Pakistan Railways’ miserable financial position is no secret. It has been incurring losses since 1972-73 reaching a whopping Rs11 billion during 2006-07 which is likely to be higher during the next year. The Railways’ financial problem number one remains the unbridled overdraft which started with Rs74 million in 1975-76 and swelled to Rs26 billion at the end of June, 2008.

Pakistan Railways’ miserable financial position is no secret. It has been incurring losses since 1972-73 reaching a whopping Rs11 billion during 2006-07 which is likely to be higher during the next year. The Railways’ financial problem number one remains the unbridled overdraft which started with Rs74 million in 1975-76 and swelled to Rs26 billion at the end of June, 2008.

Add another Rs7 billion which the Railways owe to the employees’ provident fund and to private parties in the name of security deposits etc. and there is a massive gap of Rs33 billion in its cash position. And about Rs20 billion must have been sunk as interest expense over the last 15 years or so.

Unfortunately all this adds up to a staggering liability of Rs53 billion to the nation. It is open to imagination what Rs53 billion could have done to change the fate of the Railways if these resources were available as additional development finance that could bolster railways’ earning capacity and handsomely improve quality of its service rather than a wasteful cost of inefficiency, mismanagement and corruption.

The most disturbing thing is to realise that railways’ overdraft was simply avoidable. As a matter of fact its financial system is so designed that there is no room for an overdraft. There should normally be a credit balance at the end of a financial year which roughly represents employees’ and other parties’ monies lying in Railways’ account. Unforeseen events, if any, implying cash crunch should be dealt with as such on their own merit but not allowing the situation to drift into a point of no return as is at present.

Over the last about 35 years of rampant overdraft, there are two periods of five years each when the Railways were in fact run without an overdraft. Both these periods, 1979-80 to 1983-84 and 1988-89 to 1992-93, stand out prominently in terms of financial discipline and performance. All basic financial indicators corroborate that.

There were three basic ingredients in the recipe for this performance. First, ‘Integrated Financial Management’ was introduced and consolidated midway in 1979-80. This approach to financial management ensured superb budgeting, robust internal control mechanism and focused on cash monitoring. Financial management was at its best marked by a high degree of professionalism and impeccable standard of integrity. The results were credit balances, no unauthorised overdrafts and minimised losses.

Second, integrated financial management was reinforced by additional initiatives as part of a wider agenda of financial management reforms in the public sector and to support germination of culture of corporate governance in the Railways. Some elements of accrual accounting were introduced with positive results. Formats of financial statements (balance sheet and profit and loss account) were revamped to conform to generally accepted accounting principles for commercial organisations. Monthly financial reviews were computerised which permitted timely managerial decision making. Financial reporting thus became more transparent, prompt, complete and reliable.

Third, professional financial management was instrumental in promoting the concept of corporate governance in railway administration. As a first step, the government was moved to accept a priori the distinction between ‘commercial railway’ and the ‘social railway’. Some worst loss making passenger services were compensated as Public Service Obligation (PSO) by the government and the railway administration was charged with the bottom line responsibility for commercial services implying greater transparency and accountability in the process of financial results.

This led to a gradual and consistent improvement in the bottom line of railway operations. Operating surpluses in 1991-92 and 1992-93 were thrown up for the only time in the last 28 years. Similarly, net loss was reduced to less than Rs1 billion in 1992-93, the lowest figure in the last 27 years. The corporate financial forecast prepared at the time projected the Railways to break-even by 1993-94. But the events that were to unfold subsequently rendered this as a dream gone sour. The unmatched phase in the Railways’ financial history had ended.

One aberration propping towards the end of 1992-93 sparked the beginning of a relentless phase in the Railways’ overdraft. Unrealised traffic earnings and other receivables which historically stood at about six per cent of total earnings abruptly jumped to almost 11 per cent in 1992-93 causing an unauthorised overdraft which grew like a wild fire thereafter.

