BRUSSELS, Jan 2: Financial markets gave the euro a strong vote of confidence on Wednesday as the near flawless New Year launch of notes and coins simultaneously in 12 European Union countries won widespread praise.

BRUSSELS, Jan 2: Financial markets gave the euro a strong vote of confidence on Wednesday as the near flawless New Year launch of notes and coins simultaneously in 12 European Union countries won widespread praise.

Commuters and shoppers shrugged off the inevitable confusion and some queues when more than 300 million Europeans from the Mediterranean to the Arctic Circle began spending their common currency on the first working day of the year.

The euro, already traded on paper for three years, surged by more than one percent against the dollar and yen and a record two percent against the British pound in what one banker called a “relief rally” after forecasts of chaos proved unfounded.

“This is more than a one-day wonder — now the euro is a reality, you are going to get euro creep, and it will positively affect sentiment,” said David Bloom, currency strategist at HSBC Markets in London, referring to expectations that the currency will gain commercial acceptance beyond its own borders.

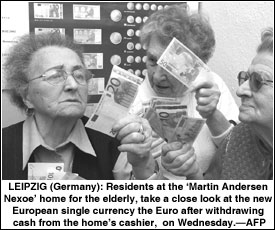

There were long lines in German banks as customers rushed to convert big cash sums of marks into euros, even though national currencies can still be used for another two months. One Deutsche Bank branch briefly locked its doors for security.

Like the Millennium bug — a widely feared global computer breakdown that fizzled on January 1, 2000 — the rollout of the single European currency confounded prophets of doom with what Spain’s El Pais called “watchmaker’s precision”.

European Monetary Affairs Commissioner Pedro Solbes said he was delighted with the clockwork efficiency of the changeover, the largest peacetime logistical exercise in history.

“I am extremely satisfied with the course of the events,” Solbes said, adding some 80 per cent of cash dispensers in the euro area had already been converted and more than half of all transactions should be in euros by the end of the week.

Early morning travellers faced some delays due to the unfamiliarity of the new coinage but scattered banking strikes in France and Italy, a software failure in Dutch post offices and a Greek bank robbery caused only minor disruption.

The next major hurdle will be on Saturday, traditionally the biggest shopping day of the week in Europe.

By eliminating currency risk and creating price transparency in their single market, euro states hope to make their economies more competitive and encourage trade, travel and investment.

While 12 states have adopted it — Germany, France, Italy, Austria, Portugal, Spain, Finland, Ireland, Greece, Belgium, the Netherlands and Luxembourg — the euro has already spread well beyond their borders and the pound’s plunge on Wednesday showed many investors think Britain may eventually opt for it too.

EURO RISES AGAINST DOLLAR: The euro surged above 90 US cents on Wednesday and tested two-month high points, gaining a psychological boost on its first trading day after notes and coins were issued in the 12 euro-zone nations.

Celebrating its long-awaited birth after a three-year incubation period, the single European currency soared more than a cent against the dollar to ride as high as 0.9063 dollars, breaking the 0.90-dollar threshold for the first time since mid-December.—Reuters/AFP