What can we expect from Pakistan's business landscape in 2018?

By: Afshan Subohi

A decade-high GDP growth, contained inflation, expansion in all key sectors, dividends of massive CPEC investment being cashed in and a visible improvement in security and power supply.

Yet it still doesn’t feel like a fresh start.

Are there external vulnerabilities? Can twin deficits reverse the rising tide? Is the growth thrust strong enough to survive political upheaval? Is it sensible for stakeholders cognisant of risks in an election year to hold.

In this special report the Dawn’s Business magazine team reaches out to the key players and attempts to identify crucial drivers to project the trend in focal sectors in the New Year.

The acceleration in economic growth and the political compulsion to focus on voters in 2018 may augur well for the masses. The failure of the system to deliver on the promise of a decent, secure life for all has not weakened citizens’ romance with democracy in Pakistan.

The government’s confidence, however, on its finance team to handle the risks on the external front efficiently appears misplaced.

The challenge of succeeding in raising funds to match loan repayment obligations and finance essential imports may prove daunting. By mid-2018, for lack of other options, Pakistan may find itself back in the IMF fold.

For now, however, people-centric initiatives are expected to improve the quality and coverage of basic public utilities. The expanding job market will improve job prospects and achieve salary increase for the working class.

The inflation graph will look up but it is not expected to get out of control and accelerate into double digits unless there is a major upswing in the global oil market.

The exchange rate may come under pressure because of external sector vulnerabilities but currency dealers do not foresee a major dip after the December seven per cent adjustment in the value of the rupee against the dollar. Assuming everything else remains the same, devaluation by at most 5pc during 2018 is expected.

The year ahead is expected to turn out better for Pakistanis engaged in capital formation in the real sector as opposed to those shuffling assets through speculative businesses. Gamers, gamblers and speculators may be driven out of the mainstream to watch the economy grow from the sidelines.

Business houses may expand their industry and explore new projects in collaboration with Chinese companies. Improved credit access under the new policy may bolster medium and small enterprises.

This under reported sector is considered to be highly potent lending resilience to the economy.

There are multiple factors indicating that the farming community may plough back its profit in the hope of richer dividends in 2018, in an environment where it expects higher demand for its produce and a more congenial government stance.

The community’s expectations may be based on its awareness of the value of rural vote bank for all those who aspire for a political career.

Growth in Pakistan may not be even across all segments of the service sector. While transport, construction and communication may boom the pace of growth in retail and banking may be moderate.

The demand of higher compliance standards and the closer financial engagement with China may necessitate costly adjustments in the banking sector.

In 2018, the retail sector is expected to expand but the pace may be slower, as in an uncertain political situation consumers tend to be less enthusiastic.

An online survey by Dawn to gauge people’s perception on financial expectations in 2018 supported this projection.

The capital market may recover but an upward swing, if at all, is expected towards the end of the year. The brokers’ community, unruffled by the blot on their credibility for unrealistic projections for 2017, continues to sell optimism.

At the start of last year, brokers predicted a 20pc increase in the index in a year. Instead the index took a beating in the second half, dropping by about the same percentage.

It wiped out stakes worth billions of rupees from the markets, hitting retail investors the hardest that had entered the rings too late.

The regional disparities can’t vanish but the growth tide is expected to lift all boats. In the absence of provincial economic surveys, a deeper insight into the regional economies is lacking.

However, on the basis of whatever little information that trickles out of provincial establishments, Punjab will continue to lead while the performance of the other three provinces may be significantly better on both physical and social indicators.

It will be unrealistic to expect meaningful structural or taxation reforms in an election year. There are weak signals of improvement in resource mobilisation as the economy expands, but dramatic happenings on that front look improbable.

The progress on the export front will be slow and tedious. A spike in remittances inflow appears unlikely. The option of financial help from friendly nations will not be available.

Therefore, the danger of the breach of amended Fiscal Responsibility and Debt Limitation Act 2005 can’t be ruled out.

“A bolt from the blue or a major misadventure by the self-professed guardians of national interests can disrupt the trajectory of progress but the chances are slimmer in a changed world with growing Chinese stakes in Pakistan,” commented an economist sympathetic towards the PML-N.

The conflicts in a transformational country can’t be wished away. Some friction and fireworks will probably persist in the foreseeable future beyond 2018, but busting the limits of the constitution might be unviable for even the most ambitious lot, with China now watching over their shoulders.

“As long as the game is inside constitutional boundaries, the thrust of growth with $25 billion investment in infrastructure under the CPEC has generated enough steam to keep the economic train moving at a higher speed,” commented a retired bureaucrat now working on a World Bank project.

The political opponents of the government find the perception unrealistically simplistic.

In their complete distrust of the politicians, they are betting on a government of technocrats to carry out corrections and structural reforms and ensure rich dividends for Pakistan from the CPEC.

They tie the good fortunes to the exit of PML-N from the political scene for once and for all.

In its remarks at the end of the post-programme review meeting in early December, the IMF warned, “Maintaining this positive trend will require strengthening the economy’s resilience with greater exchange rate flexibility, fiscal discipline, and an adequately tight monetary policy stance”.

By: Jawaid Bokhari

The economy is taking a new direction where improvement in variable macroeconomic indicators is likely to be more long-lasting.

The new year bring hopes and fears.

Let’s start with the positives.

It is probable that the current upturn in output of large-scale manufacturing (LSM) and the resultant surge in export earnings may spill over into the whole of next year thereby reducing the trade deficit and shoring up its contribution to GDP.

Nonetheless, the risk to economic growth sustainability from vulnerabilities of the external sector still persists. Rising imports have hit a new record.

However, policymakers can take some comfort in the observation made by the IMF Mission Chief Harald Finger that Pakistan has not sought a bailout so far. That means that there is no risk of any debt default in the near term.

Even if Fitch’s forecast of risks to the external sector rising in the medium term is accepted, the economy in the current calendar year is likely to muddle through to record a moderate growth rate.

Mr Finger had estimated last month the GDP growth rate at 5.6pc for fiscal year ending in June — a bit higher than earlier World Bank forecast of 5.5pc, but lower than the year’s target of 6pc set by Islamabad.

The risks perception, however, gets accentuated owing to political uncertainties arising from elections scheduled for the middle of the next year with divisive politics and institutional frictions going haywire.

On the other hand, the current political stalemate indicates that the status quo will largely prevail though some space may be created for political manipulations after the electoral verdict.

There is very little room to speculate on policy changes as there is an unwritten national consensus among mainstream political parties on fundamentals of economic policy framework.

Notwithstanding the diverse perceptions and mixed trends, the economy is taking a new direction where improvement in variable macroeconomic indicators is likely to be more long-lasting since they come on the back of improved energy supplies, upgrade of technology infrastructure facilities, etc.

No less important is capital spending, funded by diverse sources, on a scale and mix rarely witnessed in this country.

CPEC projects, vital for the integration of the national market and regional connectivity, are largely being financed by the Chinese.

The balance-of-payments support is coming from the auction of Pakistani bonds with tacit support of the IMF without the Fund’s stabilisation programmes but through advice to pursue a flexible exchange rate policy to reinforce the international confidence.

The World Bank and Asian Development Bank are making joint efforts to improve governance, systems, build institutional capacity, provide technical and financial assistance for a wide range of economic and social activities including measures to bring agriculture into the market economy.

How these financial and capital inflows would ultimately and directly impact the external sector is not clear, but they have the potential to help Pakistan build a vibrant and robust economy in the long run that can take care of trade deficits and balance of payments on its own.

The two vital sectors (LSM and exports) are unlikely to lose their growth momentum with impetus provided by the sharp rupee depreciation and reduction in custom duties on selected industrial raw materials to further support their upturn in both production as well as exports.

Before this impetus, in five months of this fiscal year, LSM’s output grew by 9.64pc year-on-year and the overall export earnings went up by 11.8pc.

