Since the end-1999, the State Bank of Pakistan [SBP] has been headed by incumbents hailing from the World Bank and the Asian Development Bank.

Since the end-1999, the State Bank of Pakistan [SBP] has been headed by incumbents hailing from the World Bank and the Asian Development Bank.

After Dr Ishrat Husain took over as the SBP governor, his policy was that the country should have only 20 large and strong banks, by getting rid of smaller banks. To this end, the Minimum Capital Requirement [MCR] was raised to Rs6 billion for compliance by the end of 2009. If any bank that did not fulfil the regulation, it was to be merged with another bank.

A number of small banks were allowed to be set up in the 1990s with the MCR of Rs500 million only. The close of the calendar year 2009 is still far away. But almost all the smaller banks seem to have met the above MCR target except a one or two including Pak-Saudi Bank [which is the legacy of a central banker turned commercial banker who had enlarged his interests not only in banking but also in the insurance sector in an extra-ordinary way].

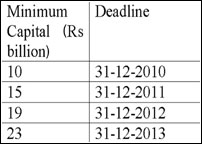

The earlier deadline for meeting MCR is still far away. But the SBP has come up with still stringent regulations under which the smaller banks are now required to enhance minimum capital to Rs23 billion by 2013. The time frame is given in the Table:.

The proposed targets can be achieved only if the after tax profits of the smaller banks grow at the following rates year-over-year and the entire amount is reinvested in the bank itself: 2010- 66.6 per cent, 2011- 50 per cent, 2012- 36.66 per cent and 2013- 21 per cent. True that the profitability of the banks has enormously increased after 2000, but can any one expect that the banks will earn such huge profits during 2010-2013? Apparently, it seems impossible. In case of the failure to meet MCR deadline, the small banks will have no option but to merge in other banks.

The question is what is the need of introducing this coercive mode of mergers.The history tells us that most of the small banks established in early 1990s are performing well. They are successfully competing with the large banks, and rendering comparatively better services and offering higher returns on deposits.

No doubt there are instances of these small banks’ failures too i.e. Prudential Bank Ltd., Indus Bank Ltd and Mehran Bank Ltd. But the fault lies with the government and the SBP in having issued licences to the undeserving sponsors in these cases.

The question also is there any guarantee that the large banks will not fail? The answer is certainly in the negative. The position of fourth largest American Bank Lehman Brothers is before us which has gone bankrupt and created a financial crisis.

The mindset of SBP governors since end-1999 has been to drive out the “small business” from the field for one reason or the other. In early 1990s, licences were granted by the SBP to small businessmen to undertake purchase and sale of foreign currency notes and coins from and to the public.

After 1999, the SBP decided to replace these small authorised money changers [AMCs] with large exchange companies with the MCR of Rs100 million. Gradually, some banking functions of making remittances etc. were also assigned to these exchange companies.

The assignment of remittance business to exchange companies was in contradiction to the policy of reducing the number of banks to 20 only, as it amounted to the enlargement of numbers of banks in some way or the other. It was only the high profile protests from the small AMCs that led SBP to devise methodology of sub-licencing to the AMCs to continue their business. Otherwise, SBP may have thrown out the small business from the field.

An important aspect which is lost sight of in the banking sector reforms is the sale of banks to foreigners. True that it results in one time inflow of foreign exchange and adds to the country’s reserves. But simultaneously, it creates permanent liability on account of remittance of profits [earned in rupees] into foreign currency. This goes on adding up with every sale of domestic assets to foreigners.

The smaller banks will not possibly be able to achieve the new stringent MCR and consequently foreigners-who are already eyeing our banking sector will eagerly purchase them. The chances of sale smaller banks to the foreigners seem real as is evident from the MCB’s sale of its shares to a Malaysian bank recently.

Apart from aggravating the problems of balance of payments, the dominance of the domestic financial sector by foreigners will give a strong leverage in the hands of the foreigners.

The SBP’s new MCR policy needs to be reviewed and reversed. It should let the smaller banks grow in the normal way. This will raise their size over time and they will become large. Any attempt to hurriedly hand them over to the foreigners will hardly serve any national cause.

The writer is a retired Additional Director/Foreign Exchange, SBP.