Pakistan’s quarter-century Ponzi scheme, and the exit that has no architecture

Long before credit rating agencies existed, there was a simpler test of financial health: can a borrower pay interest from their income, or by borrowing more money?

American economist Hyman Minsky gave the failed rating a name: Ponzi finance. And it is worth being precise about it. A Ponzi position is not high debt, or even rising debt. It is the specific condition in which you are paying your interest by borrowing more money.

Pakistan has run Ponzi finance for a quarter of a century. From the late 2000s until two years ago, our budgets were in constant loss because we were spending more than we were earning each year, before deducting what we had to pay in interest on loans. Each rupee in interest payments on the national debt was paid with a freshly borrowed rupee, and then some more.

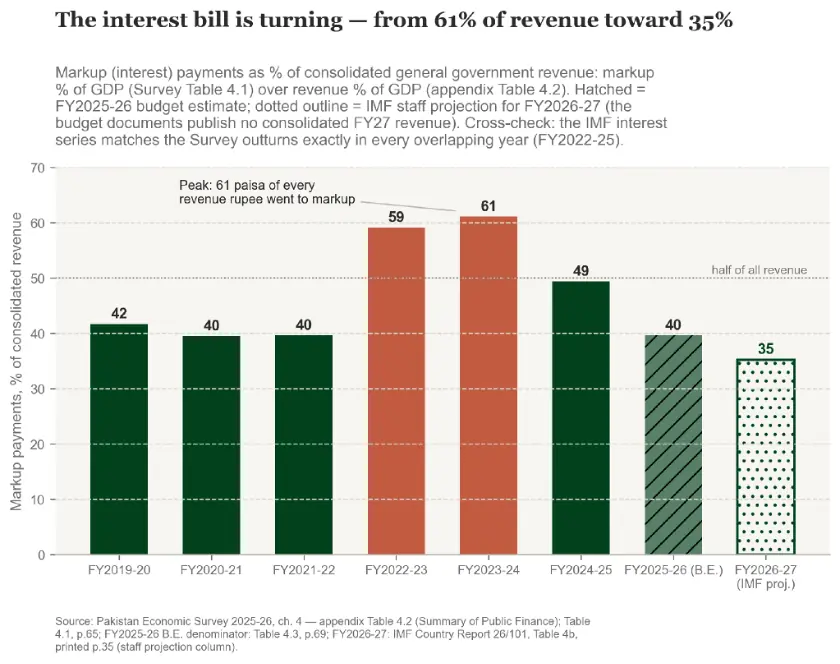

Pakistan’s debt-to-GDP ratio rose every single year from 2012 to 2023, going from 58 per cent of GDP to over 82pc (except for 2021 when we received Covid-19 relief). Our burden of interest peaked in the year to June 2024, when it ate into sixty-one paisas of every rupee the government earned.

This essay makes three claims. First, that the Ponzi scheme never collapsed, for reasons that are uncomfortable rather than reassuring. Second, the past two budgets made the first genuine attempt to exit since the turn of the century. Third, the heart of the matter, that the gains are financial but not institutional: we have interrupted the machine that produced the Ponzi without replacing it, and the new budget shows the old incentives still running underneath.

Why Pakistan’s Ponzi scheme never collapsed

A private Ponzi scheme dies when new money stops arriving. A sovereign one does not die, because the state has three instruments no private schemer possesses, and over the past decade, we used all three.

The first is a captive lender base. Most of our domestic debt is held by our own banks, which fund those holdings substantially through liquidity from the State Bank of Pakistan (SBP, our central bank). The system can be leaned on to roll the debt over, and it was. More on this shortly.

The second is the inflation tax. The great inflation of 2022–24, and the lesser spike of 2019, were not just a household tragedy; in cold fiscal terms it was the Ponzi scheme’s settlement mechanism at work. Inflation quietly wrote down the real value of the government’s rupee debts by eroding the value of money in current accounts and our wallets. Much of the fall in our debt-to-GDP ratio since came through the denominator: the price level, not repayment.

The third instrument is the strangest, and this June’s documents display it openly. The government pays interest on its domestic debt; the financial system earns it; the State Bank’s own profits — earned largely from lending to the banks that hold government paper — are transferred back to the government as “non-tax revenue.”

