INFLATION is often referred to as “public enemy number one,” whereas high economic growth is, no doubt, a friend to be embraced. Each was present in good measure in Pakistan’s economy last year —growth surpassed all expectations, with real GDP increasing a solid 8.4 per cent in 2004-05, but there was also a hefty rise of 9.3 per cent in consumer prices over the same period.

INFLATION is often referred to as “public enemy number one,” whereas high economic growth is, no doubt, a friend to be embraced. Each was present in good measure in Pakistan’s economy last year —growth surpassed all expectations, with real GDP increasing a solid 8.4 per cent in 2004-05, but there was also a hefty rise of 9.3 per cent in consumer prices over the same period.

With inflation and growth considerably higher-than-expected, most experts are forecasting a decline in both for next year. But with oil prices remaining stubbornly high, projections of the extent to which this will happen are rapidly changing.

For example, the Asian Development Bank (ADB) in its latest Outlook Update now says that growth in 2005-06 will decline a ½ percentage point more than previously expected, to 6½ per cent. Moreover, inflation is now projected by the ADB to decline only marginally, to 8½ percent compared to a decline to five per cent previously anticipated.

The present situation highlights some age-old questions: Isn’t it natural for higher growth to be accompanied by higher inflation? When can we live with an increase in inflation—or have no choice but to live with it—and when should we fight it? And, what are the costs of fighting it in terms of lost output, etc? Here we review the theoretical arguments and the cross-country evidence, and then evaluate Pakistan’s recent experience.

Economic theory and cross-country evidence: The relationship between growth and inflation depends on the state of the economy. An economy can experience high growth without an increase in inflation if its productive capacity (or potential output) is also expanding rapidly, so that supply is more than keeping pace with demand.

It can also experience rapid growth without inflationary pressures if output is below potential and the economy has a lot of catching up to do. In such a situation, because there are unemployed resources (slackness), a rapid expansion of demand employs unutilized factors of production, thereby generating income and spending and further employment, and so on, which leads to higher growth.

Once capacity constraints are reached and actual output has caught up to potential output, however, inflation starts to pick up because of excess demand. It may still be possible for very rapid growth to continue for a while through overtime shifts, etc, but now it would be accompanied by higher inflation.

Such an economy, in which the output gap—defined as actual output minus potential output—has become positive, is said to be overheating, and it needs to be cooled down through such measures as a tightening of monetary policy. This is because, in the long run, an increase in demand at a rate greater than the rate of increase in productive capacity would only lead to higher inflation, without any additional economic growth—or worse, a negative effect on growth.

We can also get an increase in inflation through shocks to the supply of certain food items and to world oil markets. Such supply-side shocks are very volatile and can cause large fluctuations in food and oil prices, the effects of which on overall inflation cannot easily be countered through demand management, including monetary policy.

The cross-country empirical evidence provides only weak evidence of a positive relationship between inflation and growth, and that too only for relatively low inflation rates. There appears to be consensus that once a threshold level of inflation is crossed—a threshold which appears to vary from country to country—the relationship turns strongly negative, and further increases in inflation have very deleterious effects on economic growth.

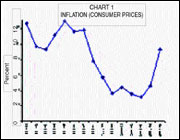

Pakistan’s experience: The average consumer price inflation rate in Pakistan over the past 32 years was a little above nine per cent. More recently, as shown in Chart 1, the downward trend of inflation, in which inflation fell from about 12 percent in 1996-97 to three per cent in 2002-03 has reversed, and inflation has risen sharply over the past two years, to more than nine per cent in 2004-05. Casual empiricism suggests that the threshold rate of increase of prices, beyond which a rise in inflation clearly has a negative effect on growth, is about 11 per cent for Pakistan. Using 12-month changes in prices and monthly data, Pakistan’s inflation rate touched this threshold earlier this year.

Pakistan has not experienced bouts of extremely high inflation or hyperinflation that have plagued Latin America, for example, from time to time. However, annual inflation was above 11 per cent in 11 of the past 32 years (about a third of the observations in the sample). As shown in Chart 2, average real per capita growth was 1.3 percentage points less in those years in which inflation was above 11 per cent, consistent with the conclusions of the cross-country evidence.

