The stocks ended an eventful 2005 on a bullish note and vowed to pass on the legacy of a sustained bull-run to this year aided by positive indicators and perceptions of new institutional buying and speculative manoeuvring. With technical corrections here and there in an overbought market, the New Year outlook remained bullish. Some heavy cash amounts from different quarters were apparent which if injected in the business could restart the buying euphoria.

The stocks ended an eventful 2005 on a bullish note and vowed to pass on the legacy of a sustained bull-run to this year aided by positive indicators and perceptions of new institutional buying and speculative manoeuvring. With technical corrections here and there in an overbought market, the New Year outlook remained bullish. Some heavy cash amounts from different quarters were apparent which if injected in the business could restart the buying euphoria.

The year which had just passed into history was eventful on more than one count. It ensured a windfall of profits and capital gains for those who did not waver by believing in the strength of the market despite many depressants.

The stocks, therefore, closed the old account on a bullish note as reports of higher corporate dividend and bonus shares and economic recovery did not allow investors, both big and small, to leave the arena as none among them was in a mood to miss the rising market.

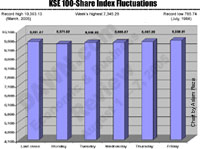

The KSE 100-share index finished the last week of 2005 at 9,556.61 points as compared to 9,491 points a week earlier. The institutional support turned shy in a highly overbought market.

The prices of most leading shares were already on the saturation point under the lead of bank, cement, and energy shares. It was up by 51.02 points over the previous week.

The market’s robust rally was well-reflected in the fact that it absorbed the shock of the massive earthquake and its negative fallout on the economy, the tension of the Kalabagh Dam, and the reported action in Balochistan.

The outlook for the New Year account was terribly optimistic along with other major Asian markets as the investor-optimism was shared by the leading analysts. This could witness the inflow of foreign buying on a large scale.

The outgoing year was eventful in more than one ways. It helped in building up a massive rally after the market collapse in March last which was aided by the positive news both on economic and corporate fronts with investors’ perceptions of handsome capital gains. Some may have suffered financial losses but 2005 made many investors a millionaire.

Click to view the larger image

The sector-wise bank and cement shares outperformed after mid-year on higher earning and larger exports and local consumptions followed by leading energy, fertilizer, chemicals and auto shares.

The stocks during the last trading week of the year showed volatile movements as investors squared their positions on forward counter from the matured December settlements to the newcomer July contracts, leaving negative fallout on the ready section.

But a steep decline in the traded volume to a mere 149 million shares reflected that the general investors held on to their positions ignoring the negative fallout of forward counter.

Incidentally that was a rollover week, said a leading analyst. Financial institutions squared their positions and adjusted their portfolios to open 2006 account on a positive note.

The rolling of positions from one forward contract to another generally upsets the trading pattern on ready counter and it appeared to be more tactical than genuine, others said.

Not in a single session during the last week, the year-end buying made any big showing and its advent was now overdue, they said adding that the next couple of sessions of the fading year could be crucial and may lead to a buying euphoria.

The current index level above 9,000 points indicated the market’s closing on positive note after passing many rough weeks alone on technical grounds, brokers said

The negative fall-out of the Kalabagh Dam from now onward may not remain an irritant for investors as the government had reportedly decided to take the issue to Supreme Court, they said.

Gainers were led by the Gillette Pakistan and Wyeth Pakistan, Shell Pakistan, Sanofi Aventis, Nestle Pakistan, Thal Corporation, Artistic Denim, the EFU Life, National Refinery and many others.

Losers were led by the Attock Petroleum, Fazal textiles, Premier Sugar, National Foods, Noon Sugar, Shezan International, Mustahkam Cement and some others.

FORWARD COUNTER: Speculative issues on the cleared list on-balance ended higher but well below their weekly best levels.

The PTCL, the OGDC, National Bank, the MCB, Lucky Cement, the D.G. Khan Cement and many others finished with extended gains amid active two-way trading.

It was notable that there were no negative fallouts of the rollover position from the matured December contracts to ruling January as most of them were manageable and within the limits of the CFS.—Muhammad Aslam.