KARACHI, June 23: Stocks on Thursday turned mixed as some of the leading base shares came in for active late short-covering at the lower levels and finished partially recovered but the undertone was a bit shaky.

KARACHI, June 23: Stocks on Thursday turned mixed as some of the leading base shares came in for active late short-covering at the lower levels and finished partially recovered but the undertone was a bit shaky.

The market’s inability to achieve a major breakthrough in the post-PTCL privatization sessions is chiefly attributed to the meagre financial support despite lining up of well over Rs10 billion for margin financing by some of the banks.

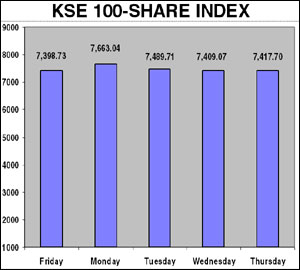

Both price and index showed terribly volatile movements and it was well-reflected in the KSE 100-share index, which after having fallen to day’s lowest at 7,185.00, off 224 points, recovered to close 8.63 points higher at 7,417.70 as compared to 7,409.07 a day earlier.

Whether or not the remarkable late rally could be sustained at the weekend session will set the market’s future direction, brokers predict.

The late recovery was attributed to active short-covering in PTCL (which at one stage has fallen to Rs64.25), OGDC, National Bank and some others.

The initial steep decline was attributed to clearing worries on the forward counter and fall in financial demand, and later recovery to short-covering in some of the high profile shares, just to show that all is well on the bourse.

“The post-privatization performance of the PTCL is not in line with the analysts thinking but they predict a turned around any time by the next week as higher bid price could prove an attractive bait for investors in the sessions to come”.

Investors appear to be taking an extra care about the matured June settlements on the forward counter and are not inclined to ride the bandwagon until the clearing is smooth.

Memories of previous standoff in the clearing in May contracts, which caused massive selling in the ready section, are still afresh in the minds of investors who mostly played safe as was reflected by falling daily volumes.

Memories of previous standoff in the clearing in May contracts, which caused massive selling in the ready section, are still afresh in the minds of investors who mostly played safe as was reflected by falling daily volumes.

Unlike the previous default on the part of some of the leading brokerage houses, there is no possibility of any problem as volumes in the cleared list are according to the limits set by the KSE high-ups, analysts said.

The matured forward June contracts will be rung off the board from next Monday, which could put the market back on the rails the same day as investors fears would be allayed, they said.

Losers again dominated the list under the lead of Atlas Honda and Unilever Pakistan, off Rs8 and Rs15, followed by National Refinery and Pakistan Refinery, Pakistan Cables, Dawood Hercules, Century Papers, and Atlas Honda, off Rs4 to Rs5.

Mari Gas, which came out with the second interim dividend of 10 per cent on the other hand fell by Rs7.20 as it seems to have fallen below the market expectations.

HinoPak Motors and Shell Pakistan managed to finish with good gains of Rs5.20 and Rs15.95, respectively, and so did Muslim Insurance, Arif Habib Securities, Ahmed Hassan Textiles, OGDC, HinoPak Motors, Nishat Chunian and Artistic Denim, up by Rs2 to Rs5.20.

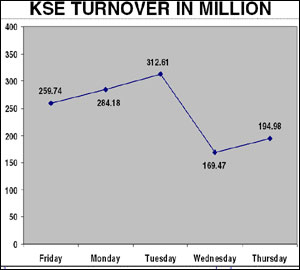

Trading volume showed a modest rise at 195m shares from the previous 170m shares but losers maintained a strong lead over the gainers at 195 to 69, with 38 shares holding on to the last levels.

PTCL again topped the list of most actives, unchanged at Rs66.95 on 63m shares followed by OGDC, higher by Rs2.60 at Rs106.20 on 41m shares, National Bank, firm by 20 paisa at Rs103.20 on 17m shares, PSO, off Rs2.85 at Rs381.90 also on 17m shares, Pakistan Petroleum, up by Rs1.50 at Rs216.00 on 12m shares, Pakistan Oilfields, lower 25 paisa at Rs270 on 5m shares and Attock Petroleum, off Rs2.70 at Rs156.50 on 4m shares.

Other actives were led by D.G.Khan Cement, lower 45 paisa on 7m shares, Fauji Fertilizer Bin Qasim, easy 40 paisa on 2m shares and Lucky Cement, up by 95 paisa also on 2m shares.

PTCL also led the list of actives on the forward counter, easy 46 paisa at Rs67.79 on 16m shares for the July settlement followed by its June contract, off 95 paisa at Rs66.15 on 15m shares.

Pakistan Petroleum rose by Rs1.65 at Rs216.50 and Rs1.95 at Rs222.10 both for the June and the July settlements respectively. OGDC rose by Rs2.45 at Rs106 on 9m shares.

DEFAULTER COS: Trading on this counter remained insipid in sympathy with the prevailing sluggishness in the ready section. Stray business was reported on a number of counters but price changes were mixed and mostly fractional.