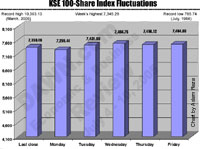

THE KSE 100-share index managed to finish with a good gain of three per cent or 114 points but well below the previous week’s highest of 7,538.00 as investors played on both sides of the fence awaiting some positive news on the COT front.

THE KSE 100-share index managed to finish with a good gain of three per cent or 114 points but well below the previous week’s highest of 7,538.00 as investors played on both sides of the fence awaiting some positive news on the COT front.

But until the fag-end of the week, reports about the COT and margin financing were not confirmed by either by the KSE high-ups or the SECP bosses. There was, however, a loud whispering in the market that both the COT and margin financing will go together for the next couple of months to restore respectability to stock trading.

However, the market showed a measure of strength on rumour-driven strong covering purchases at the lower levels but buying interest by and large remained terribly selected as investors were not inclined to go beyond the safe havens.

The KSE 100-share index confidentally breached through the psychological barrier of 7,500 but failed to sustain it on late selling and was last quoted around 7,464.60 as compared to 7,350.400 a week earlier as some of the leading base shares managed to finish higher. Market capital also rose by Rs37.847 billion at Rs2,071.180 billion and the index 114.14 points.

With the end of old account on June 30,2005,the new account was opened on a bullish note as leading brokerage houses and financial institutions resumed new year buying in the backdrop of higher corporate earnings and tax relief in the budget and massive incentives for the textile sector.

The current status quo will end with the new account as there are reasons to believe that lull created by the failure of the internet system owing to washing away of optic fibre will end by the next week and normal trading will resume, brokers said.

Reports that the Etisalat has paid 10 per cent($260m as first treanche) against the total sale proceed of the PTCL sell-off of $2.59 billion as stipulated in the deal quashed rumours that it has backed out of its commitment as the did the bidder of the KESC. Its share value rose from the weekly low to close around Rs66.90.

What seems to have reinforced investor perceptions of a robust future market was the revival of demand even on some untraditional sectors followed by rumours that the cut-off date of phasing out of badla financing has been extended beyond Aug 26, 2005.

On the heels of this, the mid-week trading witnessed another rumour that badla and margin financing go together until the end of the current year, allowing badla financers to re-enter the market.

Click to view the larger image

“The share business, which was facing liquidity problems as both banks and badla financers stayed on the sidelines awaiting fresh positive developments after the rumour-driven speculative buying lost its shine.

The market remained in the tight grip of rumour-mongers but there was no official word on the badla or margin financing whether or not the cut-off date is being extended or both will go side by side until the banks lined up Rs30.00 billion for margin financing.

A section of leading investors, however, continued to unload badla-related positions in the rung-off June settlements in the wake of its progressive phasing out into margin financing and in the absence of covering purchases at the dips, prices fell further across the board.

But analysts said the consortium of banks, which has committed to set a side Rs30.00 billion for the brokerage houses for margin financing is said to be not that liberal in extending required credit lines and the switch over has created liquidity problems for the investors.

What worry brokers is post-privatization persistent selling in the PTCL, which otherwise should have led the entire as it has been doing early this year on market talk of its sell-off.

It has fallen by Rs5 during the post-sell-off sessions, which reflects tactical selling by an interested group to push its price below Rs60 and then to resume covering operations.

What is more disturbing for all other heavy weights, including OGDC, Pakistan Oilfields, National Bank and PSO are following its trend, sending bearish signals to the general investors.

“ Absence of the year-end portfolio adjustments may be another reason behind the current sluggishness but the chief factor is the liquidity problem”, they said, adding that the “falling volumes signal investors are just marking time giving time to banks for adequate funding under margin financing”.

They said in market parlance it could be year-end pause but some others claim the market is the victim of technical factors including squaring of carryover transactions(COT) positions in the June contracts.

Investors are expected to be back in the market during the first week of the new fiscal(July 1) as by that time outstanding positions in the rung off June settlements will be squared up, they added.

Although losers again dominated the list some leading shares managed to finish partially recovered under the lead of EFU Life Insurance, Pakistan Services, Unilever Pakistan, Artistic Denim, and Arif Habib Securities, which posted gains followed by Zulfiqar Industries, Clover Pakistan, Pakistan Petroleum and Haroon Oils, up Rs3-4.05.

Losers were led by some of the leading foreing MNCs, notabluy Park-Davis, Wyeth Pakistan, Rafhan Maize followed by Clariant Pakistan, Nestle MilkPak and Glaxo-SKF. Other prominent losers included, Mari Gas, National Refinery, PSO, Berger Paints and AKD Securities.

FORWARD COUNTER: Speculative issues on the forward counter maintained their early week gains and finished higher under the lead of PTCL,OGDC, National Bank, PSO and some others, largest rise of Rs8 being in Pakistan Petroleum.—Muhammad Aslam