IT is a hot topic: is rupee devaluation around the corner? But is it the right question? Perhaps not. The real and more important question is whether the government is prepared to review and change the policies that have contributed to a widening trade deficit in the first place? If not, difficult days may lie ahead.

Prime Minister Shaukat Aziz has denied that the devaluation is on the card. The State Bank Governor criticised the media reports for creating “misperceptions and misunderstanding” at a rather unusual Sunday press conference.

The Governor maintained that the central bank abandoned fixed exchange rate regime a long time ago and moved to a floating exchange rate regime since early 2000 and the IMF has not advocated, in its consultations with Pakistan, any depreciation and has just provided its perspective and analysis of the movements in the real effective exchange rate. The World Bank’s Pakistan representative has also commented on economic outlook and exchange rate policy at a media briefing in Islamabad, noting that China and India have allowed their currencies to depreciate while Pakistan has not. This is factually incorrect as shown below:

| % Change Against US Dollar Since | ||

| January 2006 | January 2004 | |

| Pakistan rupee | (1.79) | (5.96) |

| Indian rupee | +0.70 | +1.99 |

| Chinese renminbi | +3.16 | +5.80 |

Pakistan rupee has depreciated against dollar while Indian and Chinese currencies have appreciated.

A few observations are in order:

The IMF is not the ultimate authority on macro economic policy. Its often-controversial and questionable prescriptions have some times proved harmful for the countries that were under its programmes and drew sharp criticism from some of the world’s leading economists.

Pakistan is currently not under any IMF programme and is not bound by its ‘advice’. Moreover, the IMF has provided estimates of the “real” exchange rate using different methodologies. That is, what is the real purchasing power of Pakistani rupee viz-a-viz a basket of currencies given the different rates of inflation in their respective economies? The hard fact is, according to the IMF report, Pakistan’s currency appreciated by 10 per cent in real terms, relative to its trading partners, from December 2004 to June 2006. The correct and relevant question is: does it need an adjustment to bring it in line with its inflation-adjusted value?

Pakistan is not under a ‘free’ floating exchange rate regime. It is under what is called a ‘dirty float’ or a ‘crawling peg’ regime with rupee de-facto pegged to the dollar. What it means that the market forces alone do not determine its value freely and the Central Bank through a variety of controls and interventions plays a key role in determining its value.

The principal reason for the current debate is not the IMF report or some ‘misunderstanding’ but the recent trade performance and the widening current account deficit.

The crux of the matter is the government believes it can run current account deficits year after another as long it can fund them through capital flows or more precisely through borrowings, foreign direct and portfolio investments and privatisation proceeds. In a worst-case scenario, foreign exchange reserves can be used to meet shortfall on a temporary basis.

This approach is faulty, short-sighted and fraught with considerable risks. Industrial and trade strategy should drive financing strategy and not vice versa. It seems that we are treating privatisation as a means of financing the expanding current account deficits while not paying sufficient attention to address the structural and fundamental reasons that are causing the deficits.

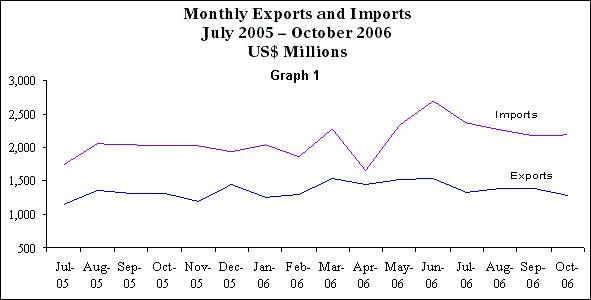

The month-wise imports and exports data for the 16 months to October 2006 reveals a clear trend of declining exports and rising imports. (see graph 1)

During the first four months of the current fiscal year, the exports growth of 1.3 per cent compared to a year earlier is not only behind a much higher 7.7 per cent growth in imports but reveals a worrying trend given Pakistan’s huge dependence on Textile and Clothing exports. They account for 60 per cent of exports but are concentrated in low-value added products: yarn and bedwear/towels account for 45 per cent of textile exports while ready-made garments account for only 15 per cent.

During the four months from July-October 2006, textiles and leather exports declined in absolute terms and the small overall export growth was achieved only due to higher rice exports. The low value-added textiles (yarn, cloth, and bedwear/towels) have seen the sharpest decline in the current fiscal year.