The period that followed can best be described as ‘free for all’. The integrated financial management system nurtured so well on two occasions in the past collapsed completely. Financial management literally ceased to exist on the Railways. The Railways administration appeared busy in pursuits other than running the system. The scale at which the actual expenditure exceeded the budget, the speed with which the overdraft swelled, the rate at which the unrealised earnings increased and the pace at which net loss bulged during this period bears a clear testimony to the fact that railway was thrown in a bottomless pit where all systems had failed to function.

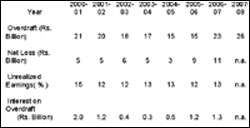

Overdraft literally exploded from Rs1.5 billion in 1993-94 to Rs19.7 billion in 1999-00 and all other indicators went haywire. Expenditure exceeded the budget like never before. Net loss jumped from Rs2 billion to Rs7 billion and unrealised earnings shot up from 10 per cent to a colossal 18 per cent.

A changed railway administration at this juncture inherited a bleak legacy but had a totally myopic perception of the Railways’ problems and was handicapped with a single track approach to tackle them. The first two years of this period saw a surge in the overdraft. The new administration at the behest of the finance management got somehow afflicted with an obsession to ‘repay’ the debt to the State Bank. A bizarre agreement was signed between Finance Ministry, Railways and the State Bank. Railways were to ‘repay’ Rs250 million every month (Rs3 billion per year) to the State Bank whereas they were in no position to pay back even a single rupee. The government financed all shortfalls of the Railways operating expenses and debt service through subsidies and met the entire development expenditure- all adding up to Rs21 billion in 2006-07.

Looking at the table, whatever little dip that appears in the overdraft in some of the years (projected as ‘repayment’ by administration) is actually attributable to amounts of grant-in-aid overpaid to the Railways for a number of years and development funds remaining undisbursed either due to constraint of absorption capacity or deliberate maneuvering.

Audit report for 2004-05 mentions an amount of Rs6.33 billion on account of overpaid grant-in-aid in previous three years alone. The circuitous route was adopted to ‘show’ repayment of overdraft when the Railways had no capacity to do that. The newspapers on April, 2004 did carry a half page ad claiming repayment of Rs4 billion by the Railways to the State Bank. If the amount overpaid is ever adjusted by the government, the overdraft will rebound to its true level.

Of late, confusion has been further added to the issue by treating the overdraft as a ‘long-term liability’ and budgeting its ‘repayment’. That was neither correct in principle nor required when the government was bearing the entire brunt of repayment and the Railways’ ability to do that was not in sight for many years to come.

If the finance ministry had decided after all to pick up the tab then a simpler and direct way should have been adopted. The government should have directly settled the Railway’s account with the State Bank the way it settles its own liabilities and treated the amount involved as the government investment in the Railways. This action could have subjected railway authorities to conditionalities as to its performance and behaviour in future and obviated distortions in the financial statements.

The Railways’ net loss climbed to new heights during 2005-07 in spite of the reduction of almost 15 per cent in employee strength over the period with its attendant effect on the staff cost. It is also a great pity that an investment of no less than Rs50 billion poured into the Railways system between years 2000 and 2008 could not produce any positive results. The net loss, on the contrary, doubled and this casts serious doubts on the proper, meaningful and judicious utilisation of a large volume of development funds.

With such massive losses and debilitating finances have the Railways reached a point of no return? Answer is probably not. Even keeping its character as a state-owned enterprise and with a policy of adaptation, the Pakistan Railways can perform. The prime need is to take a searching look into the basic parameters encompassing macroeconomic framework and policy, organisational structure and size, management outlook and practices and not the least the information systems. It is imperative to ascertain objectively as to why and how the Railways actually failed to perform over the years in relation to these parameters. Viable and pragmatic solutions will not be hard to find.

Reform is warranted but lessons must be learnt and half baked and costly experimentation needs to be avoided. Where an aspirin can work it is wise to shun expensive and complicated surgery. One thing that stands out clearly in the turnaround of the Railways is that certain trends that got entrenched over time must be reversed and the reversals sustained. If that can be ensured, the Pakistan Railways can hope to deliver.