Much of the growth in imports can be traced to Pakistan’s trade with China.

With the exception of oil, Pakistan’s top imports come from its neighbouring country whether it be capital goods, industrial raw materials or cheap consumer items that accounted for $13.9bn in 2016-17.

With exports at $1.4bn, the bilateral trade gap touched $12.5bn. That accounted for more than one-third of the country’s trade deficit of $32.5bn recorded in that fiscal year.

The China-Pakistan Free Trade Agreement, which became effective in July 2007, has turned out to be primarily one-way street, more so since the launch of CPEC — the game-changer.

While the existing currency-swap arrangement, if successfully activated, may ease the pressure on Pakistan’s balance-of-payments position for some time, the two sides must meanwhile also try to boost Pakistani exports to China.

For exporters, earnings in yuan may not be as attractive as in dollars. And it may not be so easy to dislodge the greenback’s entrenched position in the Pakistani currency market.

So far the domestic economy has shown great resilience against external vulnerabilities and has continued to expand at a moderate pace.

The share of domestic consumption in GDP shot up to 94pc in 2016-17 from 90pc recorded over the previous 10 years.

Much of the market is growing on its own momentum. In an expanding economy, the investment-to-GDP ratio edged up slightly.

The overall outlook for 2018, therefore, is essentially positive.

By: Khaleeq Kiani

Prime Minister Shahid Khaqan Abbasi expects the country to achieve six per cent growth in 2018 and to set the stage for an even higher trajectory with an all encompassing sectoral expansion after successful elimination of key barriers — energy and infrastructure — through concentrated efforts over the past four years.

In an interview with Dawn, the prime minister identified the external account and security situation as manageable risks but noted that economic fundamentals were strong enough to sail through challenges. The following are the details:

1) How do you expect the economy to perform in 2018 in terms of growth, job creation, inflation and trade?

A. Pakistan has seen a visible economic turnaround over the last four years due to the successful implementation of a comprehensive programme of economic revival aimed at higher economic growth and macro-economic stability.

The growth momentum remained above 4pc for the last three years and reached a decade high of 5.3pc in FY2017.

Due to the expansion in real economic activity, economic growth in FY2017 was not only the highest in a decade, but was also broad based.

Growth FY2018

The government is confident that economic growth will continue its upward acceleration in 2018 and beyond. For FY2018, the GDP growth target has been set at 6.0pc. Our estimates are that Agriculture will grow by 3.5pc, Industry 7.3pc and Services 6.4pc.

The production estimates of major crops such as cotton, sugarcane and rice are very encouraging. Also, disbursement of agriculture credit during July- October FY2018 has shown over 50pc increase compared to last year.

As for the industrial sector, the momentum of robust growth built during the three years is likely to further increase in FY2018. Large-Scale Manufacturing (LSM) growth performance of 9.64pc during July-October FY2018 clearly points in that direction.

It is also encouraging that this higher growth is derived from across all the industrial groups such as; automobiles (28.48pc), iron and steel (44.39pc), electronics (65.03pc), engineering products (15.29pc), coke and petroleum (15.67pc), food, beverages, tobacco (14.24pc).

In the services sector, wholesale and retail trade and transport and communication are growing in line with the improved performance of agriculture and industrial sectors. We are confident that our efforts aimed at improving ease of doing business will further augment the performance of this sector and it will continue to show healthy growth.

Job creation

As a result of various projects and programmes, aimed at improving employment levels, the unemployment rate has decreased from 6.2pc in 2012-13 to 5.9pc in 2014-15.

We expect that the initiatives including CPEC will create millions of new jobs in the country in all sector of the economy in the coming years. Going forward, the government has targeted 7.0pc GDP growth in the medium-term to absorb the growing labour force.

Inflation

Although there is an increase in aggregate demand owing to the increase in economic activity along with the increase in global prices, the effective monetary and prudent fiscal policies have anchored inflation and we expect that it will remain within the target of 6pc during the current fiscal year.

Trade

The trade deficit during FY2017 increased by 37.8pc to $26.6bn. Imports were higher by 17.6pc to $48.5bn while exports were down by 0.15pc to $21.9bn. The widening of trade deficit was accompanied with a decade high level of real GDP growth.

Consequently, the pickup in economic activity, along with investments in CPEC projects, has created demand for machinery, petroleum products and other productive imports.

At the same time exports declined due to the subdued global demand and depressed commodity prices.

However, exports have started recovering since the third quarter of FY 2017, partially offsetting the decline observed in the first half of FY2017.

The exports-related incentives such as reduction in rates of export re-finance facility, the long-term finance facility, the prime minister’s export package (Rs180bn), incentives provided to textile, leather, sports goods, surgical goods and carpets as part of a zero-rated sales tax regime, drawback of local taxes and levies as well as improved global outlook have started to produce results: exports during July-November 2017-18 increased 12pc over the same period of last year.

On the import side the government has taken many measures for the rationalisation of imports such as 100pc cash margins on LCs, discouraging non-essential imports through non-tariff adjustments, and an increase in regulatory duties on existing and new tariff lines.

All these endeavours are geared towards bridging the trade deficit. Other measures aiming at enhancing the level of foreign remittances will ensure that the current account deficit is kept within manageable limits.

2) In an election year what will be the key drivers of growth in Pakistan where the private sector is reputed to be risk averse?

A. The key drivers of growth in Pakistan will be production (real sector — industry, agriculture, services) as well as investments.

In terms of investments, the federal Public Sector Development Programme increased from Rs348bn in 2012-13 to Rs733bn in 2016-17, while the credit to private sector (flows) has also seen a remarkable increase from negative Rs7.6bn in 2012-13 to Rs748bn in 2016-17.

The number of companies incorporated has increased significantly from 3,960 in 2012-13 to 8,286 in 2016-17.

Credit to private sector has also increased to Rs105bn during July-November 2017-18 compared to Rs60bn during the corresponding period last year.

Agriculture credit disbursement also improved by 43pc in July-November (Rs294bn compared to Rs206bn last year). FDI increased by 57pc ($1,146m in July-November 2018 compared to $729m a year ago).

The private sector in Pakistan was once reputed as risk averse. However, the situation is improving. The provision of a better regulatory framework through the promulgation of the new Companies Act 2017, Benami Transactions Prohibition Act, Securities Act 2015, Futures Market Act 2015, Corporate Restructuring Companies Act and several other legislations are some of the structural improvements which are helping to improve the corporate landscape.

3) What are downside risks that could derail the economy?

A. The government recognises that external factors, e.g. lower exports, tighter international financial conditions and a faster rise in global oil prices, could pose risks to Pakistan’s economic outlook. The government is cognisant of these potential challenges and is taking measures to address them.

Various measures are taken to increase exports, increase remittances and reduce non-essential imports. A minimum of 10 pc increase in exports is being targeted which is likely to generate additional $2bn export proceeds (the increase so far is 12pc over the last year).

The Strategic Trade Policy Framework is being implemented, with focus on product and market diversification, institutional development and trade facilitation. The PM’s Export Package of Rs180bn is under implementation and an uninterrupted supply of gas and electricity to the industry is being ensured.

The agriculture support package announced in 2016-17 to boost agricultural production is also contributing. And to reduce non-essential Imports 100pc cash margin on LCs, non-tariff measures and regulatory duties on non-essential imports have been imposed.

4) Is there a plan in place to avert an external front crisis if foreign exchange position falls to unsustainable risking default?

A. The external sector poses a challenge which is being tackled through various measures. The challenge, however, is not of a magnitude that it could lead to a crisis.

The State Bank of Pakistan’s foreign exchange reserves which were at the lowest level of $2.829bn in February, 2014 increased to $14.05bn as on 21st December, 2017.

The issuance of Eurobonds and sukuk worth $2.5bn and the policy of exchange rate flexibility being pursued by the State Bank has also helped in reducing external imbalances.

The government is actively working on other options and several proposals are under consideration, should a need arise to build on the existing measures to improve the external balance.

