INFLATION which is one of the dominant economic problems of our times may be broadly defined as a process of steady and sustained rise in the general price level. Excess of demand over the available supply is the hallmark of inflation. It is a condition of economic disequilibrium.

The inflationary rise in general price level is measured by an index such as the Consumer Price Index (CPI), the Wholesale Price Index (WPI), or an implicit price deflator for the Gross National Product (GNP).History has witnessed inflation of various magnitudes, from mild increases of less than five percent to rates of 100 percent and above a year.

Almost from the very inception of coinage, there have been depreciations of the currency. With the advent of paper money, the opportunity for inflation became much larger and with the development of bank deposit money, the scope for it expanded much further.

Since the first occurrence of inflation in the misty past, the lay public as well as the learned pundits have generally offered two explanations for it, namely excessive money supply and/or jacking up of prices by unscrupulous producers and traders facilitated by the presence of imperfectly competitive labour or product markets in one form or other. Thus the demand pull and cost push explanations are as old as inflation itself.

However, the debate regarding the primacy of one or the other interpretation came into sharp focus only after World War II. The demand pull theorists, by and large, consider inflation fundamentally a monetary phenomenon, its cause and cure being based in money supply variations. The other school considers inflation in contemporary market economies as a problem related to and stemming from social, political and economic processes of income distribution. In their view, it is these processes which determine the growth of money supply, which in contemporary societies is a “sociologically determined variable”. If such a view is taken regarding money supply, the demand pull and sociological interpretations can be fused together to constitute the ‘political economy of inflation’.

Inflation is a monetary phenomenon merely in its appearance and not its causation. Behind the excessive expansion in money supply lie complex socio-political forces over the distribution of income and wealth. Various groups, strata and classes in contemporary society are engaged in an organized struggle over distributive shares. This distributive struggle is not new but it has acquired certain new dimensions in practically all countries of the world on account of the decline of the status order, the heightened awareness and growth of ownership rights. It is this distributional conflict which compels the State to continuously increase the stock of money. Thus, it is with the socio-political process behind the monetary malaise of contemporary society that the political economy of inflation is concerned.

Distributional conflict can no doubt be softened by means of rapid economic growth, provided its fruits reach all members of the society. Rapid economic growth, however, requires a high level of economic resource mobilization and, therefore the sacrifice of present consumption and leisure by the people. This raises the question of the proportions in which the burden of economic growth is to be shared by different social groups.

Social reality is such that every one wants the fruits of economic progress without sharing its proportionate burdens. Particularly when incomes are sharply unequally distributed, the conflict in respect of cost sharing to provide resources for growth becomes very intense and the government is under pressure from many sides. In this difficult situation government is often compelled to take recourse to the method of inflationary finance.

Inflation, in other words, becomes politically the most convenient way of taxing the people. The socio-political compulsions can be traced behind all types of inflation experienced by different nations at different times.

These groups do not explicitly ask for inflation, but it is their demands which, if fulfilled, usually lead to it. These implicit demands for inflation arise from pressures on government to pursue an expansionary policy or not to pursue an anti-inflationary policy. These may stem from tax payers who demand lower taxes and exemptions or who resist tax increases and the enlargement of the tax base; or these may emanate from beneficiaries of government programmes who resist expenditure reductions or the imposition of appropriate user charges; these could be ignited by groups attempting to obtain an increase in their share of national income e.g. farmers demanding higher agricultural support prices.

The response of the government to these pressures keeping in view its vote maximizing objective, results in inflationary mobilization of resources. Thus,in the short run, accelerations in money supply and prices represent a politically rational response to the varied pressures exercised by the beneficiaries of inflation or by those who are going to suffer as a consequence of disinflationary measures. It is, however, also a fact that politically motivated inflation if persisted in for a considerable period of time can assume serious proportions with unwelcome consequences for the government perceived to be responsible for it.