In light of the previous discussion, is the recent sharp rise in inflation in Pakistan a case of an economy that is overheating? Or, is it the case that the high inflation can be accounted for by special supply-side factors, with the rapid growth being independently explained by gains in productive capacity? A bit of both appears to be the case.

Three factors should be noted in defence of the government’s policies generally and of the State Bank of Pakistan (SBP), in particular. First, there is much to the argument that a big chunk of the recent rise in prices can be accounted for by supply-side changes, which have kept food prices and world oil prices high. Computations using monthly price data show that about two-thirds of the rise in consumer prices over the past two years can be accounted for by increases in the ‘Food, Beverages, and Tobacco’ and ‘Transport and Communications’ (which includes the price of petrol and diesel) components.

Second, according to estimates made by the Social Policy and Development Centre (SPDC) in its latest report on the State of the Economy, the output gap (which, recall is the economy’s actual output minus its potential output) turned negative in 1999-2000 and remained negative through 2003-04, so that until last year it was not a source of inflationary pressures.

Third, no doubt, the government’s policies and the stable macroeconomic environment have contributed to increasing the long-run sustainable rate of economic growth so that a higher level of demand can now be supported by the economy.

Having said that, there is no room for complacency on the part of policymakers, as there are signs of stress and, in particular, overheating now emerging in the economy. One such sign is that other components of the consumer price index (CPI) besides food and transport and communications, particularly house rent, are also registering substantial increases.

Moreover, according to SPDC estimates, the output gap may well have turned positive in 2004-05, suggesting that there are demand-side pressures on prices building up as well. And, although no doubt the long-run sustainable growth rate of the economy has increased, it is unlikely that potential output growth has yet reached the 7-8 percent mark because part of the recent surge in output is due to transient factors, such as a bumper cotton crop. Therefore, with the output gap already positive, if aggregate demand is allowed to grow at around this rate, this will further exacerbate excess demand pressures in an environment in which inflation is already high.

The expectations effect is important too. There is thus a real danger that the current high rate of inflation, whatever its source, can get locked into expectations of inflation, which then become self-fulfilling through mechanisms such as wage contract renegotiations based on these expectations. The booming imports are also suggestive of an overheating economy, and, if the rupee continues to depreciate, this will also have pass-through effects on inflation.

Finally, the proposed federal budget for 2005-06 is expansionary and makes the task of controlling inflation all the more difficult.

The factors, as mentioned earlier, will not automatically dissipate with a deceleration of food and oil prices. It is, therefore, appropriate that the SBP has now adopted a contractionary stance of monetary policy, and further tightening is probably in order.

Also, although some expansion of credit to the private sector was necessary to stimulate the economy, credit should now be reined in to prevent household debt from reaching unsustainable proportions. Evidence presented in a recent issue of the IMF’s World Economic Outlook suggests that excessive credit growth in developing countries can have very adverse effects on real variables.

However, it can be a bit tricky to determine what level of credit is “excessive” in a fast-growing economy and one in which financial deepening is also taking place. Such credit as occurs should also be channelled more concertedly toward physical investment to prevent it from leading to too much speculative activity in the real estate and stock markets.

Finally, not only can high inflation erode the gains from growth, but it also increases the huge divide between the rich and the poor. And, in this respect, it is little comfort that much of the inflation is due to food price increases; since the poor spend something on the order of half their income on food items, food prices inflation hurts them particularly.

In sum, Pakistan’s economy has made impressive gains on the growth front and, bolstered by the government’s macroeconomic policies, the long-run sustainable rate of economic growth has, no doubt, increased.

But some of the recent surge in activity can be attributed to factors such as a bumper cotton crop, which has a large transient component, and unused capacity which may now have filled up. Thus, although supply-side factors account for much of the recent increase in inflation, signs of overheating are now discernible in the economy, and demand needs to cool off in the short run.

The euphoria over growth should not lead to complacency and Pakistan’s policymakers should be cognizant that over-estimating the potential growth rate of the economy runs the risk of letting demand elevate to a level that cannot be sustained. If such an outcome materializes, it would put further inflationary pressures in an already high inflation environment. And all the international evidence suggests that if high enough inflation persists for a while, it can make the gains from growth and macroeconomic stability disappear in a hurry.

Dr Shaghil Ahmed is Acting Managing Director and Mr Abdul Aleem Khan is Research Officer at the Social Policy and Development Centre, Karachi