Basing regulatory action on Federal Bureau of Statistics( FBS) reported statistics can be dangerous.

Basing regulatory action on Federal Bureau of Statistics( FBS) reported statistics can be dangerous.

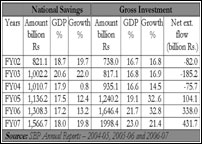

The FY04 SBP Annual Report quoted the FBS figure of National Savings as Rs988 billion; it was revised to Rs1,101 billion in SBP’s FY06 report and then to Rs1,136.2 billion in its FY07 report. As a consequence, the negative 4.5 per cent growth in the National Savings in FY04 became positive growth of 12.4 per cent in the FY07 report.

In spite of this jugglery, low savings rate in recent years remains the ongoing problem, for which banks carry bulk of the blame. Besides their business strategies, they need to watch the trends in macro indicators i.e. growth in domestic savings, saving-investment gap, trade deficit, and the level of escalation in reliance on external resources, given our growing isolation in international financial circles.

In view of the worrying growth in population, investment, particularly in its industrial base, must grow to boost production and employment, but the gap between savings and investment is expanding, making the economy vulnerable. Reason: banks’ overstretched asset bases in marginally productive sectors (15 per cent of total in consumer credit) that reflect poorly on their lending choices.

In recent years — prelude to the demise of ‘globalisation of trade and investment’ — we got accustomed to relying on foreign direct investment (FDI) flows (Rs874 billion from FY 05 to FY07) to remedy our shocking inability to save, realising little that, besides the impending global economic chaos, events on the country’s western borders were bound to worsen Pakistan’s risk perception abroad and stop foreign investment inflows.

The SBP annual report 2006-07 pointed to this trend, noting that “the large saving-investment gap (five per cent by FY07) results in accumulation of external debt and puts burden on the balance of payment (BoP) in terms of mounting debt-servicing. As a result, the country seeks more external debt to service its debt obligation and falls into a trap.” This vulnerability could prove devastating unless managed skilfully.

Bank regulators and economy managers (both repeatedly warned by observers) did not notice that after FY03, saving-GDP ratio had become virtually static as banks’ branch networks serving the rural areas contracted, supposedly, to improve banks’ efficiency and profitability. The trend hampered saving as well as documentation of the economy while fraudsters like ‘Double Shah’ flourished.

The network of the Central Directorate of National Savings (CDNS), which, according to its MD, has the lowest operating cost hasn’t been expanded to plug the gap created by closure of bank branches, nor has the employee strength of the CDNS expanded to benefit from the savings flow that has doubled after revision of profit rates. Instead, penalties being imposed on shifting investment into higher yielding securities are frustrating the savers.

Accounting records of CDNS are still maintained manually. The worst part is that no branch is adequate in terms of its physical infrastructure or frontline staff, forcing investors, mostly aged individuals, to spend hours for their turn in uncomfortable surroundings. To reduce a bit of this pain, investors can’t shift their account from one CDNS branch to another.

How, in this setting, will the CDNS collect its targeted Rs150 billion during 2008-09, is anybody’s guess because this is hardly the way to go about encouraging saving and attracting saver funds into NSS schemes to limit the government’s reliance on the inflation-fuelling borrowing from SBP, or from external sources.

Banks did no better. Spurred by suspicious official CPI estimates, between 2004 and 2006 they lowered profit rates on deposits to a point that rendered saving unattractive. The trend worsened due to an inapt lowering of returns on NSS. Increasingly, it made sense to borrow at low mark-up rates, and consume — a disastrous setting in the newly heralded era of floating interest rates — or invest in equities for which savers had no risk estimation capacity.

Not surprisingly therefore, and in spite of the experiences of 2003 and 2005, on April 18, KSE index reached its zenith when stock indices globally were in a free fall. It reflects on how badly banks failed to make citizens prudent savers. Given their huge (Rs240 billion) stake in mutual funds, they now worry about the fallout from removal of the lower lock on share prices scheduled for October 27.

Few banks have noted their failure and made amends by innovating deposit products that fairly reward savers and also commit to provide temporary overdraft, if needed by them — a good start though not on an encouraging scale. Banks still haven’t accepted that returns on equity of 40 per cent (thrice the CPI at the time) or more that they earned, reflected social irresponsibility, not high resource productivity.

The coming months will prove that countries with a risk perception as weak as ours must fend for themselves. It implies relying on domestic savings to expand industrial and social infrastructure by setting lending and investment priorities that optimise economic (not jut monetary) returns there from. So far, banks haven’t appreciated this role that they must play in fulfilling this crucial obligation.

Thus far, they erred by disregarding the quality of assets represented on their balance sheets merely by numbers. Over-satisfaction with numbers and low concern for the risk associated with these assets and their realisable values was imprudent. I know of bankers who thought it naive to ask individuals taking (the highly profitable) ‘personal loans’ to disclose the use of loan funds—something highly imprudent.

Now banks face a big multi-faceted challenge; they must devise attractive saving products and prioritise deployment of savings in key economic sectors that boost exports or cut imports to build the sort of exchange reserves that steadily strengthen the rupee. The aim isn’t achievable without focused market research — virtually non-existent in banks — linked to bank-specific market niches and risks. It is time to build this capacity.