THE bulls are back in the ring, and Karachi’s stock market has climbed by 18 per cent so far this year outperforming the rest of Asia and almost all major stock indices around the world.

THE bulls are back in the ring, and Karachi’s stock market has climbed by 18 per cent so far this year outperforming the rest of Asia and almost all major stock indices around the world.

After trading in the range of 10,000-11,000 for most of the second half of 2006, the KSE100 Index broke the 11,000 resistance level to close at 11,844 last Friday. Total market trading reached $6.3 billion in January and aggregated about $4 billion during the first trading week of February.

The volume of borrowings used to finance purchases of stocks in the local CFS market surged by 45 per cent to $860 million and the financing rates shot to around 19 from 13 per cent in December. The index gained 12.3 per cent in January, which was largest gain in a single month since February 2005, when it rose by 22.5 per cent only to crash in the following months. What has been behind such a rapid rise in the Index and surging volumes since the New Year began?

Some market analysts have attributed this bull run to the extension in the exemption from capital gains tax announced by Prime Minister Shaukat Aziz on January 5 while others have pointed towards the fresh buying from the foreign investors as the principal reason for the strong performance. Perhaps both the factors coincided to encourage the market to take a bullish view.

In addition, there were reports that a foreign investment bank issued a “buy Pakistan, sell India” recommendation. This was quoted out of context because there was no such recommendation made by the portfolio strategists of that bank as Pakistan is not even part of their recommended international portfolio.

Others cited Pakistan’s price-to-earnings (P/E) multiples as being cheap compared to its regional peers. But they were cheap in December and Pakistan’s market has always traded at lower P/E multiples compared to larger Asian markets. This led us to probe deeper into the market activity and trading patterns during the past few months including January 2007.

Although the foreign investors made net purchases of $110 during the first six weeks of 2007, the average daily traded volume on the Karachi Stock Exchange jumped to $412 million from an average of $212 million during December 2006. But the averages do not reveal the whole picture. On February 2, the aggregate volume reached a staggering $943 million. This indicates a massive level of short-term trading both in the official and unofficial badla markets. It appears that some local operators decided that the time was right to make a killing in a matter of days or weeks by using borrowed funds or, what the professionals would call, highly leveraged short term bets. What makes such large players so confident that they can ride on an initially small stimulus provided by foreign buying?

To some it represents a bullish sentiment and hence a reason to buy but some others attribute this to the old habit of the local speculators to take advantage of a shallow market that can fluctuate violently when “real money” flows in and the investors take delivery of the shares. Rumours of front running abound. This refers to the illegal and unethical practice of purchase of shares by a broker in anticipation of a rise in its price after a buy order has been received from a client but the broker buys the shares for his own account before the client order is filled.

Lot of easy money is believed to have been made this way. To prevent this or any other violation of law, many countries now require that the brokers record all telephone conversations of their trading personnel because it is usually quite difficult to check insider trading but there is no such requirement in Pakistan.

Leaving that side, in order to better understand the recent trading activity, it is important to highlight some important features of the market.

The ten largest companies account for about 60 per cent of the index but a much higher 85 per cent of the value traded on average. It is rather a small market and vulnerable to manipulation. Although the market capitalization is frequently quoted around $ 50 billion, it is much less in terms of the free float which is around $ 7 billion This means the shares available for trading (excluding the holdings of the government or principal owners of companies) are significantly less than what appears to be the case.

More importantly, this means that most of the foreign buying tends to be in a handful scrips and even a $20-30 million inflow can have a disproportionate impact on their prices if it is accompanied by much larger level of trading or speculation by the local players.

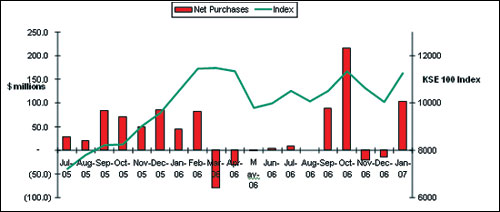

Given that the speculative trading tends to be concentrated in the shares of the companies with large weights in the index, the market index can exhibit large movements in a short period. During the last eighteen months or so, the foreign investors’ net purchases have been lumpy or sporadic as illustrated by following graph

While the foreign investors stayed on the sidelines for about six months after a sell-off during March-April 2006, they came back in September and October for some buying but remained net sellers during the rest of 2006. As usually is the case in stock markets around the world, the second week of January saw fresh buying by the foreign investors who bought about $29 million of stocks in a matter of four days.

At the same time, the CFS (continuous financing system), that represents borrowings for the purchases of stocks by local brokers, went up by $22 million on just one day and by $41 million during the first two weeks of January. For the entire month of January, foreigners’ net purchases were $103 million but the CFS outstandings went up by $208 million. The index rose by about 400 points (or 3.6 per cent during the first two weeks) and finished the month up 1231 points or 12.3 per cent.

However, even if one takes into account the aggregate volume of foreign buying and increase in CFS outstandings (that is, $311 million), there is only one explanation of the aggregate volume of $6.3 billion that was traded during the whole month of January. There has been a phenomenal increase in day trading and unofficial badla market activity. This would be hard to sustain as was experienced in the previous market crashes during March 2005 and May-June 2006.

Here it relevant to note that the cost of borrowing (or badla) rose to 18-19 per cent in January 2007 from about 11-13 per cent in the previous month and some market reports suggest that the local mutual funds have been taking profits during the first week of February as they anticipate correction in the coming weeks.

Now let us look at what activity took place in some of the biggest stocks that moved the whole market since the beginning of the New Year. The ten largest shares in the index shot by 10-30 per cent in a matter of few week, led by National Bank of Pakistan (NBP), Pakistan Telecom (PTC), Muslim Commercial Bank (MCB), Pakistan State Oil (PSO), Bank of Punjab (BOP), Pakistan Petroleum (PPL) and Oil and Gas Development Co. (OGDC)) that rose as follows:

Per cent Rise in CFS

rise outstandings

Jan. 1 – Jan. 31 ($ million)

NBP 24.5 52.4

PTC 24.7 8.4

MCB 21.1 7.0

PSO 15.6 9.7

BOP 13.5 27.4

PPL 10.9 32.0

OGDC 8.5 46.8

As the data shows, 90 per cent of the increase in total CFS market was concentrated in just six stocks that led the advance in the stock market following initial purchases made by the foreign portfolio investors otherwise there was little in the fundamentals to justify 15-25 per cent changes in stock prices.

Given the facts and trading pattern, it appears that the real reason behind the relatively low trading volumes during the second half of 2007 was not the imposition of the capital value tax (CVT) as has been claimed by some observers and brokers. The market was dull because foreigners were net sellers during four of the six months including November and December. As soon as fresh buying came in January, the local punters jumped on the bandwagon and started making highly leveraged bets at high interest rates and CVT ceased to be an issue. Let us see how long this bull runs on borrowed money?