5) What are the weaknesses of the economic fundamentals and what are key fundamental strengths?

A. For many years the large energy deficit, as well as the adverse security situation, was the most telling weaknesses for the economy. Other challenges included low tax-to-GDP ratio as well as low savings- and investment-to-GDP ratios.

Non-diversified exports in terms of markets and products have remained another challenge. The present government has taken a number of measures to address these weaknesses.

The security situation in the country as well as energy supplies has considerably improved. Efforts are underway to broaden the tax base. The investment-to-GDP ratio is persistently improving. The Strategic Trade Policy Framework is focusing on export diversification and value addition.

In terms of fundamental strengths, Pakistan has a vibrant economy with strong contributions from industry, agriculture and services sectors.

With the improvement in energy supply and removal of structural impediments, all sectors of economy have been showing sustained and higher growth during the last four years.

Pakistan is also endowed with large deposits of natural gas as well as minerals such as coal, copper, gold, rock salt, iron ore, chromite, sulphur, marble etc.

Pakistan also has the demographic advantage of a young population which allows us to have a large domestic workforce of both skilled and unskilled labour, as well as exportable manpower which continues to be a strong source of foreign remittances.

Our country’s location as an economic corridor between Central, South and West Asia as well as access to the Arabian Sea is also a fundamental strength.

We are pursuing several multilateral regional connectivity initiatives, including the flagship CPEC, to take full advantage of our geographic location.

By: Dilawar Hussain

The positivism of big brokers and equity strategists has been sparked by the clarity on the political front, which for most of 2017 was shrouded in uncertainty.

If those who invest in Pakistani stocks are ruffled and glum-faced on the eve of the new year, they have good reason to be, as much went wrong during the outgoing year.

Unlike at the end of 2016 when brokers and investors were dancing with glee on having made fortunes owing to a mouth-watering return of 44pc on their investment — highest among Asian markets and second best in the world — investors in the local bourse are staring at a negative return of 15.3pc in 2017.

The benchmark KSE-100 index of the Pakistan Stock Exchange (PSX) sank 7,335.49 points during 2017 to close the year at 40,471.48 points.

Misfortune befell late entrants into the market for they lost more than a quarter of their savings as the stocks started to tumble from May 25 when the index peaked at 52,876 points.

The reversal that the stock market took in mid-May stunned even the best analysts.

Overjoyed by the performance in 2016, the top pundits were predicting the KSE-100 index to cross 62,000 points in 2017.

But such hopes were dashed to dust, for the market has a mind of its own.

Not many people take Warren Buffett’s warnings seriously who once told shareholders: “Anything can happen anytime in markets. And no adviser, economist, or TV commentator — and definitely not Charlie nor I — can tell you when chaos will occur.”

And the chaos in the Pakistan stock market occurred with the announcement of the budget 2017-18, which burdened equity investment with new taxes. It was followed by the debacle of Pakistan’s relocation to MSCI’s emerging-market index from the frontier-market category.

Regulators, fund managers, institutional and individual investors had exhausted all the cash in buying stocks that they were sure foreign investors would swoop in to add to their portfolios once the Pakistani bourse was upgraded. That, however, was not to be as the market witnessed heavy outflows instead of the expected inflows.

Then, in the last six months of the year, the country was embroiled in political and economic uncertainties, which refused to provide respite to the market.

But optimists are looking at the turn of the tide in 2018.

Brokerage JS Global observed in its strategy report: “We expect the market to pare most of the losses of 2017 in 2018 by setting December 2018 index target of KSE-100 index at 47,000 points.”

However, the report said the returns are likely to be skewed towards the second half of 2018, when “we expect clarity on domestic politics and economic policies to emerge”.

Topline Securities believed that Pakistan’s price-to-earnings ratio could potentially be in the range of 8.5-9 times by the end of 2018, providing 22pc to 29pc upside from current levels.

PSX chairman Muneer Kamal affirmed that the market had all the reasons to rebound. He asserted that the overall direction of the economy was on track including growth rate, inflation and interest rates. “Yes, there are issues with the current account deficit,” he said, but he argued that those could be overcome.

Following the rupee devaluation, the Pakistani market would be back on the foreign fund managers’ radar due to its attractive valuations, he said.

“There is every likelihood of emerging-market foreign flows in 2018,” Mr Kamal, who is also the SECP-nominated director on the bourses’ board, said, adding that that with sizeable free-float held by foreign investors, their entry could turn the market around and boost the confidence of local investors.

He said mutual funds, banks and foreign investors (with 30pc Chinese investors’ stake in the market) would all be anxious to set a positive direction for the market.

The optimism of big brokers and equity strategists has been sparked by the turn of tide on the political front, which for most of 2017 was shrouded in uncertainty.

After five weeks of battering, stocks gained over 2pc in the week preceding the one before the close of the year as the passage of an important bill by the Senate dispelled doubts about elections being held on time and the briefing of the Army chief to the Senate comforted investors that the democratic process was not to be derailed.

Arif Habib, a former chairman of the stock exchange, concurred with the views of Mr Kamal, stating that the outlook for the market in 2018 was positive with the hope that reasonable returns would be netted by investors.

He thought there could be an uptick in interest rates which might leave a healthy impact on banks’ bottom lines.

The devaluation of the rupee may help reduce pressure on the external account; it is likely to give a boost to exports and import-substitution industries. Since the power sector and exploration and production receive dollar-based returns, their earnings could also increase.

Many market experts do not subscribe to the story of an imminent rally. They contend that the KSE-100 index may continue to move sideways until the elections.

A Topline analyst, however, displays charts and graphs to show that in the last 25 years, Pakistan’s equities have always surged by 12-22pc on an average in three- to six-month period prior to the elections.

By: Mohiuddin Aazim

Banks will have to learn and unlearn many things to keep up with the changing financial environment.

Banks’ private sector lending remained robust in the outgoing year, and the growing economy guarantees further acceleration during this year.

Small and medium enterprises (SMEs) received increased attention of banks last year, a trend they can expect to continue.

By the end of 2017, the State Bank of Pakistan (SBP) introduced a policy to promote SMEs that envisages a more enabling regulatory environment for banks to extend fatter loans to a larger number of SME borrowers.

The central bank also allowed export refinance from banks to SMEs operating in eight export-oriented sectors including IT, food processing and printing and packaging.

A big challenge for banks in 2018 will be to build credit appraisal capacity and augment internal controls to keep the infection ratio of SME financing at sustainable levels.

In fact, the SBP has already required banks to adopt non-financial advisory services in their SME banking strategy for this purpose.

Under the new policy, microfinance banks (MFBs) have also been permitted to lend up to Rs1 million to a microenterprise employing up to 25 individuals. This will certainly boost demand for microcredit, help MFBs cut their cost of lending and brighten business opportunities.

Here again, the challenge for MFBs is that they’ll have to enhance their capital base and ensure readiness of handling larger microenterprise loans because, under new rules, they will have to satisfy the SBP on such counts before committing more than Rs500,000 loan to a microenterprise.

Generally speaking, credit quality of banks changed for the better in 2017 with a larger amount of private sector loans offered for fixed investment.

This should help companies, particularly those in the manufacturing sector, to improve quality and output of products and would, thus, lead to further demand for private sector loans.

More lending for fixed investment in 2018 can be predicted safely as CPEC investment in big-ticket energy and infrastructure projects in 2016 and 2017 have created demand for such investment in corollary industries.

Also related to CPEC are some prospects and challenges for banks that will unfold in 2018 and beyond.

Banks have already undertaken massive CPEC-related financing projects and will continue to do so in this and many years to come.

Project financing characteristics will be defined anew with greater interaction of local banks, with two Chinese banks already operating in Pakistan.

They will have to learn and unlearn many things when it comes to consortium lending with significant participation of the Chinese banks; and in dealing with Chinese companies and corporate consortia made up of local, Chinese and other foreign companies banks will have to rely more on complex structured finance than simple lending portfolios.

