Is Karachi disposable by design?

Gul Plaza’s three facades were clearly damaged in the stage II and III January 18 fire which killed 70 people, but when a building inspector came afterwards, he held back. “It was impossible to go inside,” he said, “the heat was too intense even after two days.” That same month, one after another, three other market fires erupted in Karachi, intensifying the feeling of anger and helplessness that the city had turned into a tinderbox because of years of neglect. The bodies just keep piling up.

The preventable deaths from urban negligence — fires, open manholes, building collapses, electrocution, rains, bad road design — all speak to the systemic weakening of Karachi. At least 300 have been reported in newspapers so far in 2026 by rough count. Many of these deaths are evidence of the failure of vertical expansion of informality. You cannot allow floor upon floor, shop upon shop, to be slowly added to urban spaces and infrastructure that was never designed to support such density in the first place.

Neither the Karachi Metropolitan Corporation (KMC), its fire brigade nor the regulatory Sindh Building Control Authority (SBCA) seemed to respond to this state of affairs in any way that would persuade us that they were aware or care about just how unliveable they were making the city.

Instead of focusing on the accountability of these governing institutions and their actors, so much of the talk surrounding these preventable deaths skips to championing what is described as informalisation as resilience or a rose-tinted tale of survival against odds. But for the oppressed with no choice but to live and work in Karachi, resilience’s ugly reality consists of working in a building with no safety standards. There is no ventilation when smoke chokes it, and the flames swallow the stairwells or when its exits are blocked or structurally insufficient to cater to the actual volume of people inside. That is not the resilience of a people. It is the abandonment of the system supposed to serve them.

Fire station coverage

The international benchmark, guided by the National Fire Protection Association, says that the first responding unit should take no more than 4 minutes to reach a fire. Full deployment should take no more than 8 minutes. In cities with thin traffic, this translates into a 2-3km service radius for a fire station.

In places where fires spread rapidly, such as high-risk commercial hubs and industrial zones, the standard is for a station to be located within a distance of 1.5kms. But in Karachi, however, congestion shrinks this safety zone to a mere 0.5km. In other words, a fire station should be 500m away. By these standards, the city needs over 200 fire stations. It has only 26.

In high-density zones, where water infrastructure is already unreliable, spatial shortage ensures that by the time help arrives, the window for containment has already slammed shut. The following data shows the huge gap between population density and the available emergency infrastructure.

Given the shortage of fire stations, the state needs to reconsider how the existing ones should serve their areas. It should not allow taller buildings (through floor-area-ratio relaxations) until it is confident it can tackle their fires. This applies to vertical intensification, for cases when a builder wants to turn an old two-story bungalow in PECHS into six floors of apartments. This adds to the load of the service areas of existing fire stations.

Since the 1980s, land values and floor area permissions have drastically changed in the city. This has raised concerns about the idea of “disposable architecture” — buildings designed for short-term profit at the expense of long-term human survival.

The money trail

Poor safety in Karachi is often blamed on oversight, but in the fire department’s case, it is also a symptom of cost-cutting, or worse, the creative diversion of funds. As recently as the 2024-25 financial year, audits from its ledgers provide ample damnation.

In one instance, the Auditor General of Pakistan found that Rs33 million was paid out for vehicle repairs, but the work was not authenticated with original vouchers, daily work orders or logbooks.