Endemic inflation, as is well known, is a regressive form of taxation; it tends to aggravate inequalities, accentuates the strains on balance of payments, diverts resources into socially wasteful uses such us luxury housing, speculative inventories, bullion and jewellery and results in flight of capital; it enlivens speculation and stimulates unessential consumption aside from generating a climate of industrial strife and rendering national accounting difficult. A chronic inflation is not truly stable.

It is somewhat paradoxical that despite being aware of these evils associated with chronic inflation and notwithstanding the loud and clear bells of history in this regard, governments find themselves unable to stabilize prices within reasonable limits. Skills in handling inflation, though well known are difficult to apply because of failure in the short run to accommodate political pressures referred to above, in a stable non- inflationary milieu.

There is undoubtedly a conflict between short-term political expediency and medium as well as long term economic rationality in regard to inflation control. Unfortunately, most rules succumb to the temptation of politically easy short term economic solutions, hoping the long term will look after itself. They seem to endorse the celebrated dictum of Lord Keyness that ‘in the long run we are all dead’. Successful inflation control is not easy because it involves the deft management of complex social and political systems and not just money supply.

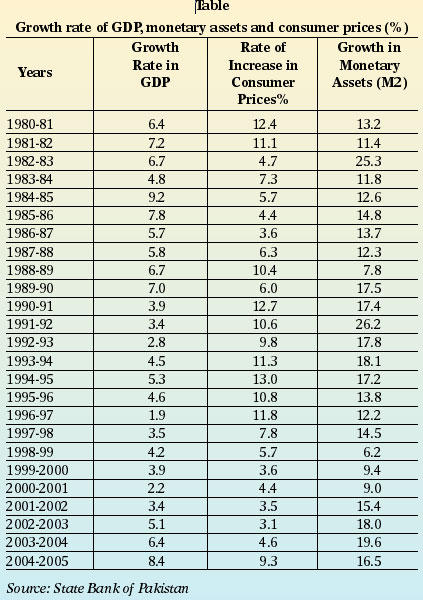

Pakistan has been grapping with inflationary pressures of varying intensity for the last 58 years. Apparently these can be attributed to a disequilibrium between the expansion of money claims and the growth of the real economy. A careful analysis of this persistent upward price trend, however, would reveal that socio-political factors in the context of the anatomy of power in our society provide the breeding ground for their continuance.

According to official statistics, consumer price index has increased 35 fold between 1949150 and 2004-05.

The successive governments in Pakistan have found it very difficult to mobilize adequate resource for our pressing current and development requirements without recourse to inflationary finance on account of their failure to resist powerful vested interests and influential lobbies. This is reflected in our failure to tax ourselves adequately or to curb non- development expenditures because of pressures emanating from such groups.

At present, we have a tax structure which falls short of all major functions of a modern tax system — adequate revenue generation, efficient resource allocation and equity. To satisfy the different lobbies, the tax system has a host of tax exemptions and concessions.

The ratio of taxes to Gross Domestic Product (GDP) at 10.1 per cent in 2004-05 is disappointingly meagre. The share of direct taxes in this meagre ratio is 31.4 per cent.

Total government revenue (tax plus non-tax) accounted for 13.0 per cent of GDP in 200405, while the total consolidated budget expenditure was 16 per cent by GDP.

The Medium Term Development Framework (MTDF) covering the period 2005-10 has articulated a strategy for mobilizing adequate financial resources to achieve the envisaged annual growth rate of 7.6 per cent in Gross Domestic Product. It projects an increase in government revenue from 13 per cent of GDP in 2004-05 to 14.8 per cent in 2009-10. The Central Board of Revenue (CBR) is expected to add to its normal collection, a revenue of 0.3 per cent of GDP per annum for the next five years.

Fiscal deficit will be kept under four per cent of GDP. Together with a prudent monetary policy, inflation will be kept in check by bringing down its rate of 7.0 per cent by the end of MTDF. The monetary expansion, it is hoped, would be commensurate with the growth momentum of the economy, providing required amount of credit to the private sector to serve as the engine of growth, but at the same time keeping strict vigilance on exchange rate and price stability and curbing inflationary expectations.