In so doing, issues might crop up in complex credit proposal assessment and monitoring of big multi-pooled loans.

The continuity of low interest rate regime through 2017 may get a break in 2018 for two reasons: first, the demand for bank credit is growing and, second, a weaker rupee that may have to be allowed to shed more weight in the next year as well.

Deposit mobilisation may become quite challenging in 2018 if a lax monetary policy is allowed to continue. Both companies as well as individuals are fed up with extremely low bank deposit rates that, in some cases, have already turned negative with a spike in headline inflation.

Even average fresh bank deposit rates may soon turn negative with demand-push inflation building up in the economy.

Here again, much depends on how the monetary policy tool is used to strike a balance between economic growth, inflation and stable yet realistic exchange rates.

Digitalisation of the financial services and phenomenal rise of fintech may serve as a catalyst for banks’ business through improved identity management and consequent ease for banks to reach out to underserved segments of depositors and borrowers.

But these developments would keep banks on their toes to ensure digital transformation of their back offices, IT managers warn.

Besides, compliance of regulatory requirements such as the recently introduced SBP regulations on branchless banking for promoting home remittances would also add on to banks’ “do more” list of digitalisation work.

On Dec 22, the SBP asked all banks, Islamic banks and microfinance banks to “facilitate swift and cost-effective inflow of home remittances through branchless banking”.

They are now required to open special online accounts for people in Pakistan who receive remittances sent back home by their relatives and enable them to withdraw up to Rs50,000 from these accounts on a daily basis with a monthly cap of Rs500,000 rupees.

Since the move would not only boost overall inflow of remittances via official channels and thus help in minimising the surging external sector’s imbalance, it would mean more business for, and greater outreach of, banks.

In 2018, an operational area of banking wherein banks would remain both excited and challenged is growth of lending to private sector by Islamic banking branches (IBBs) of conventional banks.

For many years, Islamic banks dominated such lending and IBBs of conventional banks thrived alongside.

But senior bankers who oversee the flow of private sector lending say this trend might now change.

By: Mohiuddin Aazim

When sanity prevails, sanctity of economic fundamentals is ensured.

On July 5, 2017 sanity prevailed and the State Bank of Pakistan (SBP) set the rupee from an artificial trading band through a market-based mechanism.

But that sanity was lost in no time as the then finance minister, Ishaq Dar, audaciously compelled the central bank to reverse the move.

On Dec 8, sanity prevailed again when the central bank once again loosened the trading band of the rupee, forcing it to shed some value — and this time no one from the government objected to the move.

By the end of July, Nawaz Sharif had been disqualified as prime minister on the orders of the Supreme Court and replaced by Shahid Khaqan Abbasi. By end-September Ishaq Dar was convicted by an accountability court, and he was declared an absconder on Nov 21.

The sanctity of exchange rate has been ensured, at least for now.

This sort of fiddling with the economic indicators is unfortunate: it creates a bad image of the economy, creates confusion in markets and leaves everyone, including businesses and local and international investors, guessing about things that should be predictable.

In theory, Pakistan is practising a free exchange rate regime, but keeping in view the sensitive role that exchange rates play in an economy like ours, the central bank keeps the rupee in a certain rate-band to avoid volatility beyond control.

This is understandable. What is beyond comprehension is that fiscal authorities rather than the central bank want a final say in deciding when to loosen or tighten that trading band.

A modest 4.8pc depreciation of the rupee, between Dec 8 and Dec 12, 2017, still leaves the rupee overvalued, if its parity with the dollar is examined by the Real Effective Exchange Rate (REER) index.

But most bank treasurers and forex dealers believe that the central bank will not let the local currency fall any more — at least in the next two quarters, ie till June 2018.

After the slide of the rupee, inflation has spiked but it is difficult to predict whether a modest depreciation — and that too at a time when the economy is not suffering any supply side setbacks — can impact inflation numbers significantly.

It’s a separate story, though, that demand-pull inflation has already been in sight as the economy is growing fast. Coinciding this with a weaker rupee might keep general prices higher in 2018 than in 2017.

After the rupee’s depreciation, bankers are hoping for some tightening of the long-held easy monetary policy but central bankers say any decision in this regard is taken, and will continue to be taken, on the basis of overall assessment of the economic conditions in the country.

In simpler words, monetary policy tightening remains a distant possibility as the most pressing case for such a move — a worrying build-up in inflationary pressure — is nowhere in sight, productive sectors of the economy are doing reasonably well and SBP is vigilant enough to use central banking tools to keep broad money supply in line with the set targets.

By: Nasir Jamal

Politics is likely to weigh heavily on investment decisions of companies and businessmen in 2018 because of worsening political strife and threat of protests by certain opposition parties and religious groups ahead of the upcoming elections.

However, economic analysts and businesspeople say economic growth prospects proffered by improved energy supplies and security conditions, as well as new business opportunities opening up under the multibillion-dollar CPEC initiative will keep new investments coming in despite political uncertainty.

“Despite concerns, the industry believes the political situation will improve and uncertainty will ease in the next several months… the government will complete its term and the elections will be held on time,” argues Saad Hashemy, chief economist and director research at Topline Securities.

This means investors will largely start returning to the market and companies will begin implementing their expansion plans as the country moves towards the new elections.

Syed Nabeel Hashmi, a leading auto parts manufacturer and exporter, agrees. “Indeed, political changes do affect investment decisions because businesses like stability. But I think the lull in investment in the first half of 2018 is not going to break the growth momentum,” he says.

“I think the elections are going to generate a lot of economic activity, and create new business opportunities and jobs. Unless there is widespread political disturbance and violence, I see the economy and private business grow pretty fast in 2018, despite it being an election year,” he says.

Triggered by disqualification of ex-prime minister Nawaz Sharif by the apex court in a corruption inquiry linked to the leaked Panama Papers, concerns about the premature dismissal of the PML-N government and possible delays in the next polls had deepened.

This was because of the two-week-long lockdown by a religious group — on changes in the oath of elected public representatives — and the last-minute refusal of PPP and PTI to support the delimitation bill.

Ever since, the protest sit-in has been called off, the delimitation law passed and fears about future of government dissipated.

Even if the country’s exports have slowed down and fallen by almost a quarter in the last three years, Mr Hashmi feels that domestic demand continues to rise rapidly.

“From auto, steel and cement to food, white goods and pharmaceuticals, you know, there is double-digit growth everywhere,” he says.

“Our GDP is growing by almost 7.5-8pc due to increasing domestic demand if we also take our large undocumented economy into account. No domestic market-based investor or company focused on consumer market can ignore this trend and stop investing in capacity enhancement, no matter what the political conditions in the country are.”

Quratul Ain Irfan, vice president of a pharmaceutical company, says the overall economic outlook for 2018 looks promising, with the CPEC taking shape and reduction in energy shortages.

“Pakistan’s economic outlook is quite bright. Cement, steel, chemicals, food, pharmaceuticals and consumer durables should do well despite election-related political activities,” she says.

The share of consumption in Pakistan’s GDP has increased to nearly 94pc, up from around 90pc during the last 10 years, according to the State Bank of Pakistan.

But the investment-to-GDP ratio has edged up only slightly to around 15pc despite a substantial increase in import of machinery and credit for fixed investment during the last couple of years.

Ehsan Malik, chief executive officer of the Pakistan Business Council (PBC) that represents the country’s large local and foreign companies, agrees that market-based firms have been investing in capacity expansion as domestic consumption has grown pretty fast over the years.

But he cautions that the “economy will remain on the edge as our consumption is high and mostly import-reliant. The demand has far surpassed (domestic) supply (on the back of rising household income in rural as well as urban areas, and the projects under the corridor initiative) and is being met with imports. It is because our failure to develop a strong, efficient manufacturing base that our exports remain weak and we have sought 12 bailouts from the International Monetary Fund in the last 30 years”.

