It does not need hindsight to come to the conclusion that it was a colossal failure of public policy during the period when President Pervez Musharraf was in charge of the country to plan for increase in the supply of electricity. The President was aware of the fact that unless the state made investments in generating additional power, the country will have to face serious power shortages. These have materialised and in the summer of 2008, the number of hours that people have to go without electricity continues to increase.

It does not need hindsight to come to the conclusion that it was a colossal failure of public policy during the period when President Pervez Musharraf was in charge of the country to plan for increase in the supply of electricity. The President was aware of the fact that unless the state made investments in generating additional power, the country will have to face serious power shortages. These have materialised and in the summer of 2008, the number of hours that people have to go without electricity continues to increase.

It is said that President Musharraf’s strategy was to concentrate on the constructions of large dams, preferably the one at Kalabagh on the Indus. There is no doubt that the President worked hard to develop a political consensus that would have made the construction of Kalabagh possible. That did not happen and later in his tenure, the President gave up the attempt leaving his administration with no contingency plan to meet the anticipated demand-supply gap.

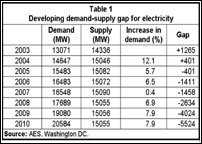

The data on supply and demand presented in accompanying Table 1 provides some interesting information. It shows a surplus of 1265 MW in 2003, three years after Musharraf had removed Prime Minister Nawaz Sharif from office. The surplus was largely the consequence of the power policy adopted by the administrations that were in charge in the 1990s. They encouraged investment in the electric sector by private entrepreneurs. But the surplus did not last beyond 2004.

By 2005, demand-supply gaps had appeared and began to increase in size as no increase in supply occurred. In 2004, demand exceeded supply by 2.5 per cent, increasing to 15 per cent by 2008, the last year of the administration headed by Musharraf. It is estimated that by 2010, the demand-supply gap will increase to almost 27 per cent of supply. It is clear that urgent action is required on the supply side.

Policy makers must find answers to two questions: One, how to take care of the shortages that are already seriously hurting the economy and causing some discomfort to the citizenry? Two, what should be the sources for generating electricity over the medium and long-term? Whatever choices are made by the government, it will have to take cognizance of the fact that it takes a long time to bring additional generation capacity into operation. In this context, the short-term strategy will have to be looked at differently from the strategy for the long-term.

At this time, individual households and small business have starting installing small generators. Somewhere between 100,000 to 250,000 have been imported and installed at cost of well over Rs30 billion. The combined output of these generators is possibly between 100 and 150 MW. This is a very expensive way to meeting the power shortage. Since a significant proportion of these are run on imported diesel fuel they are adding to the high fuel bill as well as putting an additional burden on the already strained urban environment. Also, meeting the supply-demand gap by installing generators in individual households and small business is an option available to a small segment of the population.

At this time, individual households and small business have starting installing small generators. Somewhere between 100,000 to 250,000 have been imported and installed at cost of well over Rs30 billion. The combined output of these generators is possibly between 100 and 150 MW. This is a very expensive way to meeting the power shortage. Since a significant proportion of these are run on imported diesel fuel they are adding to the high fuel bill as well as putting an additional burden on the already strained urban environment. Also, meeting the supply-demand gap by installing generators in individual households and small business is an option available to a small segment of the population.

This solution is perhaps feasible for no more than 20 per cent of the households. By further turning to their own devices for filling a function that should be provided by the state or by the public utilities operating under the supervision and regulation of the state, the rich and the well-to-do are further isolating themselves from the ordinary citizenry. They are sending their children to expensive private schools; many of them have turned to private security operators to purchase protection not provided by the police; and they have begun to purchase their second homes in the Middle East and Europe to escape from Pakistan when the weather becomes hot or the temperature of political discourse rises. Now, by installing private power generators, they have created another little island for themselves. Thus the use of private generators to deal with power shortage have all kinds of high costs, economic environmental, political and social.

