THE KSE index, during the last two consecutive weeks broke three psychological barriers on the perceptions of higher activity once reconstruction of the quake devastated areas began, and substantial interim announcements. A good bit of speculative activity did not allow the bulls to loosen their grip on the price line.

THE KSE index, during the last two consecutive weeks broke three psychological barriers on the perceptions of higher activity once reconstruction of the quake devastated areas began, and substantial interim announcements. A good bit of speculative activity did not allow the bulls to loosen their grip on the price line.

The market witnessed a virtual squeeze in bank, oil, auto, cement and pharmaceutical shares followed by fresh price flare-up owing to the pressure on floating stocks.

The current buying euphoria could be extended in the coming week also amid talk of an increase in the exposure limits of banks from 20 to 30 per cent. Banks capable of investing their surplus funds in shares could enlarge their commitments on selected counters in coming weeks, adding to the existing price flare-up, broker predicted.

The post-quake trading week on the stock market was marked by an avalanche of fresh buying orders in bank, oil and cement sectors followed by reports of higher quarterly earnings and predictions of interim payouts.

The price flare-up on blue chip counters was reminiscent of early year bullish outlook but low daily volumes reflected that the investors generally played safe as crash of the last March remained a guiding force for them.

Apart from the reports of expectations of enhanced quarterly earnings and interim dividend, the other contributory factor behind the run-up was the perception of large-scale consumption of most of the items once reconstruction in the quake-hit areas took off.

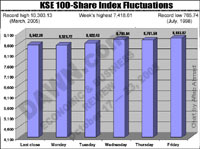

Both, the KSE 100-share index and the market capital steadily rose to their pre-reaction levels and were quoted at 8,863.87, up 321.49 points or 4.5 per cent, and at Rs2,526,832 billion up by Rs81.214 billion from the last close.

The index breached three consecutive barriers as bulls were not inclined to take even a technical breather fearing bears may ride the bandwagon in their absence. It was a spectacular performance despite a massive earthquake resulting in heavy destruction and colossal deaths, and an ensuing misery of those spared.

After mourning the deaths followed by rescue and relief operations, brokers and financial traders were back in the market and made active short covering in sectors still ruling at low levels.

Click to view the larger image

But the mid-week buying flurry in the PTCL followed by some positive developments on the privatization front changed the trading venue and investors flooded its share with heavy buying offers leading to a virtual price flare-up.

As leading bank, cement and oil shares were ruling around high circuit- breakers with some perhaps reaching the saturation points, the PTCL somehow was still an attractive bait at the current level. Any positive news about the completion of sale deals could add significantly to the market trend. That is what actually happened after the reports of completion of formalities by October 28, reached the market and investors started making heavy covering purchases.

The KSE 100-share index broke another three barriers of 8,600; 8,700; and 8,800 amid fresh heavy buying in leading base shares. The smart gains indicate that its next target of 9,000 points may not be that far off.

A major change in the market psychology was thus caused by the PTCL which had joined the band of market trendsetters after having ruled a bit sluggish amid conflicting reports of changeover of the management. Along with the OGDC, it is one of the leading heavy weights.

After absorbing the shock of massive deaths in the quake-struck Northern Pakistan, stocks were back on rails as investors covered their positions in the cement sector followed by predictions of higher sales when the reconstruction work in the devastated areas started.

However, the post-quake grief and sorrow still dominated the corridors of the KSE as silent mourning for victims continue, although some courageous investors and brokers resumed their normal operations.

The economy could hardly remain unscathed after such a huge tragedy but it was too early to say something of its magnitude, analysts said adding it would take time to filter into the real growth and export figures.

The bulk of support originated from the speculative forces who continued to build-up long positions in cement, bank, and oil sectors - not as a genuine investment but for instant gains.

Some other sectors including textiles and those which will be directly associated with the reconstruction work also remained in active demand and generally ended high.

Both, the National and the Muslim Commercial banks hit their career-best levels at Rs166.65 and Rs114.60 on reports of higher earnings linked by the handsome dividend while the revival of demand in the PTCL at lower level was another positive factor.

The National Refinery was leading by gaining Rs14.35 followed by reports that the Attock group of companies had taken over the management of the company after paying the final bid money. The Pakistan Oilfields followed it with a gain of Rs14. The Wyeth Pakistan fell by Rs25 and was leading among the losers.

Gainers were led by the Attock Petroleum, the Attock Refinery, the Pakistan Oilfields, and the National Refinery up by Rs9 to Rs14.35, followed by the Arif Habib Securities, the National Bank, the United Sugar, the Pakistan Refinery, the Suzuki Motors, the MCB, and the National Bank.

Losses on the other hand were fractional barring the Blessed Textiles, the Bolan Casting, the Atlas Honda, the Huffza Steel, the Security Papers, the Glaxo-SKF, the Siemens Pakistan and the Javedan Cement.—Muhammad Aslam