Analysts like Azfar Akseer, chief executive officer of Akseer Research, do not expect any new major industrial project being launched in 2018. Though he says the steel, cement, food, automobile and consumer appliances companies that have already announced their expansion plans will stick to their investment plans and timeline.

“As far as new greenfield investments are concerned, I think local and foreign investors will wait for the announcement of the incentives for the Special Economic Zones (SEZs) under the CPEC before making any meaningful investments in manufacturing. And I don’t see that happening any time soon, at least not before the elections,” he says.

Mr Malik does not feel that any local or foreign investor will, in the near to medium term, invest in export-oriented sectors like textiles. “Our exports are down because we have become uncompetitive in the world. Most of the foreign investment (excluding Chinese investments under the CPEC) has been made in existing businesses focused on the domestic market.

“No job is created and no export dollar earned. In fact, this kind of investment will add to pressure on the external account once investors start repatriating profits. Unless the government implements meaningful governance, regulatory, policy and tax reforms, the chances of stimulating investment in the export-oriented sectors will remain a distant dream and we will continue to borrow money to pay our bills,” he says.

By: Mubarak Zeb Khan

The structure of the economy has undergone significant changes with the growing share of services.

No doubt the size of the GDP has expanded over the years, but the growth was mainly driven by the services sector instead of real economic sectors like agriculture and manufacturing. This is evident from a 10-year data of service that suggest its contribution to national economy jumped to almost 60 per cent in 2015-16 from 54pc in 2005-06.

The size of the industrial sector in the overall economy has lowered to 21.01pc from almost 22pc, while that of agriculture fell to 19.8pc from 23pc, respectively.

It seems that as a result of difficulty in operating in the manufacturing sector, small and medium investors are registering companies in the services sector.

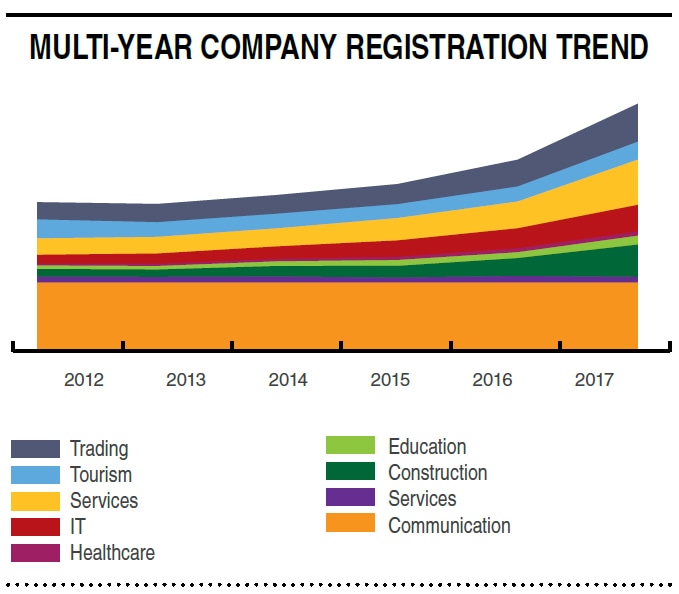

This trend is clear from the past six years of data regarding registration of new companies with the Securities and Exchange Commission of Pakistan (SECP).

The lion’s share of registrations was in nine areas: communication, construction, education, healthcare, information technology, services, tourism and trading.

There are a few other sectors which also witnessed sizable registration of companies such as real estate development.

As per official figures, the share of the nine sectors in total registration of new companies was 60pc or 2,325 in 2012 out of total 3,926 companies. In the following two years — 2013 and 2014 — the share of these companies in overall registration fell to 57.3pc and 59.4pc, respectively.

It was in 2017, when the share of all these companies in total registrations reached an all-time high of 83.2pc or 5,163 companies out of total 6,200 companies. Nearly 42,000 companies were registered alone in these nine sectors till June 2017.

It is because of this huge investment in these sectors, the share of wholesale and retail trade in the services sector stood at 18.2pc, with the next biggest share goes to transport, storage and communication which stood at 13.3pc.

According to the official SECP spokesperson, the increasing rate of corporatisation that can lead to documentation of economy is one of the core objectives of the SECP.

In pursuance of this goal, the SECP has taken a host of reform measures, which have resulted in robust corporate growth in the country, leading to formalisation of the business sector and documentation of the economy.

The landmark reform in this regard is the passage by parliament of the Companies Bill of 2017, which aims at easing doing business.

The significant measures aiming at promoting a business-friendly environment include simplifying the registration process by elimination of the requirement of third party digital signature, launch of new User Registration System under eServices, substantial reduction in cost and turnaround time and development of modified Virtual One-Stop Shop portal and its successful integration with the FBR for NTN registration.

In the World Bank’s 2017 Doing Business Report, Pakistan’s overall ranking has improved by four points from 148 to 144. “We are optimistic that the recent SECP reform measures would result in further improvement in Pakistan’s ranking in the doing business indicator,” the spokesperson added.

But for FPCCI President Zubair Tufail this development is not good for the overall health of the economy. He said that the services sector is booming because of fewer regulations and hassles, and that industries and services should be developed and facilitated at the same time.

He added that he had also informed the prime minister and newly appointed adviser on finance about the shrinking manufacturing base in the country.

He expects the government may announce reduction in electricity and gas tariff for industrial sector in the next year.

There are economists who look at the fast growth in the service sector as a normal process. However, services should not develop at the cost of manufacturing which would result in erratic rate of growth.

Analysts believe the growth in information technology, retail, tourism, and construction will continue to grow in the year 2018.

Communication

In 2018, the government plans to auction 3G and 4G in Azad Jammu and Kashmir and northern areas. It is also considering testing 5G spectrum next year. Moreover, there is an additional demand for auction of 3G/4G in the market.

Tourism

After devolution, domestic tourism has witnessed substantial growth.

In 2018, all provinces plan to promote domestic tourism. KP has emerged as the leading province with plans to attract more than 20 million domestic tourists. Balochistan plans to develop 64 sites to enhance natural and heritage tourism while Sindh and Punjab also have similar plans.

By: Mohiuddin Aazim

Wheat, sugarcane and rice are all heading in the right direction and we may see additional output and yield enhancement this year.

The prospects of key crops and livestock sector in 2018 are somewhat promising but structural issues remain and need increased attention.

Only three out of five key crops are expected to do well, showing an increase in production and a modest growth in yield, and the livestock sector also seems set to perform better than the year before.

Wheat, sugarcane and rice are all heading in the right direction and we may see additional output and yield enhancement this year.

Officials and growers say output of maize, however, may either remain stagnant or record a slight decline due to multiple reasons. If all goes well, cotton output, too, may touch the 13 million bales mark but would still remain below the original target of 14.04m bales.

Two key challenges to crops that have so far continued to haunt the agriculture sector might also remain in sight in 2018 even if their severity weakens.

The first is to bring national average yield of key crops closer to the global average and the second is to improve supply and the value chain.

How closely we chase the objective of bridging the yield gap depends upon how seriously ongoing yield enhancement programmes based on seed research and modernisation of farming practices are implemented.

Lethargy on this count would not only result in slower growth of the crop sector but would also constraint the country’s ability to meet growing demand for food grains and cotton at home, and to achieve desired growth in export of grains, food items and textiles.

If distortions in supply chain of crops are not managed well the country can neither maintain a sober inflation nor get high per unit value for food and textile exports.

Cotton: The current season’s cotton output looks set to exceed 13m bales against the second assessment of the cotton crop assessment committee. This is by no means a very optimistic assessment as by mid-December the country has already produced 10.685m bales.

Sindh is sure to contribute 4m bales, up from earlier estimates of 3.7m bales—a number already achieved by mid-December.

However, even a 13m bales output would not only be lower than the original target of 14.04m bales but also insufficient to cover growing demand from the textile sector after the recent spike in textile exports.

