THE strong weekend rally has reinforced investors’ perceptions of continued bull-run on strong institutional and foreign buying at least till next month as both the fair values of some of the leading scrips and talks of higher expected payouts would not allow leading market players to sit on sidelines.

THE strong weekend rally has reinforced investors’ perceptions of continued bull-run on strong institutional and foreign buying at least till next month as both the fair values of some of the leading scrips and talks of higher expected payouts would not allow leading market players to sit on sidelines.

Both the current index level and the price flare-up on selected counters reflect that the market could explore new highs in coming weeks. Fresh increase of 484.3 points in the KSE 100-share index and Rs142 billion increase in the market capital over the week, eloquently speaks of the investors’ mind, notably institutional and foreign ones.

An idea of bull-run may well be had from the fact that investment in CFS has touched the high mark of Rs52 billion, only Rs3 billion short of the ceiling of Rs55 billion. Although financial risks are involved in the higher leveraging positions, investors are inclined to take them may be for good reasons.

The KSE 100-share index maintained its upward drive last week boosted by strong buying in leading oil and bank shares aided by higher international prices and encouraging corporate earnings.

The near-term index level of 12,000 points or above may not be an elusive goal now as analysts predict some new records both in terms of index level and single session volume as the talk of an increase in the CFS limit beyond the current Rs55 billion may turn into a reality, some brokers believe.

Essentially, it was dividend related buying euphoria confined mainly to banking and oil shares whose annual general meetings are due and there are predictions of higher payout and bonus shares.

Click to view the larger image

The month that just passed was most important for the future direction of the market and analysts believe a strong future rally could be built-up on the New Year gains.

“As goes January so goes the market,” the market's performance during last month literally fits into this old adage, they said.

But some of the leading investors are worried over the massive leveraging as the CFS figure has touched the danger point of Rs49 billion, signaling possibility of strong technical correction during the sessions to come.

However, as the best of dividend news are still in the pipeline, bulk of profit-selling is expected to be absorbed at the dips and indications are that there could hardly by a major interruption in the future market stance, some others said.

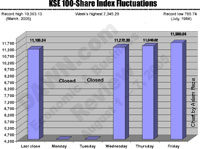

The KSE 100-share index finished the week with an extended gain of 484.3 points at 11,589.64 as compared to 11,105.34 at the fag-end of last week, reflecting that bulls are not inclined to loose their grip on the rising market.

OGDC was the top scorer in terms of daily volume followed by PTCL, Pakistan Oilfields, Pakistan Petroleum, National Bank, MCB, Bank of Punjab, United Bank and D. G. Khan Cement.

“The post-Ashura strong extended rally indicates that the next bull target could be 11,500 points before technical factors should become operative”, said a leading stock analyst Hasnain Asghar Ali adding that “the market is already in a danger zone owing to sustained run-up of about 1,800 points during the last three weeks”.

Another analyst Ahsan Mehanti said some technical factors, notably market talks of some relaxation in the operative capital value tax and withholding tax seem to have sustained the current bull-run carried through from the pre-Ashura sessions.

However, the general perception is that upcoming dividend news from the banking, oil and other sectors would continue to inspire fresh buying on selected counters and could boost the index to further higher levels.

Apart from the sustained price flare-up, other supporting factor was the advent of foreign buying on selected counters followed by strong institutional covering purchases, brokers said.

Arif Habib Ltd, Rafhan Maize, Wyeth Pakistan, Unilever Pakistan, MCB, Pakistan Petroleum, National Bank, Allied Bank, United Bank, Bank of Punjab and Pakistan Oilfields were leading among the gainers.

Losers were led by Pakistan Cables, Clariant Pakistan, Lakson Tobacco, Sanofi-Aventis, Nestle Pakistan and Clover Pakistan.

FORWARD COUNTER: Speculative issues on the forward counter also maintained their bullish outlook and finished the week with an extended gain. Major gainers were National Bank, MCB, Bank of Punjab, Pakistan Petroleum, OGDC, Fauji Fertiliser Bin Qasim and some others, which are heading towards their pre-reaction levels.—Muhammad Aslam