A modest recovery at the end of week allowed overvalued shares of oil, bank, cement, and auto sectors to finish with clipped gains. However, the future outlook appeared uncertain despite reports of higher earning from most of the leading companies.

A modest recovery at the end of week allowed overvalued shares of oil, bank, cement, and auto sectors to finish with clipped gains. However, the future outlook appeared uncertain despite reports of higher earning from most of the leading companies.

Investors were reluctant to accept any positive outcome of the PTCL deal and remained sceptical whether or not the deal will go through the set deadline owing to some unresolved issues. Positive signals aired by a Dubai-based paper, quoting the Adviser to the Prime Minister, failed in giving the share a push as it fell further.

Investors will opt for the PTCL share, now ruling at an attractively lower level after completion of the deal by Etisalat, and may not play the host to a loud whispering, brokers said.

The stocks passed through another lean week. However, at the close these appreciated modestly. The underlying sentiments were boosted by the feelers that the PTCL-Etisalat will see the light of the day.

Over a dozen leading companies announced their interim earnings and payouts which in normal conditions was a morale booster for the entire market. Some technical factors neutralized their positive impact on stock trading.

There were attempted rallies early in the week inspired by higher dividend and bonus shares. Some technical factors, notably unloading in the matured October settlements halted the market’s technical rebound.

Analysts said squaring up of positions in matured October settlements which were rung off the board triggered selling in their counterparts in the ready section, and a consequent extension of the previous bearishness.

Click to view the larger image

The selling in part was attributed to lower-than-the-market expectations of profits by the PTCL and its likely negative impact on other blue chip counters, they said.

The rolling of positions from the October to November contracts appeared dried up as was evident from the late recovery of the KSE 100-share index.

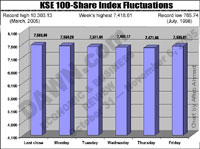

After falling by 300 points early in the week which the analysts called an extension of the overnight sell-off, the index managed to finish with a clipped gain of 28 points at 8,317.36 points as compared to 8,289.81 in the previous week. Active buying in the OGDC and renewed selling in the PTCL were balancing factors in the rise and fall of the index.

Although Eid holidays were a week away but a section of leading investors was trying to shed its extra weight to avert possible losses if the current bearish spell continued, brokers said.

Investors were hesitant to come in a big way until the PTCL deal went through, they said adding, conflicting rumours about completion of formalities by October 28, kept them out of the market.

That was perhaps why some fairly encouraging interim corporate reports failed to stimulate the investors for their stabilizing role in a falling market.

The weakness in oil and bank sectors was another inhibiting factor as investors tried to cash in on the available margins rather than buying at the dips. Cement shares, however, performed well but fresh selling in the textile on reports of lower crop and higher lint prices weighed against their sentiments.

The Nestle Pakistan and the Unilever Pakistan led the list of gainers by Rs20 and 50, followed by the Central Insurance, the United Sugar whose controlling shares were acquired by the management of the JWD Sugar Mills at Rs333.33 per share, the Pakistan Refinery, the Siemens Pakistan, the Wyeth Pakistan and the Colgate Pakistan.

Prominent losers included the PSO, the Attock Petroleum, the Arif Habib Securities, the National Bank, the Bank of Punjab, the MCB, the Island Textiles, the Pakistan Oilfields, Dawood Hercules and the PSO. They ended with clipped gains from their early highs.

FORWARD COUNTER: Speculative issues on the cleared list showed mixed trend but leading among them, notably the Pakistan Petroleum, the PSO, the D.G. Khan Cement, the Fauji Fertiliuser, the Engro Chemicals and some others managed to finish well above the week’s lows. But the PTCL, the OGDC, the Bank of Punjab remained under pressure and fell modestly lower. The MCB and the National Bank managed to finish higher from the week’s lower levels.

It was notable that the matured October settlements were rung off the board and the November contracts assumed the role of ruling deliveries. There, however, was no problem of rolling over of October positions by some dealers to the November contracts.—Muhammad Aslam