Had Punjab’s cotton output not come under pressure (despite increase in the area under cultivation) due to climatic reasons, total national production would be around 13.5m bales.

Wheat: The target for wheat output in the upcoming season is 26.46m tonnes, up from 25.75m tonnes in the previous season.

Shortage of irrigation water and none or lesser rains in some wheat growing areas might make the achievement of this target difficult, according to a Suparco assessment.

But officials of provincial agricultural departments say, on the basis of field reports received so far, that the target could be achieved despite some reduction in the area under cultivation.

They are pinning their hopes on projected increase in yields, thanks to introduction of some new varieties in the past couple of years and greater awareness created among farmers about proper care of the crop.

According to Dawn reports, experiments on winter wheat are being conducted in four high altitude regions. If encouraging results emerge, the country will begin growing this crop as well, though on a limited scale. Winter wheat crop is expected to offer 20-30pc higher yield than spring wheat — an added advantage.

Rice: Rice harvest in 2017 is estimated to have reached 7.55m tonnes, according to officials who say that in 2018 production would cross eight million tonnes even if the area under cultivation remains the same.

Their optimism springs from a faster growth in production of coarse rice — thanks to expanding use of high-yield varieties— and a modest increase in even Basmati rice.

For several years, Pakistan has been promoting use of paddy seeds that survive and grow on less water and has also been teaching farmers how to reduce post-harvest losses.

Mechanised paddy harvesting and newer techniques of replanting of saplings, too, have been playing their role in boosting rice output for some years now. Hopefully these trends should become stronger in 2018, officials of the Ministry of National Food Security and Research (MNFSR) say.

Sugarcane: Sugarcane output has been growing steadily leading to surplus sugar production in the country and a crash in domestic prices.

Sugar exports continue to bring in much-needed foreign exchange into the country. Delays over fixation of support price of cane by provinces continue to occur incessantly and the year 2017 was no exception.

Farmer lobbies persist in demanding upward revision in support prices even when the same are notified. The same is expected to happen in 2018.

But on sugarcane farms we can expect changes: a straight 10pc increase in cane production (to 89m plus from 81.4m tonnes in 2017) and a rise in per-hectare yield to 64 tonnes per hectare from 62 tonnes per hectare, according to initial official projections, not yet finalised.

Maize: Maize output that exceeded 6.1m tonnes for the first time in 2017 may remain under pressure in 2018 for the simple reason that the 2017 output gain came from a big 12pc increase in the area under cultivation.

In 2018 this might not be the case and the area under cultivation would rather shrink, officials say, adding that total production could range between 5.3m and 5.5m tonnes.

They are, however, optimistic that the per-hectare yield of a little less than 4.6 tonnes in 2017 may actually rise to 5 tonnes per-hectare due to wider adoption of high-yield varieties of the grain.

Livestock: In the absence of data obtained via physical animal surveys, authorities continue to make calculations about milk and meat production on the basis of inter census growth rates between 1996 and 2006.

Much has changed since 2006 and the entry and progress of large milk and meat processing companies have changed the entire landscape of value-added livestock industries.

Increase in economic growth, consequent rise in income levels in recent years and proliferation of chains of super markets also continues to boost demand for dairy and milk products. That is why officials of MNFSR remain upbeat about growth in the livestock sector in 2018.

But whether an anticipated growth in the sector’s performance would also help in export of meat and meat preparations and of food items in which milk is used as the main ingredient, cannot be predicted right now as competition in export markets is getting tougher.

One way of looking at high impact of grains and livestock sectors’ performance could be the growth of the food and beverages segment of large-scale manufacturing.

Here, an 11.49pc expansion in output of this segment in FY17 topped by 14.24pc further growth in five months of this fiscal year indicates that things are moving in the right direction.

By: Mohammad Hussain Khan

While water and agriculture experts in the country keep highlighting issues that have by now assumed critical proportions, the commitment to addressing them seems to be missing; while a rapid increase in population has increased water demand.

Experts believe 93 to 95 per cent of Pakistan’s total surface water/freshwater is utilised in the agriculture sector and, according to a Water and Power Development Authority (Wapda) presentation, the country has the lowest productivity per unit of water i.e. 0.13kg/m3 with India at 0.39kg/m3 and China 0.82kg/m3.

The agriculture sector’s contribution in GDP remains at 21pc but progressive growers agree that given the quantum of surface water utilised in the farm sector its efficiency leaves a lot to be desired.

Despite shortcomings Pakistan comes up with lesser per hectare yields of wheat, cotton, sugarcane and rice when compared with countries like Australia, America, Egypt, Turkey, China, Germany and France according to Pakistan Ministry of National Food Security and Research 2014-15 statistics.

But policymakers have to go beyond the rhetoric on integrated water resource management to be ready to face the challenges ahead if they aim to offset the impact of water scarcity.

The country’s water challenges could be put into the following categories: inadequate storage, conservation, lack of water efficiency leading to lower per acre productivity, unchecked groundwater abstraction and rationalisation of water pricing, canal inefficiency, contiguous but dilapidated irrigation infrastructure.

Under the Falkenmark Water Stress Indicator Pakistan is bracketed with nations under water stress, for our per capita water availability remains less than 1,700m3. If a country’s water availability falls below 1,000m3 it is rated as a water scarce country. Until 2010 Pakistan’s water availability was around 1,223m3.

A researcher at the Pakistan Council of Research in Water Resources (PCRWR), Ahmad Zeeshan Bhatti opines that the International Institute of Water (IWMI) says countries that will not be able to meet estimated water demands in 2025, even after accounting for future adaptive capacity, are called “physically water scarce”.

While countries with sufficient renewable resources that would have to make very significant investment in water infrastructure to access them are called “economically water scarce”. “So as yet we are economically, not physically scarce”, he says.

Pakistan stores 10pc of total surface freshwater with a 30 day carryover capacity (14 million acre-feet) achieved through Mangla and Tarbela dams, says a senior Wapda officer. India remains far ahead with a 170 day capacity.

Irrigation channels’ efficiency remains below 40pc for multiple reasons — chiefly sedimentation — though this could be increased to 80pc with lining as per one research and close to 100pc if piped water supply is to be ensured.

The desired investment alludes water infrastructure.

Besides, due to inter-provincial discord and trust deficit major water reservoirs have remained a contention between provinces. Small and medium size dams are not built for want of resources in provinces although Sindh has lately completed the rain-fed Darawat dam in Jamshoro that has to feed 25,000 acres of its command in rain a dependent area.

A senior Wapda officer, who deals with the water sector believes that things have to go in tandem if sustainable growth is to be achieved.

After building mega dams like Diamer-Bhasha, and 90 small and medium sized dams, Pakistan can achieve 90 day carryover capacity. “Although by 2050 our demand will have been increased considerably” he bemoans.

“Tarbella, that is built on the Indus river, had 9.6MAF live storage capacity in 1954 which has now been reduced to 6.1MAF on account of sedimentation. Clearing sediment involves a huge cost while flushing it can choke downstream barrages that’s why it’s not advisable”, he says.

He adds that due to ownership issues international funding is not feasible for the Diamer-Bhasha dam and that even its completion will offer only marginal relief as with its 6.4MAF storage, impact of sedimentation losses in existing dams can only be offset so that new achievable storage would remain between 1-2MAF.

“If work starts on Bhasha now it takes nine years to complete. I don’t see new storage being built in Pakistan in the next 5-7 years. Successive governments have preferred short term projects for political mileage instead of long term projects”, he observes.

“Water availability may not be a serious issue as it is management that actually matters so that besides storages we have to improve overall irrigation efficiency as well”, he quips.

Wapda has a list of seven future water projects for storage and run of the river purposes which are at the early stage of submission of project cost-II, pre-feasibility and approval of PC-II.

These projects include run of the river Dasu, Mohmand (0.67MAF) and Shyok dams (5.5MAF) for storage with the latter’s feasibility study to be completed in February this year.