One arm pays, another receives, and the books record both a cost and an income. This year that one source was worth Rs2.4 trillion — and nearly half of last year’s much-celebrated revenue surge was, on inspection, this loop.

Let’s piece this together in simple terms: the government gets through another year without expanding the tax net, fixing government-owned company mismanagement, or trimming waste. So we come to the end of the year with less money than needed. The government goes and borrows more money from the banks, and promises them a return above inflation. The problems stay unfixed, and the government ends the next year with the usual gap, and in addition has to pay interest on this year’s new debt. So it goes out and borrows more money…

Non-filers aren’t touched. State-owned enterprise employees and vendors aren’t touched. Bureaucrats still all have their jobs. Politicians are still in power. And banks end the year having earned interest above inflation. If you own assets that don’t age, such as plots or gold or dollars, you’re still doing fine.

But if you are salaried, or run a kiryana store on cash, or don’t put your money in bonds or a savings account out of a sense of piety, or are one of the 100 million Pakistani adults without a bank account, you have — for one generation now — paid disproportionately for the system’s Ponzi scheme.

The exit is real

The good news is that the recent improvement is not a rounding artefact. Interest took 61 paisas of every rupee of revenue at the peak, in the year to June 2024. It fell to 49 the next year, and the budgets since point lower still toward the mid-30s.

And the turn rests on real legs, not accounting. Interest rates have fallen from their crisis peak. As a result, this year’s budget projects the State Bank’s own transfer to drop by 41pc, because it will rightly earn less interest than in the past. The federation has run a primary surplus for the first sustained stretch since FY2000: the Minsky test, passed, two years running. And last year, almost without precedent, it spent less than it had budgeted on both current and development heads—the first such mid-year underspend in at least sixteen budget cycles.

So the financial exit is genuine. The question that matters is what is holding it up.

Financial, not institutional

The honest answer: an external programme, not a domestic architecture. To see why that matters, return to where the Ponzi’s engine was built.

Institutions discipline spending when each tier of government is a residual claimant — when it keeps the marginal rupee it saves or taxes and bears the burden of the marginal rupee it overspends. The Eighteenth Amendment and the Seventh National Finance Commission (NFC) Award, our great decentralisation of 2010, were meant to bring decisions closer to the people.

What they did was split decision rights from residual risk. The provinces received the big spending responsibilities—schools, hospitals, local infrastructure — together with a constitutionally guaranteed 57.5pc of the divisible tax pool, arriving by formula regardless of their own tax effort; the constitution now forbids any future award from giving them less.

The federation kept the opposite bundle: the deficit, the debt, and the duty to fund itself from the minority share of every tax rupee its machinery collects. And the great promise of efficiency gains through decentralised governance never arrived, because provincial governments never devolved power and simply replaced top-down and bureaucratic management from Islamabad with top-down bureaucratic management from Karachi, Quetta, Lahore, and Peshawar instead.

Nobody, in other words, became a residual claimant. Provincial capitals are claimants without residual risk: their transfer is unconditional, so the return to building their own tax capacity is politically negligible, and their own-source effort has stayed trivial. The federation bears the residual risk without incentive: every additional rupee the Federal Board of Revenue collects yields it forty-two and a half paisa. The deficit became a commons — and the quarter-century Ponzi was the commons being grazed.

