THE stocks last week fell and rose on positive and negative news of the PTCL. However, they managed to finish modestly higher despite a massive battering received by the telecom giant amid rumours that the Dubai-based Etisalat may have backed out from the deal.

THE stocks last week fell and rose on positive and negative news of the PTCL. However, they managed to finish modestly higher despite a massive battering received by the telecom giant amid rumours that the Dubai-based Etisalat may have backed out from the deal.

But its denial, according to a Dubai-based newspaper, pushed it from the mid-week lows on active short-covering at lower levels aided partly by the credible performance of bank, auto and cement sectors.

High dividend and bonus shares by some second-liners also aided the underlying sentiment allowing the market to finish well above the week’s lows amid active daily volumes.

Earlier the stocks turned into a highly volatile performance as investors apparently read too much in the omission of final dividend by the PTCL and extension sought by Etisalat to complete privatization formalities after the payment of final bid money.

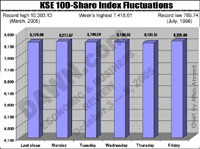

The 100-share index, more than twice crossed the barrier of 8,200 points and confidently sustained it on subsequent buying to finally finish with a modest rise of 45.76 points at 8,225.66 and so did the capital at Rs2,361 billion.

The late recovery was attributed to rumour denial by Etisalat on backing out from the deal. Etisalat had said to honour the deal.

The market should have passed through a major shakeout after the PTCL news but higher dividend and bonus shares by some leading averted panic-selling. Investors were expecting a higher final from corporate giants but were disappointed on omission by the PTCL.

The Privatization Commission had extended the completion up to October 28. Some well-informed brokers feared that all may not be well with the final outcome owing to the questions raised by Etisalat Chief which perhaps had not been cleared by the relevant quarters.

Although, prevailing uncertainty regarding the PTCL sell-off was removed by the government but a section of investors was sceptical over the management transfer in this situation, they said.

However, ready absorption of all sale offers at dips indicated that the sell-off was tactical rather than real - an apparent attempt to outwit small investors and to grab their holding at falling prices, others said.

Click to view the larger image

Analysts were predicting final cash dividend of 35 to 40 per cent in addition to 20 per cent already paid by the PTCL but the passing over of final triggered panic selling in its share which ended lower by Rs6. At one stage it dropped below the resistance level of Rs60.

Owing to weightage in the KSE 100-share index, it could drag down the entire market to new lows, along with the OGDC and the Pakistan Petroleum. But the worst was averted thanks to the presence of strong support at dips.

Leading analysts predicted that the fall was psychological and natural but the PTCL had the will to rise from any low on the strength of its basic financial fundamentals.

Trading resumed on a higher note on active short-covering in the favourites ahead of the PTCL board meeting and conflicting reports about its final earnings.

The PTCL board met on September 27, but omitted the final dividend to the disappointment of investors amid early conflicting reports about its annual earning and the payout.

But its current volatile performance reflected that the strike by the employees at the time of sell-off may had wiped out a substantial amounts in terms of hard cash because of the disruption in services.

The dividend and bonus-share announcements by some resisted a fresh decline as some shares of cement, bank, auto, and energy put on smart gains.

Analysts had said that unlike previous sessions, oil shares could not assume the role of trendsetters along with the banking sector, apparently amid reports that the Prime Minister had sought report on price fixation by the oil giants.

However, bank shares did not look back and maintained their upward drive on fresh covering purchases triggered by reports of higher interim earnings and the market talk of enhanced dividend.

The AKD Securities, Wyeth Pakistan, Millat Tractors, Indus Motors, Pak-Suzuki Motors, Atlas Honda, National Bank, the MCB, Bank of Punjab, Treet Corporation, Cherat Cement, the D.G. Khan Cement, Packages, Shell Pakistan, Pakistan Oilfields, the PSO, Noon Pakistan were leading among the gainers.

Prominent losers included the Grays of Cambridge, Bhanero Textiles, Dawood Hercules, Gatron Industries, Pakistan Refinery, Yousuf Textiles, Arif Habib Securities, Zulfiqar Industries, and the Nestle Milkpak.

FORWARD COUNTER: Speculative issues on the this counter performed well under the lead of National Bank, Bank of Punjab, the D.G. Khan Cement, Pakistan Petroleum, Pakistan Oilfields and some others, finishing with extended gains but on the other hand the PTCL, and some others were modestly marked down on the replacement selling.—Muhammad Aslam