announced for investment attracted not only fresh direct foreign investment but also an abrupt rise in investment from domestic sources was noted both in manufacturing and service sector.

Further, privatization, on the one hand, took away sizable financial burden from public sector and on the other hand a lot of improvement was recorded in working efficiency of these banks. As a result, after a long time, the country could give a growth rate of 6.8 per cent and an abrupt rise in per capita income.

However, at the same time soaring import bill, which was mainly due to steep rise in international oil prices not only substantially increased the trade deficit, but also brought up overall inflation rate to nine per cent. Snowball effect of curbing inflation through rise in interest rate would harm the growth economic process. The future projections for economic growth rate will have to be revised downwards.

Apart from the normal issues, the greatest shock to the economy has come from the earthquake- a colossal liability of around $10—15 on account of loss of private and public assets. These assets need to be replenished on priority basis.

The loss of these assets would deprive both public and private sector sizeable revenue. The size of GDP is also likely to be squeezed. Apart from this immediate loss to the economy, entire Public Sector Development Programme allocations will have to be slashed to reallocate funds for financing reconstruction and rehabilitation programme.

The size of financial assistance/relief pledged whether in kind or cash by different countries so far is hardly four per cent of the funds actually needed for the purpose.

It is more likely that the financial relief so far pledged both by internal and external donors would be just enough to provide immediate relief to earth quake victims and to pay financial compensation to the families who have lost their dear ones as announced by the government.

For reconstruction and rebuilding lost/damaged assets in affected area, the country will have to rely on long term internal and external borrowings. OIC and Islamic Development Bank have already pledged financial assistance of $251.6 million including $1.6 million grant.

Based on experience under such circumstances obtaining in other parts of the globe, World Bank and Asian Development Bank may come up with long-term funding at zero rate of interest but with service charges with a long grace period on its repayment. Despite these concessions, if extended debt servicing of the same would bring additional burden on national resources and external debt ratio, now at 62 per cent of GDP, would again go up.

In this regard, the best approach for Pakistan would be to make an appeal to existing creditors as well as to donors to write of 15 per cent of the existing loans or at least waive interest altogether on all loans and extend grace period by 10 years in all cases.