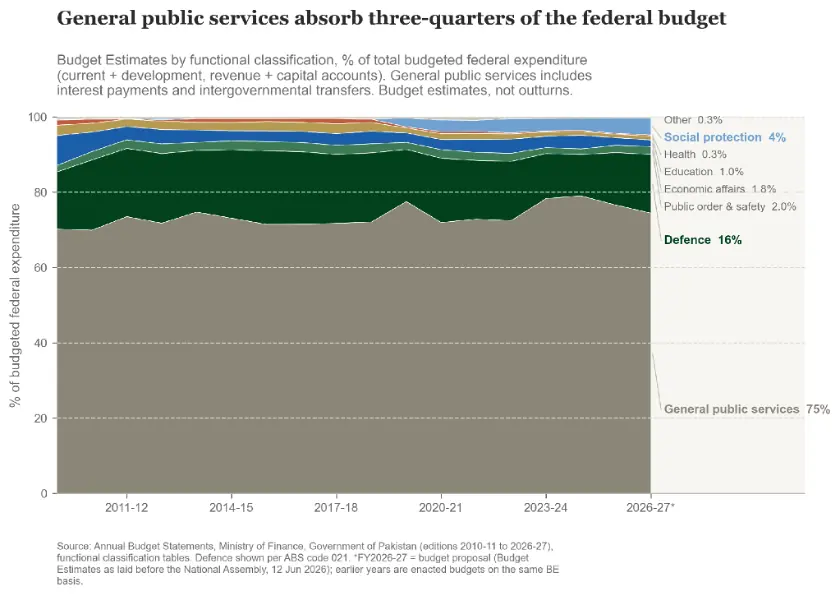

The federation was handed the worse bundle, but it did not play even that bundle straight. Devolution was supposed to shrink the centre; the centre never shrank. The World Bank’s expenditure review found that federal spending on subjects the constitution had handed to the provinces actually rose after the amendment, with six-figure growth in federal staffing to match.

Fifteen years on, the federal budget’s functional shape is almost exactly what it was before devolution — three-quarters general public services, a rounding error on the health and education it no longer runs — the ministries devolution made redundant still open, still funded. BISP, expanded over time with great fanfare and acclaim, was financed simply by displaying other types of Federal social spending.

So how does the federation respond to this broken architecture? It sidesteps the fundamental problem and starts undercutting it: instead of building political consensus to create permanent institutional fixes with the 18th Amendment’s flawed but principled structure, it migrates some taxation to instruments that sit outside the divisible pool and are kept 100pc federally—the petroleum levy first among them.

This year’s budget asks the levy for 12pc more revenue while its own volume assumptions grow 4pc: arithmetic that closes only at six to nine rupees more per litre. The legal machinery is already in place. The statutory ceiling on the levy was deleted last year; the remaining rate schedules go in this year’s Finance Bill; a new climate levy stands beside it — each adjustable by gazette notification, with no return to parliament.

The levy creep is usually read as a revenue tactic. It is better read as the broken architecture speaking: a federation that must share taxes but may keep levies will, year after year, tax the country at the petrol pump.

Now look at what restrains the system today. The provinces are banking the largest surpluses in their recorded history — not because any incentive changed, but because the International Monetary Fund programme sets the floors and the National Economic Council has frozen provincial development to hit them. An external referee is doing the work that our own economic and legal institutions will not: the restraint is rented, not owned. The replacement institution — a National Fiscal Pact that would re-align spending functions with revenue claims — exists, so far, as a single line in the IMF programme’s commitments table. The NFC award itself has not been reopened since 2009.

We have not rebuilt the machine, merely unplugged it.

That is the precise sense in which the gains are financial, not institutional. The primary surpluses, the falling interest burden — all real, all reversible, because each is enforced by a programme with an expiry date rather than by an architecture in which any Pakistani government, federal or provincial, profits from prudence.

And inside the discipline, the old reflexes show: a new, unexplained lump of Rs 361 billion labelled “National Economic Initiatives” — larger than the federal health and education budgets combined, absent by name and amount from the demands the National Assembly votes — sits in the summary tables, roughly half the size of this year’s entire real-terms interest saving. The saved money is already leaking toward discretion.

The bargain we have not struck

Development does not start until a country’s powerful conclude that their own futures are better served by growth than by extraction, and bind themselves accordingly.

Everything in this budget that works — the surpluses, the falling interest share, the honesty of a shrinking State Bank dividend — can be reversed as quickly as our rulers’ moods. Everything that does not — the levy migration, the unexplained lump, the untaxed sectors still untaxed, the banks still fattest when the state borrows most, the federation and provinces still locked in a formula neither will reopen — is the evidence that our elite bargain remains unstruck.

A quarter-century of Ponzi finance was not a technical failure; it was how the absence of that bargain was financed. The exit from the scheme will not come until prudence and national economic growth interests our rulers more than its convenient alternatives do — when some tier of our own state becomes the residual claimant of its own choices. Until then we are solvent on a lease. Next June’s revised estimates will tell us whether we have begun to own the place, or merely behaved while the landlord came around for another inspection.

The writer is an associate professor of economics at LUMS and a board member of the National School of Public Policy. He tweets at @AliHasanain