The textile industry is blaming higher energy and interest rate costs while the Commerce Ministry has blamed shortsightedness and immaturity of the business community for their current woes. “The community in their quest for easy short-term gains, compromises on their long-term interests,” said a spokesperson for the ministry, adding had the entrepreneurs and traders read the signals being given by the government and restructured their businesses accordingly, they could have fared better.

While the government and the industry have traded accusations, Pakistan's balance of payments deficit widened 52 per cent in the first four months of the fiscal year 2006-07. The deficit, the amount by which imports exceed exports, remittances and other incomes from abroad, widened to $3.34 billion in the July-October period, from $2.19 billion a year earlier. The cost of importing oil in the first four months climbed to $2.73 billion by $594 million. Pakistan imports about 85 percent of the oil it uses.

What is not disclosed in the figures is the yet unexplained and even larger increase of $862 million in ‘other imports’. Here, it needs to be highlighted that the data provided by the Federal Bureau of Statistics is not detailed enough to facilitate more in-depth and meaningful analysis and even the Ministry of Commerce has cited shortcomings in the statistical data as an issue in taking appropriate and timely policy actions.

In addition, the quality of reporting is not generally at par with those of some other Asian countries. Notwithstanding these issues, all other major imports, including industrial machinery, commercial and consumer vehicles and metals, reported a decline during July-October compared to a year earlier. In summary, given the rise in “other imports’ and decline in machinery and vehicles’ imports, the assertion that the current difficulties are largely the consequence of a higher oil import bill is not supported by the facts nor does it tell the whole story.

It is not just the current year’s data that points to a rapid and unsustainable growth in non-oil imports. During the FY 2005-06, Pakistan’s non-oil imports grew by 32.8 per cent to $21.6 billion from $16.3 billion in 2004-05 and by 76.6 per cent compared to level of non-oil imports ($12.2 billion) in 2003-04.

The government has maintained that the rising imports represent overall economic growth and higher investment spending. If that is case, it should result in correspondingly higher investment spending. However, that is not the case. Why?

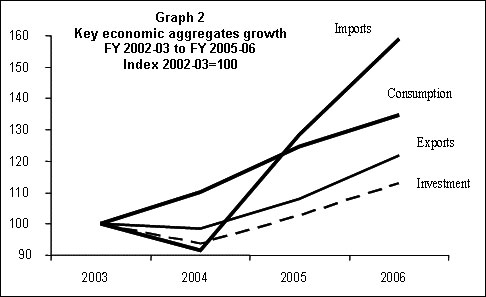

No doubt, the GDP has been increasing at a healthy rate but the growth has been fueled by an extraordinary surge in consumption. During 2005-06, private consumption spending was higher by 34.7 per cent in real terms compared to FY 2002-03 as shown in the graph.

In other words, it increased at an average of 10.4 per cent per annum (in real terms without adjusting for inflation) during the four-year period to June 2006, faster than the overall average GDP growth of 7 per cent. In sharp and somewhat curious contrast, the investment spending grew by an average of only 4.2 per cent per annum during the same period.

Simply put, we have been spending more than we have been producing and that spending boom has been supported by a rapidly expanding banking sector that has been one of the principal beneficiaries of the growing remittances since 2001. (see graph 2)

What has also contributed to the deterioration is the lack of proper incentives to encourage the rising foreign exchange flows to go into the productive channels. Fiscal and trade policy distortions have contributed to a record boom in private consumption (cars, mobile phones, real estate, consumer imports) while the investment spending has not risen as fast although the net banking credit to the private sector grew by 29 per cent in 2003-04, 33 per cent in 2004-05 and 30 per cent in 2005-06. This issue lies at the heart of the current debate.

When a credit or a liquidity driven boom is used to finance an ever-increasing level of consumption and does not result in higher capital formation and investment spending, it causes higher inflation. The problem is exacerbated when higher consumption also involves finished goods imports that put additional pressure on the current account.

The trade policy should eliminate or lower tariffs on imported raw materials and discourage consumption of luxury imports on one hand and discourage exports of raw materials and low value-added goods on the other. We seem to have been doing the opposite: importing more and more of finished goods and exporting more and more of raw materials and low value-added goods. The problem has been further compounded by the fact the Central Bank is not completely independent in reality and has not focused on containing the inflation rate as the most important goal of its monetary policy as do most central banks. The policy makers and the businesses must address these fundamental issues on a top priority basis instead of quibbling about the exchange rate.

The writer is a former head of Emerging Markets Equity Investments, Citigroup.