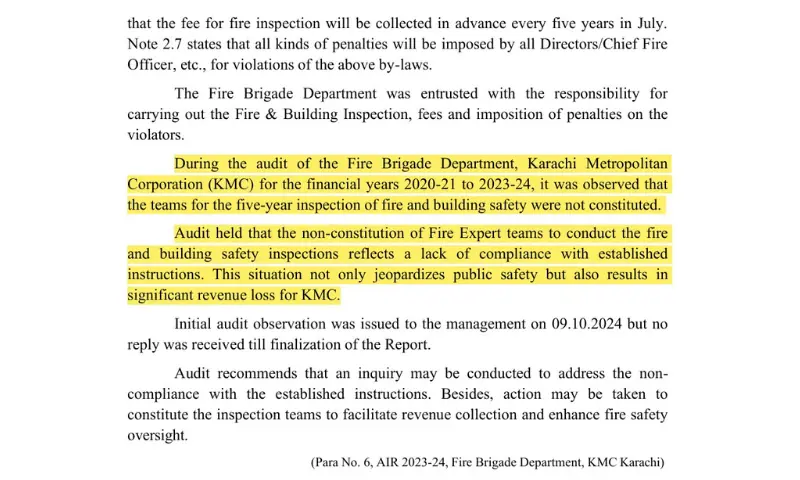

In earlier years (from 2020-21 and 2023-24), KMC didn’t ensure mandatory five-year fire and building safety inspections. Other discrepancies speak to sheer neglect, such as KMC forgetting for three years to register 55 fire vehicles sent as a gift from the federal government, in violation of its own Sindh Motor Vehicles Ordinance, 1965.

The Auditor General’s office was cognisant of the significant operational challenges KMC’s fire brigade wing faces in the shape of sprawling urbanisation, ageing infrastructure, and high vulnerability to disasters. These factors notwithstanding, the AGP’s findings suggest that the state is effectively feeding the city’s decay by ignoring how critical safety budgets are mismanaged.

Half the frustration is that people wondered why nothing had changed since the terrible lessons learned from the 2012 Baldia factory fire, in which more than 250 people were killed. After Gul Plaza, people working and living in high-rise buildings across the city started wondering where their fire escapes were located. An employee of a commercial bank on I. I. Chundrigar Road said they were worried that their office had not held any fire drills after Gul Plaza.

It is not much better in the neighbourhoods, with the 38-year-old resident of an apartment building in North Nazimabad saying all they received was an SBCA warning to comply with fire regulations in three days. “Our building has only one staircase, and two lifts, one of which has not been working for more than two years,” he said. “When the 11-storey apartment was built on a 2,000 square yard plot without a proper fire exit, where was the SBCA?” Builders build for profit, so they compromise on safety, he added. A building can be structurally sound, but it can still be a death trap.

If the people of Karachi were wondering what had been going on, the Sindh High Court outright asked how the SBCA had been doing business for the last forty years. Turns out it had not written the actual Rule book for buildings (as Section 21 of the Sindh Building Control Ordinance, 1979 insists). Instead, the SBCA has relied on the lesser powerful instrument of Regulations. To the court, this effectively meant that many buildings were given the green light “without lawful sanction”. The city’s Master Plan gathered dust on the tenth floor of Civic Centre while its skyline shot up with deathtraps.

“No regulator in the world allows 20 per cent violations in bylaws, but the SBCA does,” said an architect who did not want to be named, as it carries the risk of jeopardising drawings that need approvals. In fact, the builders are just as much to blame. They work with the architect and pay just 60 per cent of the fee until they receive the SBCA approvals. “Once they have the approvals, they forget about the architect and the submission drawings,” he added. “If an architect is principled, they would withdraw their approval. This forces the builder to [look for] some other architect willing to stamp without even a look at the submissions.”

This is why it is said that a stamp mafia is the dark underbelly of Karachi’s building and construction sector. It is alleged by many associated with the built environment, including some researchers and civil society activists, that very few buildings, commercial or residential, are built according to their submission plans. Many are not fire safe. These independent voices hold the city’s regulators responsible, along with Sindh’s legislators, as builders pay off this entire layer of elite to keep this system intact.

It is not difficult to speculate that this was the case with Gul Plaza. And indeed, some digging proves it.

At Partition, the land where the shopping plaza was built was originally an amenity plot for a KMC tram depot. But then the city government converted Plot No. 32-PR-1, Preedy Quarters, Saddar Town into a commercial site, thereby dispossessing the public of its right to a safe environment just so it could grease the wheels of capital accumulation for builders and traders alike. By the 1980s, Gul Plaza rose up with a plan for 1,021 shops on the ground, first and second floors with parking in the basement. In 1998, another floor, parking on the roof and 179 shops in the basement were crammed in.

Over time, the shop owners built wooden storage lofts so they didn’t have to keep ferrying stock from warehouses outside. The corridors and exits narrowed as displays bulged into them. Gul Plaza was, after all, the city’s most popular home store. This gradual erosion of safety features was codified under the guise of “meeting commercial demand,” according to the court documents. And by 2003, the SBCA was only too happy to certify that the building complied with all its rules and bylaws.