As experts and policymakers emphasise water storage, the issue of the dying Indus delta — lies mainly in coastal Thatta, Badin and Sujawal districts — and sustainable environmental flows post Kotri barrage has taken a back seat.

Such flows — essential for deltaic region to check sea intrusion — are often described as a wastage of water, notwithstanding the fact that the sea continues to devour fertile agriculture lands in coastal, Thatta, Sujawal, parts of Badin, Karachi and districts along Sindh’s 350km long coastline.

The Fishing sector has also suffered badly as sea intrusion also erodes the continental shelf which is developed by river water and contributes 70pc of marine fish production.

Around 3.5 million acres of land has been claimed by the since 1980 with sea water intruding up to the Thatta-Sujawal bridge.

“Germanwatch in its Global Climate Risk Index 2017 has ranked Pakistan seventh in terms of vulnerability. It perhaps necessitates that we should revisit the 1991 Water Accord in the backdrop of the climate change scenario as it must have impacted flows considerably.

“Likewise, the Indus Water Treaty can be amended with requirements of climate change”, points out Dr Imran Saqib Khalid, who heads environment and climate change unit at the Islamabad based Sustainable Development Policy Institute (SDPI).

He says that groundwater abstractions on both side of the borders remains massive and unchecked.

“Satellite data shows that the groundwater aquifer tilts towards India”, he claims and urges policymakers to look at how to ensure quality, quantity and equity in water distribution.

But what Dr Imran Khalid suggests not does seem possible unless Pakistan has its National Water Policy in place. The policy’s draft has been submitted to the Council of Common Interests (CCI).

By 2050, says the UN’s World Water Development Report 2015, developing countries would have to increase food production by 60pc. It warns that “climate change will exacerbate the risks associated with variations in the distribution and availability of water resources”.

The provinces need to rationalise water pricing in both agriculture and non-agriculture sectors to improve revenue generation and investment in irrigation. Canal water being cheap usually leads to wastages.

It is encouraging to see Sindh working on draft of agriculture policy as a component World Bank funded Sindh Agriculture Growth Project (SAGP). The draft policy talks about ‘climate smart agriculture’.

Sindh Abadgar Board Vice President Mahmood Nawaz Shah says water pricing is also necessary for all sectors of the economy given the fact Pakistan is heading towards water scarcity. Pakistan’s farm sector gets 95pc of the country’s total water resources while in rest of the world hardly 70-75pc of water is diverted to the agriculture sector.

“We need to have more per acre productivity with the same quantum of water coupled with investment in human resource, technology and an high efficiency irrigation system to achieve our objectives”, he says.

By: Khaleeq Kiani

While the consumer is set to pay a remarkably higher price for the inability of the policy makers to reform the energy sector; with induction of fresh supplies, a major industrial and business sector constraint will stand removed.

Pakistan will begin 2018 with expensive energy prices and breakeven supplies. While the year is estimated to conclude with a bit of electricity surplus after 13 years, gas shortages are unlikely to end by December 2018.

The decade of darkness is likely to come to an end during the year, though at a cost. The consumer is set to pay a remarkably higher price for the inability of the policy makers to reform any of the electricity, gas and oil sectors. With induction of fresh gas and electricity supplies, the major constraint of industrial and business sectors would stand removed.

While the input prices would walk a downward curve because of expansion in global renewable energy sector and the United States entering Liquefied Natural Gas (LNG) market with a bang in 2018; the PML-N government would enter the new year, and an election year on top, with a decision for an almost 25-30pc increase in average consumer-end electricity tariff.

In fact, the electricity regulator — National Electric Power Regulatory Authority (Nepra) —only recently gave in to government demands, after five years of resistance, to allow building higher system losses and lower recoveries in the tariff, besides a quantum jump in Net Hydel Profit payments to provinces — from around Rs1.10 per unit to almost Rs5 per unit (kwh).

And the pattern will go on with average gas rates, oil prices and electricity costs. This emanates from the fact that there are no indications that a decline in transmission and distribution losses in the electricity and gas sector is on the horizon to take root in 12 months from now.

Also, public sector entities have been struggling to sustain a higher recovery rate or inculcate efficiency patterns in the system.

Renewable producer tariffs have been falling drastically over the past few years and are forecast to maintain that trend. Having said that, the renewable market, particularly small hydro, wind and solar resources, in Pakistan is already hitting a road block.

For small hydro projects, the government has announced not to guarantee their power procurement, practically making them irrelevant going forward. For solar and wind, the government would hold competitive bidding with a cap of 400MW and 600MW respectively for the next year.

This is despite the fact that large power projects on imported fuels, particularly LNG and coal, would continue to be operated on ‘must-run’ basis to ensure their economic viability at the cost of foreign exchange.

That should in a sense be a critical point that will shift individual consumers towards self-reliance through alternate sources, and drive them away from the national grid as the price of storage equipment (batteries and cells) starts falling drastically in the international market.

With nominal increases forecast for global oil prices in near future, Qatar appears to be loosening its grip over the LNG market with major output originating from Australia and the US put together. That would also shift producer prices from traditional crude to significantly lower levels based on Henry-Hub dimensions.

The government would need to keep pace with changing LNG prices after having entered into long term supply contracts with Qatar, Gunvor and ENI at a higher base, owing to security of supply, and move towards creating a basket price to take advantage of the upcoming Australian and US supply influx.

On top of that, the price differential between domestically produced gas at about Rs600 per unit and imported price of LNG at Rs1,100-1,200 per unit would continue to cost heavily on the competitiveness of the manufacturing sector, not only with international competitors but also among those stationed in different provinces.

At the close of 2017, the PML-N government is estimated to have added around 6,000MW to the generation capacity since it came to power in 2013 and was able to deliver about 19,000MW to consumers in peak summer of 2017.

About 4,000MW of electricity generation is estimated will be added during 2018 with completion of three LNG projects of 1,200-1,300MW each (total 3,600MW) in Punjab besides the 1,400MW Tarbela fourth extension, 969MW Neelum-Jhelum Hydropower project and completion of Port Qasim Coal based project of 1,320MW among the major sources. The LNG projects at Balloki, Bhikki and Haveli Bahadurshah are currently running at half capacity.

On the other hand, the new year begins with completion of the second LNG processing terminal that puts total gas imports at 1.2 billion cubic feet per day (BCFD) against a decade long gap of about 2BCFD. In the oil sector, there is no major capacity addition lined up for 2018 except for laying of a pipeline for transportation of petroleum products to reduce reliance on road network.

Because of higher LNG imports, the dependence on furnace oil would come down significantly, from about 9.5 million tonnes per annum to somewhere between 6 -7 million tonnes during the year, down by almost 30pc.

That would mean furnace oil based generation, historically above 30pc of average power supply, would be partially replaced by relatively cheaper and efficient LNG based power generation, particularly with the commercial operations of three public sector run LNG projects in Punjab (having better fuel efficiency) to be followed by some smaller independent power producers.

With induction of almost 4,000MW during 2018, the power sector is poised to touch generation capacity of around 25,000MW to breakeven demand, without any spinning reserve to adjust for emergency breakdown, from less than 15,000MW about five years ago.

At the end of the year, the country would be entering an era of capacity trap unless the economy enters the much desired 7-8pc growth rate per annum.

By: Shahab Nafees

Sooner or later there will be little room for businesses clinging on to the old ways.

Booming mobile internet users, a growing economy, better security situation and a lot of young people: these are fair grounds for optimism among start-up entrepreneurs and the IT industry at large.

The number of cellular phone subscribers stands at 143.3 million, around 70pc of the country’s population, according to the Pakistan Telecommunication Authority. The number of 3G and 4G users in Pakistan has also jumped nearly 30pc to 47.2m over the last year, and it’s only going to grow in 2018.