How then to deal with the grim problem of power shortage given that any reasonably economic situation has a long gestation period? The only option is to buy or rent barges that have reasonably large generators installed on them. The government may quickly consider obtaining several barges and anchoring them outside. The power generated by them, say 1000 MW, could be delivered into Karachi’s distribution system. An equal amount of power could be fed into the national system for feeding the areas north of Karachi.

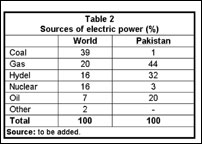

A more permanent supply situation would involve a decision on what is the most important fuel for generation given the domestic resources as well as the cost for obtaining them from the outside. In this context, the data presented in Table 2 are instructive. The table shows that Pakistan now has a very different mix of fuels for power generation when compared to the rest of the world. For the world coal is by the far the most important fuel for power generation; for Pakistan, on the other hand, natural gas is the dominant fuel for power. At one point in its history, Pakistan had an abundance of gas. However, after the construction of two vast pipeline networks, the use of gas for several different purposes has increased to the point that the reserves have been seriously depleted.

Given the possible uses of gas as a household fuel and as a feedstock for various chemical industries (including fertiliser), to use it for producing electricity may not be a good strategy. Fuel oil (most of it imported) is the second most important input for power generation, accounting for 20 per cent of the total production of electric power. For the world, the share of fuel oil is considerably smaller, only seven per cent. Given the recent sharp increases in the price of oil, Pakistan has to carefully review the fuel-for-power-generation policy it has pursued. At this point, it might be useful to take a moment to examine the dynamics that seem to be operating in the oil markets.

This is what Alexey Miller, the chief executive of Gazprom, has to say about the future of oil: “We are living in the time of a great surge in oil and gas prices: a structural shift in the market, which well end with prices at a radically new level. Fierce competition is unveiling for access to energy resource Oil price rises are linked to a major revision of long-term forecasts. They demonstrate global energy supply demand imbalance in the coming decades.” Miller believes that oil could reach $250 barrel a day next year. His arithmetic is based on continuing demand increases in the rapidly growing developing countries. “The past 10 years (1997-2007) saw China’s consumption almost double and India’s grow over 1.5 fold.”

This is what Alexey Miller, the chief executive of Gazprom, has to say about the future of oil: “We are living in the time of a great surge in oil and gas prices: a structural shift in the market, which well end with prices at a radically new level. Fierce competition is unveiling for access to energy resource Oil price rises are linked to a major revision of long-term forecasts. They demonstrate global energy supply demand imbalance in the coming decades.” Miller believes that oil could reach $250 barrel a day next year. His arithmetic is based on continuing demand increases in the rapidly growing developing countries. “The past 10 years (1997-2007) saw China’s consumption almost double and India’s grow over 1.5 fold.”

There is also the belief that the structural change in the oil market is occurring on both the demand as well as the supply side. Some experts suggest that “peak oil” – the point at which the world’s oil production can no longer be increased and begins to fall – has been reached. According to this view, oil production is peaking because the geological limits of available resources are being reached. However, this explanation does not command general support among oil experts.

The third view – in addition to the views about unrelenting increases in demand – and limits on supply – places emphasis on speculation by a large number of operators in the oil markets. This view was advanced vigorously at the summit the held in June in Saudi Arabia by a number of governments’ representatives from the countries that are large oil producers and exporters. But this explanation for the sharp increase in the price of oil misses the point that every forward purchase of oil must also be a forward sale. Also, those who don’t accept this view point out that commodities in which there is no activity by financial investors such as rice have also been rising sharply.

For strategists in Pakistan, it would be safe to assume that the period of low oil prices is gone; that the demand for the commodity will continue to increase in the rapidly growing developing economies and that this growth will more than compensate for the slow down in demand in more developed countries.

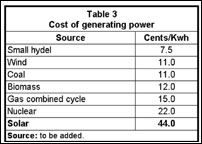

It would be prudent for the policy makers to opt for using inputs for generating power that are not under price pressure (such as domestic coal), that have an abundant domestic supply (coal and water) or that are renewable (wind and solar). In other words, the structure of electricity supply should be considerably different from the one it has today. Coal and hydro, and renewables must play a larger role in power generation than is currently the case.