It did this even though the lofts alone degraded the building squarely to the most dangerous Type V (combustible) category. Type V structures that exceed basic height and area limits are often not permitted for high-density commercial use. The SBCA’s Technical Committee on Dangerous Buildings notes: “The entire building was occupied by various categories and types of shops and godowns in different sizes with display and storage of all household saleable goods and items, right from imported and local top quality products in plastic, wood, glass, leather, metal, marble, stone, rubber, fibre glass, PVC, foam, paper, hard and soft boards to cloth and carpet rugs, artificial plants/flowers, crockery and cutlery, electronic household machinery, etc. Mostly, they are combustible. Thus, it provides a soft media (for) fire to spread.”

For buildings like these, you are supposed to use fire-resistant construction materials, protect escape routes, install standpipes, and automated suppression systems if you want to follow the Pakistan Fire Safety Provisions 2016 developed by the Pakistan Engineering Council and the National Disaster Management Authority.

Thus, a building that received the SBCA’s completion certificate, but did not have a valid fire safety NOC from KMC lands in a regulatory grey zone. This informalisation of its existence spurs its disposability. This is why the SBCA must be legally barred from issuing completion certificates or any regularising documents, permanent or ad-hoc, if a KMC fire safety NOC is missing.

Financially disposable

It is truly frightening to consider that the losses at Gul Plaza were not limited to what was physically present. One trader, for instance, lost two basement shops with stock worth Rs25 million. He is in debt now because in early January, he bought Eid inventory with Rs2.5 million of credit. “That is all ashes now,” he told Dawn.

The gap between high-end malls and “regularised” plazas is defined by three factors: construction class, accessibility, and the informal nature of the trade itself. Small businesses mostly operate without formal registration, proper invoicing, or documented records of assets and inventory. In the event of a claim, the lack of paperwork makes it impossible for insurers to accurately assess exposure, price risk, or verify ownership. In the eyes of the formal economy, if the inventory isn’t documented, it doesn’t exist — meaning it cannot be insured. This creates a state where assets are physically present but financially “disposable”.

Shopkeepers choose to keep their inventories invisible to avoid the federal or Sindh boards of revenue. “There is a conflict between tax documentation and risk mitigation,” Syed Farrukh Bukhari from UBL Insurance explains. “Traders are often reluctant to insure their inventory because doing so requires a formal declaration of value, which can alert tax officials.”

Overall, insurance penetration in Pakistan is low. Fire and property insurance accounts for approximately 32pc of total non-life insurance premiums, says the Securities and Exchange Commission of Pakistan (SECP). This share is, however, largely driven by industrial properties and undertakings, rather than retail (individual, shop owners, traders, etc.).

The SECP spokesperson said that fire and property insurance coverage was concentrated in industrial and large commercial assets, projects under construction, and properties linked to foreign financing, bilateral government agreements, REITs, or bank borrowing. But even in these cases, insurance is typically obtained to meet mandatory requirements imposed by lenders, investors, or regulators, rather than as a voluntary risk management choice. The SBCA and other provincial building control regulators do not have a mandatory legal requirement for property or fire insurance for commercial or retail buildings.

In a typical shopping plaza, a developer sells individual shops instead of renting them out. Insurance thus becomes an individual responsibility. Large, formal malls get insured for construction to operation (covering labour, machinery, and stock), but this does not happen in fragmented ownership of plazas like Gul Plaza.

Buildings are classed A, B, and C for insurance. Premiums are low for A-class buildings that comply with the rules (as low as Rs5,000 annually for fire coverage on Rs10 million worth of stock). In C-class buildings characterised by old structures, wooden lofts or mezzanines, and encroached corridors, the premium rates skyrocket. In very high-risk areas and extremely low compliance, where even a firefighting unit may have difficulty accessing in case of an emergency, the insurance companies can simply decline.

One possible remedy is a law that makes property insurance a mandatory requirement for commercial occupancy, so public safety is backed by financial indemnity. Insurance companies could recommend the government remove buildings from class C, so more shop owners can be made part of the formal economy.

But all these changes would require the authorities to actually do their job.

Header art by Maaz Jan

The author is an architect and urban planner with over 15 years of editorial expertise in Pakistan’s urban development, economy, and trade. She is currently an associate professor of architecture in Karachi. Her X handle is: @andaleebrizvi