These numbers mean exciting new apps and transforming brick-and-mortar businesses. Consumers are relying more and more on technology and want everything from paying bills, booking a car to buying groceries through their smartphones.

Sooner or later there will be little room for businesses clinging on to the old ways.

E-commerce going up

One area that is particularly flourishing is e-commerce, whose market size is expected to touch $1 billion by 2020.

Chinese Alibaba Group Holding Ltd signed an agreement with the Trade Development Authority in May to promote Pakistan’s worldwide exports by small and medium enterprises through e-commerce.

Around 1.2m transactions valuing Rs9.4bn ($84.9m) were processed through e-commerce in the previous fiscal year, according to the State Bank of Pakistan.

By the end of June 2017, 571 merchants were offering their products online. Major online shopping websites include Daraz, Kaymu and Yayvo.

Adam Dawood, who heads TCS’s e-commerce site Yayvo, said the online portal has already crossed the revenue figures it generated during the preceding fiscal year.

According to his calculations, Pakistan’s e-commerce market size is already larger than $650m.

One reason why the size of the country’s e-commerce remains under-reported is that most people prefer to pay in cash.

This is where fintech and mobile-wallet start-ups come in which are trying to make Pakistan a cash-light economy in the year to come.

The emergence of fintech, or financial technology, has resulted in a variety of apps, websites and services aimed at helping people pay for goods and get loans. Some are even eyeing replacing banks. Banks too proud to innovate

Shakir Husain, CEO of Creative Chaos, a technology, digital and outsourcing services company, agreed that fintech will gain a foothold this year. “Banks across the globe are buying fintech start-ups because they realise they cannot innovate themselves despite all the resources at their disposal,” he said in an emailed response. “The inertia and hubris is far too great at these organisations.”

“Globally, banks and traditional financial institutions are not providing what their customers want or need. This has been going on for decades,” he said. But fintech start-ups “have not only listened to their customers but they’ve delivered real value and innovation”.

He believed that digital transformation, fintech, machine learning, health tech, and sales automation will see traction in Pakistan this year.

However, he stressed that success or failure of most ideas depends on execution. “Pakistan is a great market with very decent connectivity numbers. It’s about providing customers with superior user experiences,” he said.

Gaining consumer confidence

“I believe start-ups are entering the stage of maturity,” said Sibtain Jiwani, co-founder and CEO of SmartChoice.pk, a site that offers comparison of different services.

At the same time, however, just boasting about the huge population and the market size is not enough, and much needs to be done to protect consumer rights to gain their confidence, he said.

“I believe the government must build policies to monitor and empower the end customer if we want to grow.”

Another equally major issue is of growth capital, which is creating a huge gap between demand (start-up) and supply (investor), Mr Jiwani said.

“This eventually results in a start-up either giving equity cheap or injecting private own capital which distracts them to focus on profitability instead of scale and innovation,” he said.

This year will also be big for ride-hailing services like Uber, Careem and Bykea as competition toughens up.

Careem is already seeking to take its presence to 40 cities from 10 at present over the next three years, according to Bloomberg.

By: Khaleeq Kiani

Except for completion of some ongoing projects, the progress on the China-Pakistan Economic Corridor (CPEC) would remain comparatively dull after first two years of an exciting full swing implementation that delivered a host of Early Harvest Projects (EHP) or brought them up to an advanced stage.

2018 will be a year of stock taking and planning for the future of CPEC until 2030. This is because the project would be entering a new phase — from completion of energy projects and road construction the focus would shift to industrialisation and long term financial arrangements between the two countries, having far reaching implications.

Also the implementation would move from roads to railway network. Karachi-Peshawar Main Line (ML-1) worth $8.2 billion and Karachi Circular Railway of $3.5bn estimated cost would be two central areas of attention, provided their implementation milestones are firmed up and agreements are reached on costing and repayment pricing.

The two nations, therefore, have to wriggle through a difficult and tedious process to set the foundation for future implementation.

On the industrial side, it would also be a great step forward if the countries are able to reach commercial agreements and begin physically working on three special industrial/economic zones, so far identified as Rashakai in Khyber Pakhtunkhwa, Dhabeji in Sindh and M-3 in Faisalabad, Punjab, to support manufacturing, job creation and export growth.

One of the most prominent projects expected to be complete under the CPEC during 2018 will be the $2bn Orange Line Mass Transit Project — a signature project of the PML-N government. The Punjab government has recently given the go ahead for the project that remained held up by litigation for almost a year.

In the energy sector on the other hand, Port Qasim Coal fired project of $2bn being developed by Sinohydro Resource of China and Al-Mirqab Captial of Qatar with a generation capacity of 1320MW would achieve commercial operations by June 2018. The project had already been partially energised recently.

With a minor delay in coal mining, none of the power projects in Thar would be available in 2018 while two wind projects of 50MW each in Sindh are scheduled to come into production by September 2018. One of the two 660MW units of China-Hub Coal Power Company (660x2) is scheduled to start operations in December 2018.

The Qaid-e-Azam Solar Park in Punjab was expected to add about 400MW, to the existing 300MW capacity, to reach 700MW.

At Gwadar, a $150 million Eastbay Expressway project is expected to be completed before the close of 2018 while maximum effort is being employed to deliver within next year the $130m worth Freshwater Treatment facility, of five million gallons per day, crucially important for Gwadar Port.

Likewise, a 39-km Havelian-Abbotabad-Mansehra part of $3.5bn Karakoram Highway (KKH) Phase-1 is also heading for completion in May 2018 after the completion of four out (Multan-Bahawalpur-Sukkur-Sadiqabad) of seven sections of $2.6bn Peshawar-Karachi Motorway in April.

Similarly, the cross-border optical fibre cable is also due in 2018 besides another road project spanning D.I.Khan to Hakla section of dual carriageway.

By: Dr Taneer Ahmed

With an emergent middle class, growing income, and youth bulge — aspirant of their prospects — perhaps 2018 may not be as dire as it is predicted to be.

With the general elections in sight the political noise growing louder, Pakistani consumers, who have been at the heart of economic growth, have become conscious of their spending impulse and opt to apply restrain when dealing with real and perceived risks.

In November 2017, the Consumer Confidence Index (CCI) — conducted by the State Bank of Pakistan (SBP) and the Institute of Business Administration (IBA) — dipped by 5.91 per cent to 47.3 points from 50.3 in September.

The lowest this year, the CCI revealed an understandably grim outlook of the consumers amidst the increasingly morbid cycle of economic woes circulating daily in the media.

According to the report, the decline “is attributed to both current economic conditions index (CEC), which decreased by 5.80pc and expected economic conditions index (EEC) that recorded a decline of 6.03pc”. This slightly pessimistic viewpoint was also mirrored in the Nielsen Global Survey of Consumer Confidence and Spending Intentions, 2017.

According to it, “Pakistan consumer confidence decreased four points from the fourth quarter of 2016 but maintained above the optimism baseline at a score of 102.”

But it may not all be doom and gloom on the consumer front.

Dawn’s online survey, carried out towards the end of December, shows that our readers remain optimistic, albeit cautiously, about the upcoming year.

Of the 1,522 respondents, 57.8pc were of the view that the economy would perform favourably next year. Despite perceived economic conditions, only 7.7pc people considered things to take a turn for the worst in the following 12 months.

Among those polled, 59pc are entering 2018 positive about improvements in their personal financial situation, while 16.5pc thought things would more or less remain the same.

It must be conceded that these sanguine souls seem to have pitched their hopes on any changes the election might bring. 59.9pc are looking towards Pakistan Tehreek-e-Insaf (PTI) and its promised “revolution” to uplift the economy.

However, 29.8 pc still remain confident about the current government, Pakistan Muslim League-Nawaz (PML-N) and its economic policies.

But are consumers feeling guarded when it comes to the terse political environment in the wake of upcoming elections? The survey discloses that 38.1pc of them would not consider it wise to spend on big household expenses next year, while a remaining 27pc were uncertain.